Wage Growth Is Critical In Today’s Context

Our core scenario for 2022 called for normalisation: economic growth cooling towards potential levels, which combined with easing supply constraints, would allow inflation to cool as well. While the former macro trend has been affirmed, the latter has been, at best, deferred or, at worst, derailed. Growth conditions have normalised significantly, but the combination of the Russia/Ukraine conflict and additional Covid lockdowns in China have further disrupted supply chains and sent various commodity prices higher, supporting the level of inflation. The manner and pace by which these divergent forces reconcile will drive financial markets in the months ahead: will central bankers manage to rein in inflation while avoiding a hard landing? Or will an inflationary mindset reign supreme?

It’s Good To Be King

What’s Next?

You’ve Lost that Lovin’ Feelin’

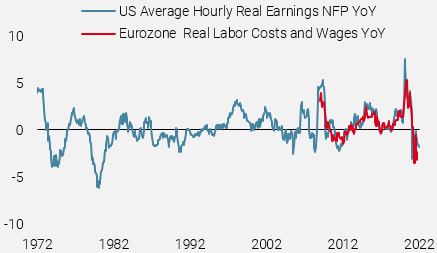

After an unprecedented fiscal and monetary stimulus in response to the pandemic and ensuing lockdowns, a deceleration in global growth should surprise no one. Importantly, most of the stimulus – direct payments to households and businesses – looks to have passed through to the economy already, with US and European household savings rates back to their pre-pandemic levels. At the same time, real wage growth in the US and Eurozone has been negative for nearly a year (Figure 2), as nominal wage increases have not kept up with inflation.

Figure 1: Real Wage Growth (%)

Source: Bloomberg, Unigestion, as of 07 April 2022

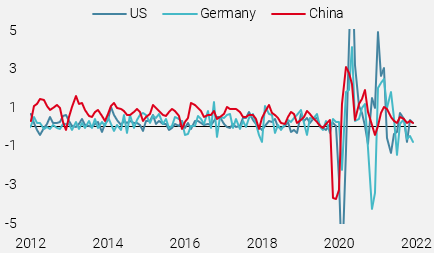

In the context of lower real incomes and deteriorated savings, it is not surprising that actual spending has slowed significantly. Figure 2 charts the month-over-month changes in real retail sales for the US, Germany, and China, demonstrating how significantly the growth in sales volumes has fallen.

Figure 2: Month-over-Month Real Retail Sales (3mma, %)

Source: Bloomberg, Unigestion, as of 07 April 2022

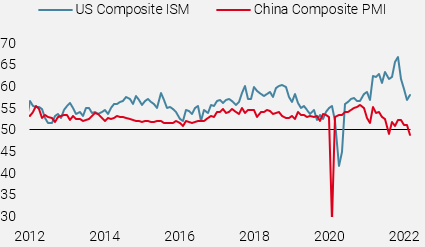

The corporate sector is naturally seeing a marked slowdown in light of the slowing demand. PMIs have been sharply dropping, as shown in Figure 3. The impact of lockdowns in China is especially stark, with sub-50 PMIs indicating economic contraction.

Figure 3: US and China Composite PMIs

Source: Bloomberg, Unigestion, as of 07 April 2022

Go Big or Go Home

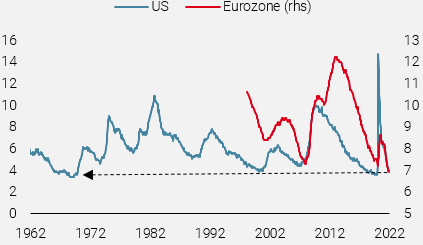

Slowing demand would typically constrain price pressures, but following further disruptions to supply chains due to the Russian invasion of Ukraine as well as lockdowns in China, commodity prices have continued to rise strongly. However, it is critical to note that the growth in prices has been largely stable, which should stabilise the broader inflation picture. It is also important to understand that inflation is inherently a backward-looking measure, reflecting how prices have evolved over the last year. It does not indicate their likely path going forward, which is paramount for investors. Looking ahead, the path of inflation will likely be determined by the reaction of wages to mounting prices in the broader economy. Tight labour markets (see Figure 4) have translated into higher nominal wage growth, which have nevertheless been unable to keep apace with inflation.

Figure 4: Unemployment Rates

Source: Bloomberg, Unigestion, as of 07 April 2022

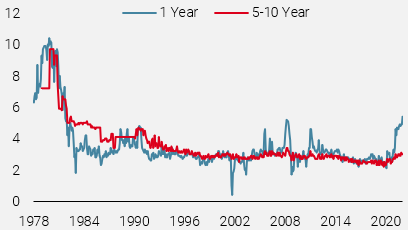

The 1970s are at the fore of many investors’ minds, given today’s context, when an inflationary mindset took hold, following the 1973 oil shock. Employees asked for increasingly higher nominal wages, even as their real wages fell, leading to lower real demand and hence the dreaded stagflation. Inflation expectations have been rising significantly over the last year, but as Figure 5 shows, they are still not at the levels seen during the depths of the 1970s experience. Importantly, longer-term inflation expectations are in line with pre-GFC rates, which suggests that a more lasting inflationary mindset has yet to materialise. These individual decisions among employees and employers over the next few months will ultimately determine whether the current inflationary period abates relatively soon or extends into the years ahead as part of a vicious price/wage spiral.

Figure 5: University of Michigan Inflation Expectations Survey

Source: Bloomberg, Unigestion, as of 07 April 2022

I’m So Humble

After an eventful start of the year, the next few months should provide investors with greater insight on the sustainability of the current inflationary environment and the consequent reaction of monetary policy. The key question will be to what extent central bankers can raise real rates to tame inflation without triggering a recession, or whether an inflationary mindset takes hold and drives wages and inflation expectations higher, thereby keeping real yields depressed. Markets are expecting central banks like the Fed to be successful in avoiding a “hard landing,” which is a difficult task at any time, never mind during a major geopolitical conflict. From an asset allocation perspective, with such high levels of uncertainty, we prefer to keep our risk moderate and our exposures selective: underweights in bonds and overweights in equities and real assets are modest and tilted toward markets that we believe will be most resilient to the risks of monetary policy and geopolitics.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster moved higher, as US data showed an improving economic picture.

- Our World Inflation Nowcaster was steady, as inflationary pressures remained broadly high and stable.

- Our Market Stress Nowcaster declined modestly due to improving liquidity conditions.

Sources: Unigestion, Bloomberg, as of 8 April 2022.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).