The current and unprecedented macro shock prompted a marked deterioration in both market sentiment and growth asset valuations. However, we are now seeing increasing signs of a stabilisation across each of these three dimensions. Macro data remains grim but it has stopped getting worse, especially the highest frequency data. Market sentiment is still bearish but positioning has settled, opening the door to a more rational price evolution. Finally, valuations have partially retraced from very low territory. All factors that determine our dynamic asset allocation have therefore stabilised: we think that the time has come to focus more on the direction than on the level of things. Our dynamic positioning retains its neutral stance but we have positioned tactically to profit from selected credit spreads and equities.We Are Focused on Changes Rather Than Levels

Mask Off

Macro indicators have collapsed globally, reflecting the rapid implementation of lockdowns and economic inactivity throughout the world. Market observers have witnessed variations in macro series unlike anything ever seen before. The most emblematic of these extraordinary variations is probably the increase in US jobless claims, which rose from an average of 200,000+ per week to a peak in 27 March, reflecting an increase of 6.9m job losses. As of last Friday, the US unemployment rate reached 14.7%: a total of 20m people without jobs, albeit temporarily for some of them. This deterioration in macro series rapidly led our Growth Nowcasters to reflect the fact that the world was facing a global, lockdown-triggered recession. In the case of the US, it has reached -2.3 standard deviations, with the Eurozone and the UK showing similar levels, while China, Thailand and South Korea remain in the -1 to -1.5 region. Nobody can dispute the message conveyed by these values: the shock we are currently experiencing is extremely bad. A key element in our understanding of the connection between macro and market dimensions is that when the macro side ceases to deteriorate, this is usually the moment to, at least, neutralise a negative bias for growth assets: to some extent, the derivative matters more than the level of macro conditions. A recovery should be coming as the lockdowns end, but it will take time to show in genuine macro data. To capture this stabilisation, we are looking in three different directions: Our Growth Nowcasters currently show that 30% of data is improving: this number will eventually confirm what we see elsewhere. For now, this early stabilisation is reflected in our strategies through an overweight for “quality growth” equities such as the Nasdaq and the SMI: this positioning aims to profit from this early macro stabilisation. This stabilisation comes with a boost from central banks and governments. In our opinion, this is now old news but it should keep on influencing markets, especially investment grade credit. The key liquidity and corporate bond buying programmes of the Fed and of the ECB have been announced, with most of them partially implemented around the end of March / beginning of April. What strikes us about this is what is happening in credit markets: the Fed has not yet started buying bonds and is currently readying itself for ETF purchases. Yet, cash bonds have seen their spreads contract rapidly. In the US, investment grade cash bond option-adjusted spreads over government bonds reached a peak of 401 bps on the 23 March. Since then, they have come down very rapidly and stabilised at around 225 bps. In investment grade European credit, the peak was reached on the 24 March at 243 bps, but currently sits at 187 bps. In our valuation metrics, in spite of this tightening in spreads, the investment grade spread risk premia does not look expensive yet. Historical analysis suggests that the 12-month forward return following such a level has been positive with a 70%+ hit ratio. Finally, as the Fed starts buying bonds without price sensitivity, its mechanical impact will further narrow these spreads. We see here a remarkable alignment of planets, from valuation to demand in the investment grade space. Once the Primary Market Corporate Credit Facility (PMCCF) for new bond and loan issuance and the Secondary Market Corporate Credit Facility (SMCCF) actually start providing liquidity to corporate bonds markets, we should see a second wave of spread compression. Here again, regardless of the level of these interventions, what matters is the direction of travel for spreads: tighter. Finally, the last elements showing signs of bottoming are market sentiment and valuation. First, most investors have decreased their equity exposures, according to survey data. The AAII US Investor Sentiment survey shows that 50% of respondents are currently bearish, which is actually very close to the average across the month of April (47%). The different beta measures we are looking at show a stabilisation in the equity positioning across many types of investors – quant and discretionary. As many retail investors are still holding a large portion of cash, this should instill in markets a “buy-the-dip” kind of psychology that could also support growth-oriented assets in the future. What is more, investor positioning is now much cleaner than before the crisis: should markets go through another round of downward correction, this should help cushion the extent of the drop, which is noteworthy now that geopolitical tensions could be building again. Finally, the valuation of growth assets through our indicators are showing a consistent pattern: they moved from expensive (January-February 2020) to cheap territories (March-April), but they have stopped getting more attractive. Our conclusions regarding the developments in these three factors (macro/sentiment/valuation) are the following: the situation is bad globally, but we think the time has come to focus on the direction of these early trends. This is why we have moved our positioning from defensive to neutral. This neutral stance is currently becoming more positive through overweights to investment grade spreads, “quality growth” equities and emerging equities in ways that best reflect our current assessment.What’s Next?

The second derivative shows early signs of stabilisation

Monetary policy has not yet fully kicked in

Sentiment as a tailwind while valuation neutralises

Unigestion Nowcasting

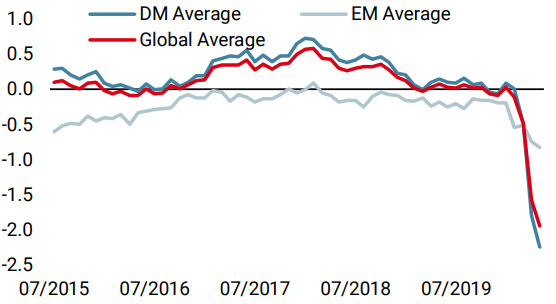

World Growth Nowcaster

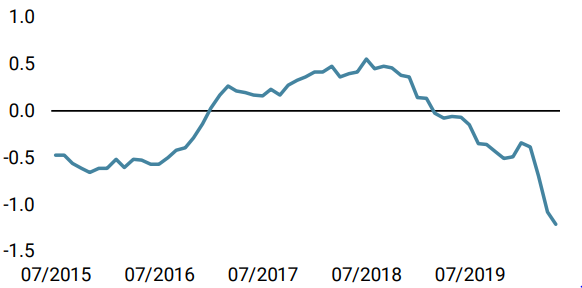

World Inflation Nowcaster

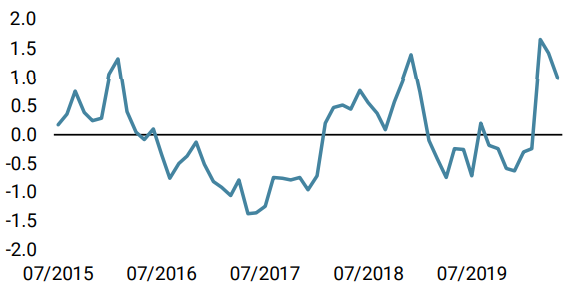

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster decreased again last week, across EM and DM economies alike, but the diffusion index has stopped deteriorating. Our world indicator has now reached a value of -1.94 standard deviations, indicative of a very high risk of recession.

- Our world Inflation Nowcaster also fell across all countries we monitor. This decline is consistent with dire growth conditions.

- Our Market Stress Nowcaster only marginally declined last week as liquidity further improved while spreads increased slightly.

Sources: Unigestion. Bloomberg, as of 08 May 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).