In a famous speech, former Fed President, Alan Greenspan said about ‘Fed watchers’: “I know you think you understand what you thought I said but I’m not sure you realise that what you heard is not what I meant”. Q1 2021 may be celebrated for many things: the first anniversary of one of the biggest equity crashes in history or the quarter with the biggest year-on-year rise in global equity indices. For some, it may even be seen as the beginning of a new economic era with the return of inflation. In our view, the most important event this quarter was the Fed meeting in March, given its credibility with investors, its leadership among central banks and its weight on the Treasuries market via the use of its balance sheet. In a context of rising interest rates, which has contributed to a wide dispersion within and between assets, what can we conclude from the message delivered by the US central bank?

Higher

What’s Next?

A history of “Don’t Fight the Fed”

A history of the Fed’s monetary policy since 1970 can be divided into three main periods. 1970-1987 saw the fight against inflation, represented by Chairman Volker’s aggressive policy of using interest rates as a weapon to curb the upward cycle of inflation. During this period, “Don’t Fight the Fed” meant higher rates. In this context, the correlation between US 10-year interest rates and the S&P 500 index was negative (-0.3). The period that followed, 1987-2007, focused more on economic growth and full employment. However, the financial deregulation observed over the period increased the interdependence between financial markets and the real economy, leading the Fed to intervene to maintain financial stability. This was the famous “Greenspan Put”, represented by the rate cut that followed the 1987 crash, but especially by the significant monetary easing policies designed to smooth the negative impact of the internet bubble burst. During this period, “Don’t Fight the Fed” meant low volatility via stable rates. The correlation between stocks and interest rates reversed and became positive (+0.3). Above all, the volatility of assets fell significantly, as Stock and Watson pointed out, calling this period “The Great Moderation”. The period since 2007 has been characterised by an exaggerated version of the “Greenspan Put” because the imbalances after the 2008 crisis were more important to restore and because deflation became the number one risk. Represented by the generalisation of QE and the massive use of the Fed’s balance sheet, “Don’t Fight the Fed” meant “lower rates for longer”. In this context, the sensitivity of financial markets to duration rose significantly, increasing the positive correlation between rates and risky assets; hence, the famous epithet: “bad news is good news”.

What about 2021, when the policy mix in the US has never been so accommodative, combining low rates, central bank balance sheet expansion and ultra-supportive fiscal policy? Are we entering a new era with a new meaning of “Don’t Fight the Fed”? How can we interpret the apparent contradiction between high economic forecasts for the next few years in terms of inflation and growth, and the dots projection that shows no hike before 2023?

“Don’t Fight the Fed” in 2021

In our view, following the various communications from the Fed over the last few weeks, “Don’t Fight the Fed” can be summarised in one word, “higher”- higher inflation, higher growth and higher interest rates. There are two key messages from the last Fed meeting:

- Inflation is welcome. Higher prices validate the “reflation” policy put in place by the Yellen/Powell duo. In this context, the increase in nominal interest rates (+80bps since November) mainly driven by the rise in the inflation premium (+55bps since Biden’s election) is not a cause for concern (especially if the path of adjustment is gradual) but a positive sign of normalisation.

- Being “behind the curve” is not a problem. On the contrary, it is a deliberate decision by the Fed because this position offers the best “risk reward” in terms of monetary policy (versus being proactive, as in 2013). On one hand, it ensures a gradual increase in the inflation and growth premia contained in 10-year interest rates because the absence of monetary tightening reflected in the dots for the next two years constitutes a limit to the increase in nominal rates. We estimate that this cap could be between 2.25% and 2.50% and we expect that, in the coming months, the market will test this upper limit to evaluate at what level the Yield Curve Control might be implemented. On the other hand, this position is encouraged by the implementation of “Average Inflation Targeting”, which allows for a more sustained upward deviation from the inflation target than in the past. Finally, the Fed considers that, in terms of the risk of monetary policy error, it is easier to fight against too much inflation than against lasting deflation, triggered by a premature tightening of financial conditions.

Asset allocation consequences

When the US Treasury and the US central bank want inflation, the best thing to do is to listen to them and position your portfolio accordingly. This should be translated as:

- A reduction in bond exposures that are expected to deliver negative or poor returns this year because of the gradual adjustment of both inflation and growth premia;

- An increase in real assets due to expected returns exceeding the average returns of the last decade, which was characterised by deflation risk. These assets – such as inflation breakeven, cyclical commodities, currencies of countries linked to global trade (AUD/NOK/CAD for developed countries), and cyclical equity sectors such as Energy, Banks, Industrial, Material – tend to benefit from rises in realised inflation and the underlying boost in activity.

At the beginning of 2021, these assets appeared all the more interesting as they were both attractive in terms of valuation and also “under-owned” by investors who, for the last few years, have been very concentrated in so-called defensive assets such as sovereign bonds and individual Quality/Tech stocks. This rotation has driven the performance of assets more than usual during Q1. Over the period, this resulted in a significant underperformance of the MSCI World Market Cap index versus the MSCI World Equal Weighted index, an underperformance of the Momentum factor versus Value and, above all, negative performance for most bond indices. Indeed, the Barclays Global Aggregate Bond index delivered its worst performance since 1994 with a quarterly return of -2.5% while its US counterpart lost -3.4%. Consequently, the spread between benchmark Treasuries and bunds has widened by more than 50bps. This about matches the move seen in the final quarter of 2016, the biggest jump since 1993.

This dispersion, which is reversing secular trends observed since the GFC, has been large and resulted in very different performances for investors invested in flexible balanced solutions such as 50% equities / 50% bonds. Depending on their investment universe and their degree of flexibility, the range of the quarterly performances observed in Q1 2021 has been wide. This is because, first, higher rates in the US had an impact in terms of geographical allocation. A balanced portfolio invested in global indices (MSCI AC / Barclays Global Agg) returned 0.9% in the first quarter of 2021 compared to 3% for a similar portfolio invested in European assets (MSCI Euro / Barclays Euro Global Agg) and only 0.6% for a portfolio invested in US assets (MSCI US / Barclays US Global Agg). Second, a tactical allocation implemented at the beginning of the year, that reduced duration exposure by 10% and added 10% in real assets (50% breakeven inflation / 50% cyclical commodities) would have added value and significantly reduced the volatility of these strategies.

The rotation should continue and amplify

While in our view, “Don’t Fight the Fed” means more inflation and more growth – in short, a shift from recovery to expansion – it also implies that investors will need to adjust their portfolios faster. We expect a continued upward adjustment of US rates in the coming months and a continuation of the rotation between and within assets. In that expected macroeconomic backdrop, we maintain a negative view on defensive assets, primarily government bonds and investment grade credit. On the other hand, our positive view on real assets is reinforced by the economic evolution in the US, boosted by the stimulus plans announced and implemented by the Biden administration, and the significant progress in vaccinations. In an expansionary context, our preference is for cyclical equity indices such as the Topix or the Russell 2000 indices, Energy and industrial commodities, as well as the US inflation breakevens, which should continue to rise in the coming months.

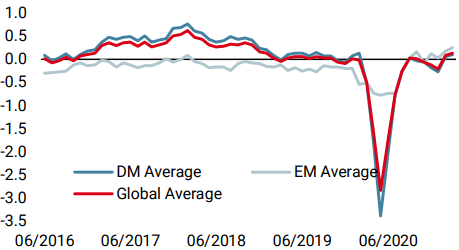

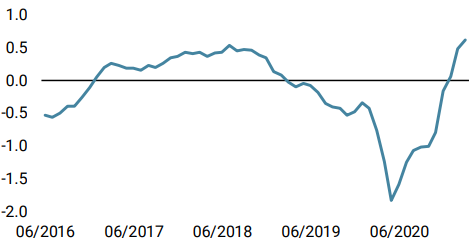

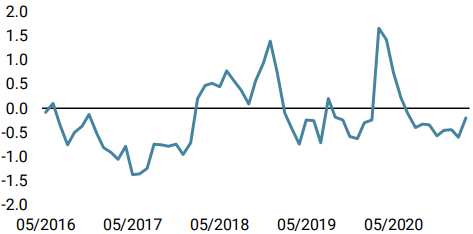

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster increased significantly as both European and US data showed firmer readings. Recession risk is now very low, reflecting that improvement.

- Our World Inflation Nowcaster increased marginally as well: inflation risk remains very high, especially among developed countries.

- Our Market Stress Nowcaster remains elevated, contrasting with the higher readings of growth and inflation: the macro picture is solid, while the stress situation is now elevated.

Sources: Unigestion. Bloomberg, as of 31 March 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).