The sweetest relief comes from the greatest of scares. Risk aversion surged two weeks ago after the eventful “Omicron” episode, as investors digested the wider risks posed by the new variant on the economic outlook. Uncertainty led to panic attacks but then cooler heads prevailed, as a window of opportunity opened for the dip buyers amongst us. After such a volatile event, what can we expect for the weeks ahead?

Sonic Boom

What’s Next?

From a macro perspective, nothing has changed

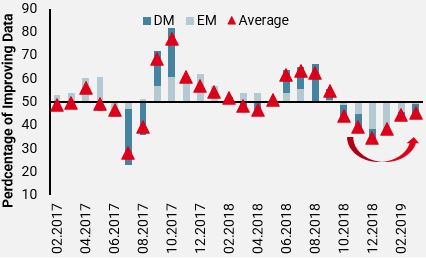

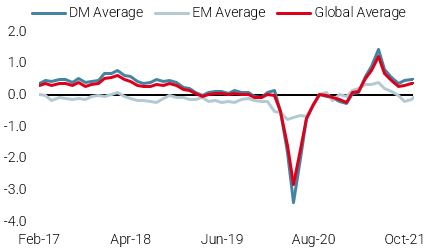

Noise and sentiment drove the markets, rather than signals and fundamentals. But on the economic front, nothing has changed: Growth continues to stabilise at elevated levels while inflation remains strong. The latest round of data is reassuring: on average, the percentage of improving vs. deteriorating data has risen from a low of 30/70 close to 50/50. This stabilisation occurs as underlying growth levels remain above “potential”, or their long terms trends. Despite a surge in “stagflation” fears after the summer, the breadth and extent of growth at present should be sufficient to avoid this adverse scenario going into next year.

Figure 1: Improving diffusion indices – Growth Nowcaster

Source: Bloomberg, Unigestion, as of 10.12.2021

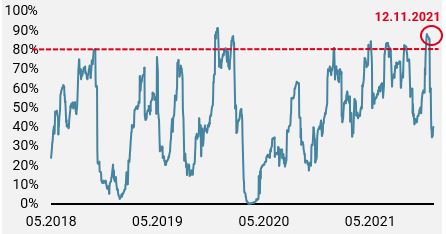

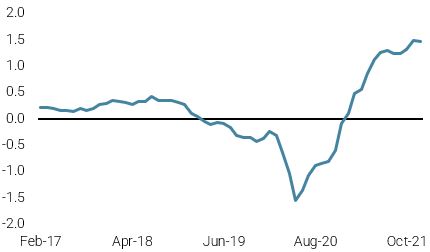

Sentiment: A lot of noise, then quiet

In our view, the price action observed since mid-November clearly illustrated how complacent investors had become. As shown in figure 2, our complacency indicator – which aggregates seven technical indicators such as implied volatility, realised volatility and velocity – had reached extreme levels on November 12. In such instances, when all parameters combined move above their 80th percentile, it waves a red flag, meaning market action over the short term has been a one-way street and that some sort of correction is imminent.

Figure 2: Complacency Indicator

Source: Bloomberg, Unigestion, as of 10.12.2021

The discovery of the Omicron variant therefore resonated like a “sonic boom” while markets were flying at the speed of sound. In addition, Jay Powell’s declaration that the Fed would finally remove its “transitory” inflation wording and accelerate their tapering program came at a very inopportune time; just when financial markets tried to stabilise and find a reason to rebound.

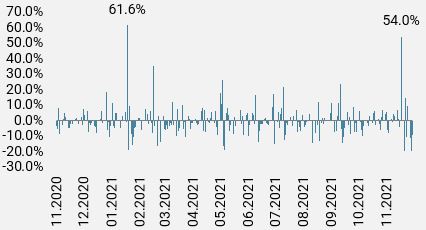

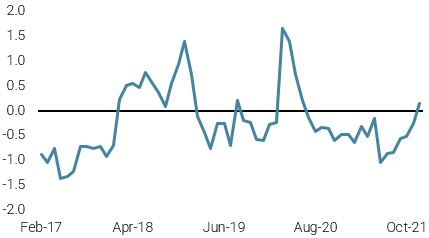

Another illustration of the extreme Omicron reaction was the move observed in implied volatility. The VIX index, which measures the average implied volatility of 1-month S&P500 options, jumped a whopping 54% on November 26th alone, closing at 28.6 vs 18.6 the previous trading day.

Figure 3: VIX Daily Change

Source: Bloomberg, Unigestion, as of 10.12.2021

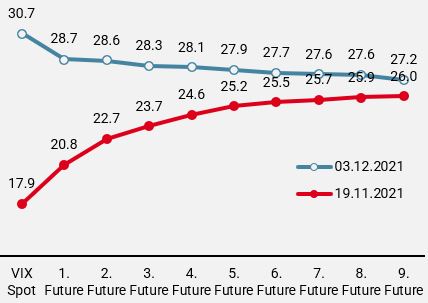

This single day return stands in the top decile, a very rare occurrence, comparable to the multiple standard deviation events like February 2018’s Volmaggedon or the recent Covid crisis. In the meantime, volatility curves have inverted from their usual contango into backwardation, while skew, (the difference in volatility paid for put vs call options) has risen dramatically. All these elements combined point to a disproportionate market stress event rather than a fundamental shift, which later triggered the sharp upside reversal observed last week.

Figure 4: Volatility Curves

Source: Bloomberg, Unigestion, as of 10.12.2021

Healthy correction: a good omen for year-end but mind the Fed

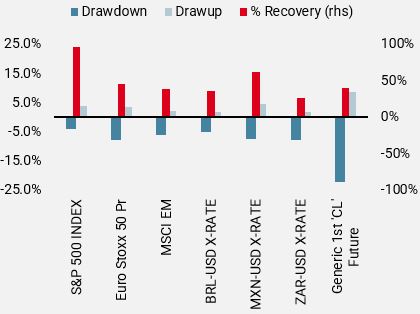

In our view, the Omicron event acted as a wakeup call, and fears will subside once confidence grows that current medical solutions will also be applicable to the new variant. Positions in many systematic strategies have been deleveraged, and the S&P500 aside, most risk assets have not yet fully recovered from November’s market stress event.

Figure 5: Price action in risk assets

Source: Bloomberg, Unigestion, as of 02.12.2021

However, the risk posed by hawkish central bankers will linger into 2022, and the recent unexpected shift by the Fed raises the probability of a new tantrum in the months ahead.

Although current market pricing for monetary tightening in 2022 has probably gone too far and fast, it constitutes one of the main risks we have identified for 2022. Although we believe that we are either at or past the peak, inflation pressures should remain elevated and above central banks’ targets next year. Depending on the pace at which these pressures ease, there is scope for central banks to act faster than initially expected. In that respect, the next Fed meeting on December 15 will be key in assessing the change in economic expectations, alongside the much-awaited new DOTs plot. Given recent market action, a hawkish surprise could dampen the year-end rally and keep volatility elevated. As the year draws to an end and investors reposition their portfolios, we remain cautiously optimistic on risk assets, with minimal exposure to government bonds and a much lower allocation to inflation breakevens.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster was steady with most countries’ indicators remaining stable.

- Our World Inflation Nowcaster moved slightly higher as inflation data in Japan rose.

- Our Market Stress Nowcaster shifted lower as volatility retreated and spreads tightened.

Sources: Unigestion, Bloomberg, as of 10 December 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).