Why US Investors Should Consider European Secondaries

In this Private Equity Q&A, Christian Böhler, Head of Secondaries, and Paul Newsome, Head of Investment Solutions, assess the case for European Secondaries

- The secondaries market has opened up again, particularly for GP-led deals at the smaller end of the market.

- GP-led deals are attractive as there is strong alignment between the secondary investor and the GP.

- European GP-led deals are dominated by multi-asset continuation funds which offer investors greater diversity.

- At Unigestion, we have completed EUR 1.5bn worth of European deals over the last 20 years and have delivered net performance of 1.7x/22% IRR on all mature deals1.

Why is now a good time to invest in secondaries?

When Covid-19 hit western economies last year, the secondary market ground to a complete halt with Q2 2020 deal volumes falling to record lows. Negative market movements and economic uncertainty consequently disrupted many secondary processes. As a result, most transactions were put on hold waiting for markets to stabilise and for the effects of the crisis on target companies to be better understood.

However, since around September, the window of opportunity for secondary transactions has gradually reopened, particularly at the smaller end of the market and particularly in the GP-led space. In fact, H2 2020 volume suggests that secondary transaction pace was already close to 2019 levels in the latter part of last year. As larger LPs look to rebalance their portfolios and more GPs seek to tap into the secondary market for their own cash management needs, we think that secondaries are set for a big 2021.

What’s behind this pick-up in GP-led deals?

There are three key factors that are driving the market at the moment:

- A significant slowdown of exit activity / liquidity issues

- Investors facing large net negative cash flows

- Weak fundraising at the small end of market

The significant slowdown in exit activity in 2020, as highlighted in Figure 1, led to severe liquidity issues, leaving GPs struggling to exit portfolio companies through traditional routes. GPs have therefore started to seek alternative liquidity options for their funds in order to placate their investors who are facing large net negative cash flows. And this has particularly been the case at the smaller end of the market. Given the much larger universe of small and mid-market GPs compared to large cap GPs, there are simply more small GPs with tail-end funds and maturing portfolios. This has created a fertile ground for smaller structured deals, leading to an increasing number of fund restructurings and continuation funds.

In addition, the Covid-19 crisis has created fundraising challenges similar to during the GFC. We have once again seen a flight to larger blue-chip firms. This has left smaller, less well-known sponsors struggling to raise funds. As a result, we are beginning to see a number of GPs switch their fundraising models to deal-by-deal direct secondary models (single assets or a small basket of portfolio companies), which provide full visibility and high capital deployment for secondary investors.

GPs also have to carefully manage their existing portfolios, either to overcome current operating challenges, or indeed take advantage of the current situation and seek finance for expansion through add-on acquisitions. This has again created a significant opportunity for structured and GP-led transactions at the smaller end of the market, where transactions can be easily tailored to focus only on the best performing portfolio companies.

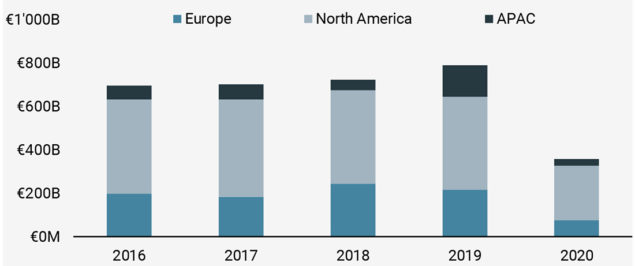

Figure 1: A Collapse in Exit Values Has Been a Key Driver of GP-Led Deals

Source: Pitchbook.

What makes GP-led transactions attractive?

One of the key factors that makes GP-led deals attractive is strong alignment between the secondary investor and the GP. Firstly, the GP typically invests a substantial amount of their own capital into the deal. Secondly, these deals are often a critical part of a GP’s future and longevity and thus they are highly motivated to maximise the outcome.

GP-led deals are often a critical part of a GP’s future and longevity and thus they are highly motivated to maximise the outcome.

Another important point is due diligence. Within a GP-led deal, we get to meet with management teams and question them on their strategy and plans, and we get access to much greater financial data. This means we really get to do a deeper dive on the underlying assets and form a real conviction. This is very important generally, but even more so during the current Covid-19 times when we are looking for assets that are not only resilient and can survive, but can even thrive.

Ideally, we are looking for GP-led deals where we can be highly selective and hand-pick only the best-performing, attractively-valued high growth companies which are at their inflection point in value creation. This means we are not relying on profiting by simply investing at deep discounts, but by investing where there is real growth potential, leading to higher returns without the need to resort to leverage.

Why are European secondaries particularly attractive?

Although the global economic recovery appears to be led by the US, with the European recovery on a slower traction, there are several factors that currently favour European secondaries over their US counterparts. This is due to some key differences in the market dynamics between the two regions.

The European market for GP-led deals is less mature and investors such as Unigestion can “educate” and structure deals with GPs.

Exit activity in Europe fell more steeply in 2020 than in the US. The global aggregate value of exits in 2020 was EUR 358bn, a 50% decline on the previous year. While all regions were lower, the falls were led by Europe (-54%) and APAC (-52%), with North America (-40%) performing relatively better. Low exit activity is a key driver of GP-led secondary activity.

In the US, the secondary market is dominated by single asset continuation funds. In Europe, most GP-led deals are multi-asset continuation funds. While both have their merits, some investors prefer the diversification offered by a multi-asset fund. In addition, the US market is considerably more mature when it comes to GP-led deals, with European deals of this nature less common, especially at the small end of the market. Therefore, there is a lot of white space and investors such as Unigestion can “educate” and structure deals with GPs.

Dry powder is also something that works in Europe’s favour. As at the end of last year, there was USD 524bn of dry powder for US buyouts and USD 220bn for EU buyouts. This suggests that US GPs are more focused on investing new funds than restructuring old ones.

One final point of note is that in Europe, GP-led deals are controlled more by the GPs. As such, deals are much more likely to be sourced through GP relationships than in the US where the market is more intermediary led. Our strong GP network means we have greater access to such deals.

Why should investors choose Unigestion for European secondaries?

At Unigestion, we have been investing in private equity since the 1980s and have over USD 9bn in AUM, with a secondaries track record dating back to 2000. We have a global network of over 500 GPs that we have built up over 30 years, especially at the small end of the market. We believe that local networks and speaking the local languages are very important and are thus able to access a global universe of untapped, off-the-beaten-path investment opportunities. Our deep relationships with GPs also gives us unrivalled knowledge of underlying portfolio companies and we have established a strong reputation as a pioneer in GP-led transactions.

Thanks to Unigestion’s local markets knowledge, we are able to provide more local/region solutions, tailored to the corresponding legal and cultural environment.

In terms of European secondaries, we have completed EUR 1.5bn worth of European deals over the last 20 years and have delivered net performance of 1.7x/22% IRR on all mature deals1. Proprietary sourcing and rigorous investment processes means we can hand-pick exceptional deals and we often lead or co-lead our deals which means we negotiate optimum fee structures and convince GPs to put in their own cash, giving a strong alignment of interests.

Another important factor is that Europe is naturally much more fragmented than the US with many different countries, cultures and legal jurisdictions. Thanks to Unigestion’s local markets knowledge, we are able to provide more local/region solutions, tailored to the corresponding legal and cultural environment – for example, a Danish SPV solution versus an Italian SPV solution versus a French SPV solution, etc. Additionally, our deep local knowledge, extensive experience and strong reputation in GP-led deals means that we can be more actively involved in the small, complex deals we chose to invest in, often gaining a seat on the board or a more advisory type of role.

Overall, dozens of industry awards in recent years for investment strategy and performance, innovation and client service are testament to the quality of our solutions and expertise of our people.

Can you provide a couple of recent deal examples involving European secondaries?

When we make investments we are looking for high growth assets with resilient business models, strong market fundamentals, recurring revenue streams, asset-light balance sheets and visible exit routes. Two deals we can highlight are Adform and Systematic Growth.

Adform was a single asset restructuring closed in Q4 2020 of a leading independent fully integrated software provider to advertisers, agencies and publishers, enabling them to control and target digital advertising spend. The deal was sourced directly through a privileged relationship with the GP at a very attractive entry multiple. The company operates in the high-growth digital advertising spend space, which is also the least cyclical part of the advertisement business. It is one of the few end-to-end product suite providers addressing key parts in the complex digital advertisement value chain. The company demonstrated stable performance during the Covid-19 pandemic, outperforming its peers. It now boasts a well invested technology platform ready for future growth, the full benefits which are not yet visible in the financial numbers.

In 2017, Unigestion led a complex, bespoke multi-asset restructuring of a fund managed by Systematic Growth, a small Swedish private equity firm, specialising in micro buy-and build strategies. In order to provide liquidity to Systematic Growth’s non-institutional investor base, Unigestion purchased a majority stake in a hand-picked portfolio of three companies at an attractive price. Unigestion invested a total amount of USD 60m over two tranches. Since then, two of the three portfolio companies have achieved highly profitable exits in a short time frame and the third continues to perform well. We ultimately expect to deliver total returns of TVPI 2x/25% IRR on this transaction.2

1As of 30 September 2020. Net multiple is calculated as the total value over the invested capital of all secondary deals from 2000 to 2018. Net IRR (Internal Rate of Return) is calculated as an average of all secondary deals from 2000 to 2018.

2TVPI refers to Total Value Paid In and the net multiple is calculated as the total value over the invested capital. IRR refers to Internal Rate of Return.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Additional Information for US Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”).

This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

US

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EU

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Document issued May 2021.