Recent price action in government yields has been among the most puzzling of all the asset classes. All factors necessary for rates to rise are in place – strong macro news, positive risk appetite and expensive valuations – yet yields remain stubbornly low. Both expected and realised inflation continue to rise month after month without any effect whatsoever on nominal rates. So what is stopping investors from exiting government bonds? The answer is central banks. But the real question is: for how long?

Manipulation

What’s Next?

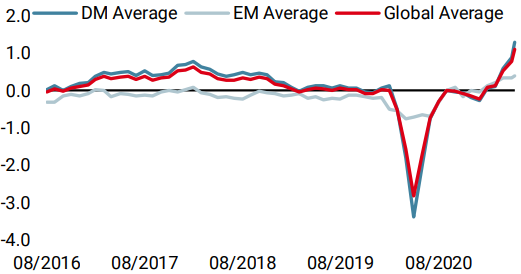

Macro conditions keep on improving

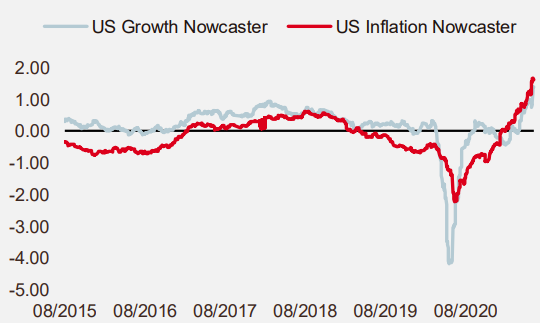

Strong, broad-based, and improving. This is how the current macroeconomic context can be described. Our proprietary Growth Nowcasters and high frequency Newscasters all indicate stronger-than-average and accelerating global economic momentum. The last time such strong numbers were seen was in late 2017 during the so-called ‘Goldilocks’ period. What were once mere expectations have translated into real data. Despite marginal divergences, the situation is homogeneous across developed countries and laggards (such as the Eurozone) are regaining lost ground as reopening accelerates on the back of successful vaccination campaigns.

Historically at least, macro fundamentals should ensure higher interest rates but the disconnect between the two has rarely been so wide. The situation may last longer than expected, but every day new macro torpedoes hit the central banks’ dam.

Figure 1: US Growth Nowcaster

Source: Unigestion, Bloomberg, as of 08.06.2021

Policy makers: the architects of ‘lower for longer’

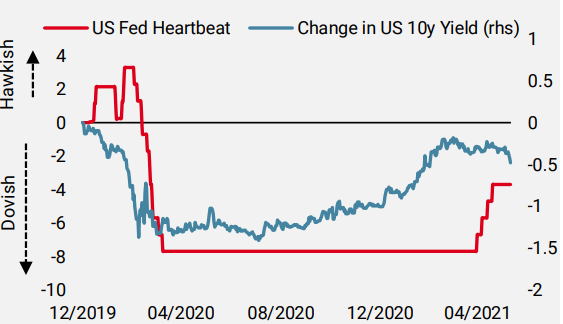

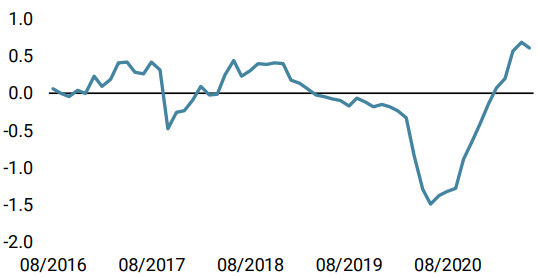

The most powerful factor behind government bond price action is central banks, with the Fed leading the pack. Different mandates have been given to various central banks: primarily price stability (inflation), growth and employment. Outcome-based monetary action should make it easier to anticipate policy makers’ behaviour and – to some extent – market reactions. Today, market sentiment seems to be focusing on the data that supports Fed rhetoric on the temporary nature of the inflation risk, and discarding the data that could prove them wrong. A good example is last week’s CPI data release for May, which came in higher than already elevated expectations. Both the headline and core numbers surprised to the upside but wage growth was negative. After an initial reaction that pushed stocks lower and bond yields higher, equities reversed, rallying to record highs while bond yields drifted lower. At the same time, the ECB did not mention a reduction in the size of its PEPP programme despite revised growth and inflation expectations. However, hawkish voices are emerging among central bankers and there is no longer unanimity on the current level of liquidity injections. Our central bank ‘heartbeat’, which aggregates hawkishness or dovishness over time, started grinding higher a few weeks ago and we believe this is only the beginning.

The disconnect between fundamentals and monetary action is increasing by the day, and we are of the view that the time for a change in stance is coming faster than expected.

Figure 2: Fed ‘Heartbeat’ and Long-term Yields

Source: Unigestion, Bloomberg, as of 10.06.2021

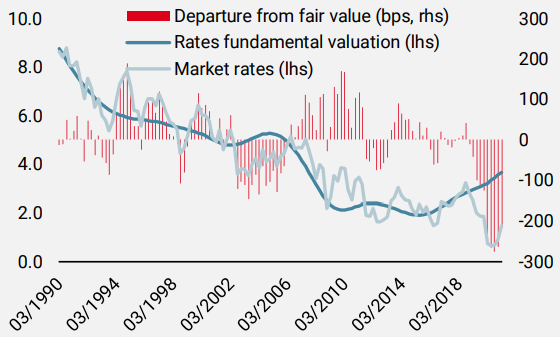

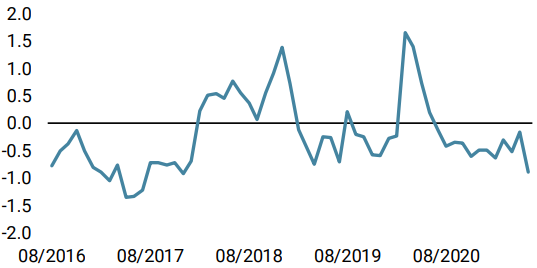

Valuation of long-term yields are stretched…

There are multiple ways to assess the theoretical fundamental valuation of yields but it should in essence take into account growth, inflation and term premia. Given the current level of growth and inflation, the fair value of US 10-yer yields should be in the region of 3.6%. Compared to the actual level of 1.5%, we are currently experiencing the largest deviation from fundamentals since at least the early 90s. This is exactly what central banks’ gigantic accommodation aims at: lowering the attractiveness of long-term rates, reducing financing costs and inducing consumption and investment in riskier alternatives in the real economy or – more often – in financial assets.

Figure 3: US 10y Yield Fundamental Valuation vs Actual Yield

Source: Unigestion, Bloomberg, as of 31.3.2021

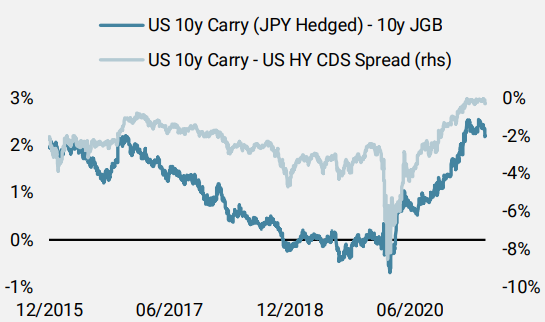

…but there are still buyers out there

Although fundamental absolute valuations are extremely rich in this current macroeconomic expansion, the current level of carry offered by long-term US Treasuries is an arbitrage opportunity for fixed income investors. Indeed, a carry of 3% today seems attractive for most foreign buyers compared to their domestic government bonds’ carry. To some extent, it may also be attractive for asset allocators investing in the credit space through spread indices. With the current US high yield spread at around 300bps, going meaningfully lower in the risk curve for the same expected return seems like an interesting play, as long as you believe that the Fed has got your back on duration risk. Other potential buyers could be systematic trend following strategies and CTAs, which could prompt further buying as yields recede.

Figure 4: US 10y Carry against JGB and HY Spreads

Source: Unigestion, Bloomberg, as of 02.06.2021

Although all necessary conditions to push yields higher are in place, central banks are still keeping rates on a short leash, and it can last as long as they want it to. We believe that the risks associated with this ‘great manipulation’ are growing and that holding government bonds offers unattractive and asymmetric sources of return at the moment. We prefer to stay underexposed to the asset class, and overweight risk premia offering better upside potential against inflationary pressures, such as cyclical commodities and inflation breakevens.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster rose further, with the US being the main positive catalyst.

- Our World Inflation Nowcaster also moved up slightly also due largely to the US.

- Our Market Stress Nowcaster remained low as all sub-components remain stable at low levels.

Sources: Unigestion. Bloomberg, as of 11 June 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).