- Equities

- Papers

- Perspectives

Amélie Séguin

Client Portfolio Manager

Equities

Edward Gladwyn

Portfolio Manager

Equities

- With inflation at multi-decade highs in several countries and with no end in sight, stagflation has become a real concern.

- In an environment of high inflation and low growth prospects, along with restrictive monetary policies, dispersion within the equity market will increase, leading to resilient returns in some area of the equity market.

- Our analysis shows that the Low Risk style has a natural tendency to outperform during such times thanks to its higher exposure to defensive sectors and to a combination of the Value and Quality factors.

- By switching to a Low Risk strategy in the current market context, equity investors can protect their portfolios against downside risks and continue generating longer-term outperformance.

Overview

Inflation has made a marked comeback this year with Russia’s invasion of Ukraine early in 2022, combined with the worldwide easing of restrictions related to the Covid-19 pandemic, pushing commodity and energy prices much higher. These inflationary forces are having knock-on effects throughout the economy, dampening growth expectations

In this paper, we look at the response of central banks to inflation and how monetary policy normalisation may be different this time. We establish the sector and factor exposures best suited to this looming stagflation environment. Finally, we analyse the underlying positioning of the Low Risk style to reveal its strong prospects in periods where growth is lower and inflation is high

Higher Inflation: A Macroeconomic and Central Bank Policy Shift

Since the Great Financial Crisis (GFC) of 2007 to 2009, central bank policies and government fiscal policies have been very supportive. Although global GDP growth came back quickly after the GFC, thanks to central banks pushing liquidity, inflation remained stubbornly low. However, that has all changed very quickly and today’s inflation levels vastly exceed those seen in the last 20 years – indeed for many countries it’s necessary to look back to the 1970’s to find such elevated levels of inflation.

But can we learn from the monetary policy of the 1970s and 1980s to understand central bank action today? Since 2008, a loose monetary policy has been implemented through not only low rates, but also with unconventional easing measures such as repurchase programmes. In providing this supportive environment, central banks had one thing in mind: reaching their long-term inflation targets while sustaining growth. This provided a boost for the economy, as well as for investors through significant asset price inflation even during a period of weak consumer inflation.

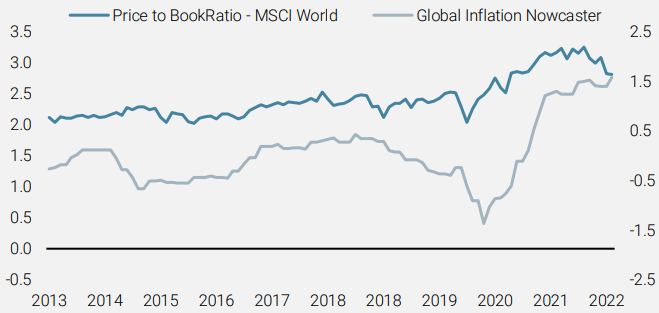

Figure 1: Price to Book Ratio of MSCI World vs. Global Inflation Nowcaster

Source: Unigestion, Bloomberg, monthly Price to Book ratio for MSCI World Index from 31.12.1998 to 31.05.2022.

Today’s inflation increase has been mainly driven by higher energy prices, which have translated into higher input prices. These are damaging corporate profitability, forcing companies to reduce investment and capex, while higher final prices are hitting consumers even harder. While the amount of money needed to operate a company or a household keeps on rising, what remains for non-vital investment or consumption is shrinking. This has led to rapidly decreasing GDP numbers, turning negative for many countries for the first time since the Covid crisis.

Central banks are now adopting a decidedly hawkish tone, showing their determination to bring inflation back under control. They have confirmed their willingness to fight the recent surge in inflation, with a series of rate hikes already implemented by the Fed, the BOE and the BNS over the last few months, while the ECB has also signalled its intention to soon start hiking. These more restrictive monetary policy measures are also bringing tighter financial conditions for companies and for households, which would dampen growth expectations in a high inflation environment.

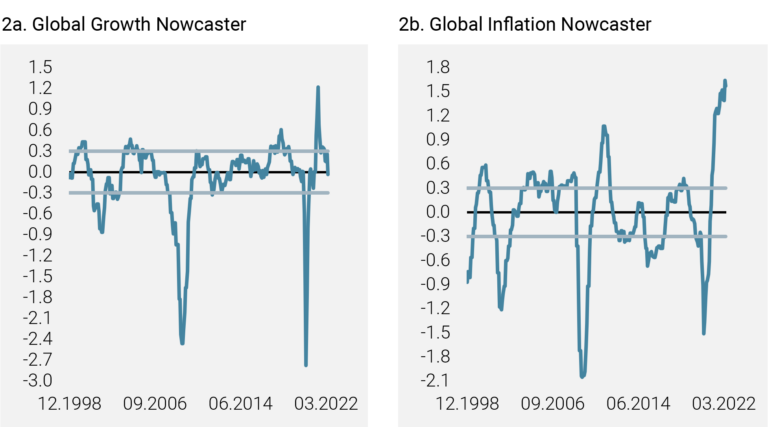

Figures 2a and 2b: Unigestion Global Growth and Inflation Nowcasters

Source: Unigestion, Bloomberg. Data as at 31.05.2022.

Reading notes: The Growth Nowcaster index is a real-time synthetic measure of economic growth. It is computed as a proprietary normalised average of a broad spectrum of indicators spanning the different domains of the economy (production, consumption, employment, investment). The Growth Nowcaster takes positive or negative values. A reading above (resp. below) 0 of the Growth Nowcaster expresses that the economy is growing at a higher (resp. lower) pace than the “normal” growth (also called potential growth).

The Inflation Nowcaster index is a real-time synthetic measure of inflation surprises. It is computed as a proprietary normalised average of a broad spectrum of indicators spanning the different domains of the economy (imported inflation, production costs and expected inflation). The Inflation Nowcaster takes positive or negative values. A reading above (resp. below) 0 of the Inflation Nowcaster expresses that inflation is growing at a higher (resp. lower) pace than expected.

For the definitions of inflation and growth regimes, see the footnote at the end of the paper.

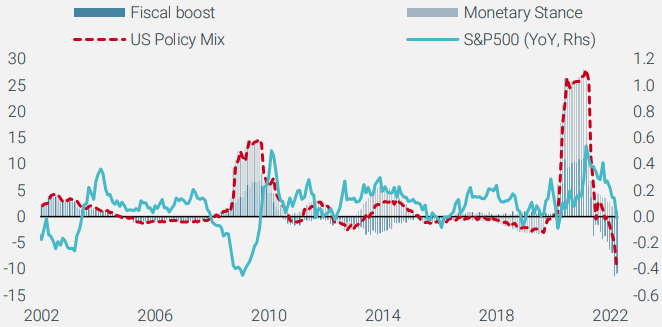

Another tool in the monetary policy normalisation toolbelt is quantitative tightening, which offers central banks a number of options to shrink the size of their balance sheets. One way is to not reinvest the proceeds of maturing bonds the central bank has in its portfolio. This is excatly what the Fed started in June.

All of these restrictive measures will lower money liquidity in the market, and are expected to lead to lower bond prices. Therefore, although government bonds have historically enjoyed safe haven status, the prospect of lower purchases (“demand”) from central banks and higher interest rate expectations means their prospective relative returns may be lower than expected in the past. Looking at equities in such an environment, the dispersion of returns within the market is increasing and some areas of the market will particularly suffer.

Figure 3: US Monetary Policy vs. S&P YoY Returns

Source: Unigestion, Bloomberg. Data as at 27.05.2022.

The Leaders in a Stagflation Environment

In the context of higher inflation risk and lower growth prospects, corporate margins come under pressure and impact profitability. But how do the different market sectors fare in such a macroeconomic environment?

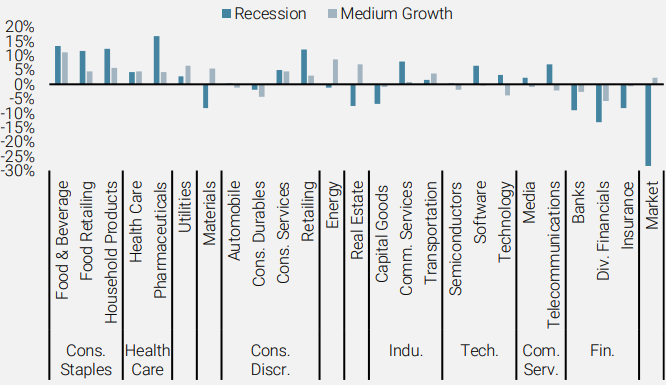

Figure 4: Average Relative Performance Over the Next 12 months of Sectors (GICS2) of the MSCI World Index (USD) in Periods of High inflation Risk and Medium to Lower Growth Prospects

Source: Unigestion, Bloomberg. Data as at 31.05.2022.

Reading notes: Sectors using a global universe, as defined by Unigestion. High Inflation defined by a Global Inflation Nowcaster above 0.3. Recession defined by a Global Growth Nowcaster below -0.3. Neutral Growth defined as a Global Growth Nowcaster between -0.3 and 0.3.

During periods of high inflation risk, we see strong performance from defensive sectors such as Health Care, Consumer Staples and Utilities, as illustrated in Figure 4. The outperformance of these sectors arises from their inelastic demand to consumption, inflation and growth shocks. An example may be in the provision of public services (Health Care, Utilities) in a regulated monopoly where growth prospects are less sensitive to GDP growth expectations. These sectors also benefit from higher pricing power, as final consumer demand is less sensitive to higher prices. Below, we take a closer look at each of these defensive sectors in turn.

Consumer Staples

Although lower growth prospects imply lower consumption, the consumer staples sector is less sensitive to the slowdown, as consumers continue to use basic supplies such as Food & Staples and Household Products. Consumers might shift their consumption from premium products to cheaper alternatives – potentially with lower margins – but this does not result in a total demand destruction. Premium brands may also be more easily able to pass on the price increase directly to consumers.

Health Care & Pharmaceuticals

Growth prospects for the Health Care sector are relatively less affected by a higher inflation and lower growth environment, since they are more a result of a company’s innovation. Research and development programmes often have long funding horizons and may be subsidised by states. On the other hand, although the price of medication and medical care may increase, the costs are passed through the health care system, be it through the state or through health insurance. They are much less likely to be passed onto customers.

Utilities

Utilities supply basic services such as electricity, gas and water. Often the sector provides these public services in a highly regulated setting, with a strong intervention of public institutions. We saw this recently, for example, in France, with the state controlling the price of gas and subsidising it to keep final consumer prices as low as possible. While economic activity may be lower, leading to shrinking demand, the revenue impact can be smoothed by the regulatory mechanism.

The New “Defensive Sectors”: Telecommunication & Software

The increasing reliance of consumers and businesses on digital technology has led to the emergence of a new class of defensive technology stocks. Across the technology infrastructure spectrum – from telecoms through to hardware and enterprise software – the economics of these industries increasingly reflect those of traditionally defensive sectors. Their strong performance throughout the pandemic highlighted this shift in economic sensitivity.

Referring back to our study in Figure 4, we already see some evidence of this in the performance of Telecommunication Services companies during high inflation risk periods. The potential caveat to this position is that many of these companies remain in a high growth phase. While there is certainty in terms of near-term revenues, the stocks remain valued on this future growth and so are subject to the volatility associated with increased uncertainty.

What About the Other Regions?

While our study has been based on a global universe of companies, the superiority of these defensive sectors in periods of higher inflation and lower growth is also applicable to the European and emerging market universes. There are very few specificities in terms of sector hierarchy, especially concerning the Utility sector in Europe, which is more regulated than in other regions. The sector benefits from higher state support in periods of high inflation and lower growth – hence on average, these companies tend to better maintain their margins in such periods and therefore outperform.

Low Risk: The Defensive Play in a High Inflation Risk and Lower Growth Environment

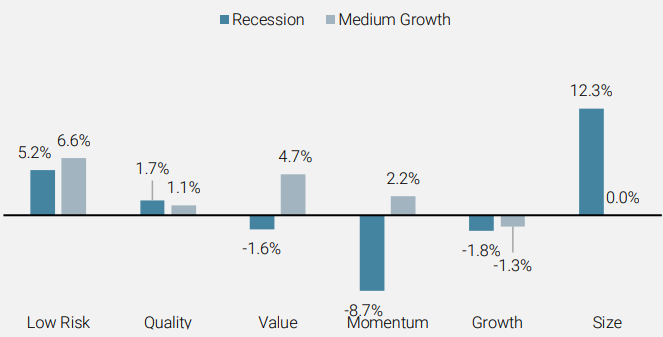

Figure 5: Average Factor Performance Over the Next 12 Months in High Inflation Regimes With Lower to Medium Growth

Source: Unigestion, Bloomberg. Data as at 31.05.2022.

Reading notes: Factors are defined using a global universe, as defined by Unigestion. High Inflation defined by a Global Inflation Nowcaster above 0.3. Recession define by a Global Growth Nowcaster below -0.3. Neutral Growth defined as Global Growth Nowcaster between -0.3 and 0.3.

So Why Does the Low Risk Style Perform Well During These Times?

In short, the Low Risk style is invested in well-capitalised defensive stocks. It is more heavily exposed to sectors such as Consumer Staples, Health Care and Utilities – and as we have already seen, these sectors tend to outperform during periods of high inflation and low growth. The stability of their revenue streams allows them to continue their business and to maintain earnings in line with long-term expectations, despite downward pressure on margins. With fears of stagflation currently at the forefront of investors’ minds, we can expect these areas of the market to continue to thrive.

Balancing Factor Exposures

Higher inflation is a source of uncertainty for future corporate earnings: its size, timing and the extent to which companies may pass through cost increases to the consumer. Under classical models of equity pricing, this uncertainty should be reflected as a ‘discount’ on the value of those future earnings. When the discount increases, the current value of an equity should fall.

In order to maintain stable equity values, it is then important to have stable future earnings in the face of inflation. As illustrated in Figure 5, we see evidence of three factors that perform well during periods of moderate inflation: Low Risk, Quality and Value. There are reasonable economic intuitions why this might be the case.

Traditional Quality definitions tend to focus on profitability – and we see this driving returns during periods of low inflation. We prefer to enhance this metric with measures of balance sheet stability. The result is a factor that shows good performance across inflation regimes – with this stability rewarded during periods of higher inflation.

Value stocks are typically associated with lower growth rates and consequently less uncertainty about the scale of their future earnings. However, their low valuations may also reveal business model risks in the near term. During episodes of moderate inflation, we see strong performance while periods of very high inflation lead to a greater focus on business model risks.

Low Risk proves to be a powerful combination of these two factors. By combining with a focus on price stability, there is an implicit filter to prefer Quality stocks with stable return streams (and not just high recent profitability) and Value stocks whose business models are less exposed to imminent threats (the so-called ‘Value traps’).

Low Risk Equity Strategy in a Stagflationary Environment

Investors have several ways to protect their portfolio against the prospect of higher inflation and lower growth. Although de-risking the portfolio with a reallocation to bonds seems to be a good strategy, the prospective returns of bonds are lowered when central banks are taking the rates-hiking path. Reallocating within the equity bucket to a Low Risk strategy allows investors to maintain their equity asset allocation, while de-risking their portfolio.

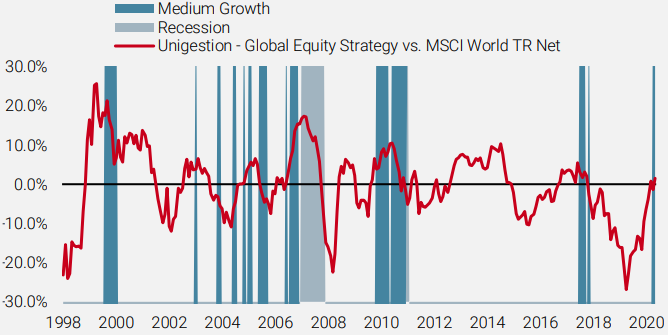

We see defensive sectors outperforming in periods of high inflation risk and lower growth prospects. Further, factors such as Quality and Low Risk see favourable returns. In such a macroeconomic environment, the bias of the Low Risk strategy towards these sectors (see Figure 4) and these styles (see Figure 5), leads the strategy to outperform the market-cap weighted index. We can see this historically in Figure 6, where the performance peaks and troughs of the strategy correlate with the peaks and troughs in global inflation risk. Outperformance increases as macroeconomic stresses arrive in the shape of higher inflation and lower growth prospects.

Figure 6: Next 12 Months Performance of Unigestion’s Global Equity Strategy vs. the Benchmark in Periods of High Inflation (shaded areas)

Source: Bloomberg, Unigestion. Data from 31.12.1999 to 30.04.2022.

Against a backdrop of high inflation and declining growth prospects, global Low Risk stocks have historically shown strong resilience, driven by the inelasticity of demand in defensive sectors to inflation and growth shocks. The characteristics of Quality and Value are enhanced by the combination with Low Risk in this macroeconomic scenario, maintaining a strong visibility on equity fundamentals.

With global economies experiencing such conditions once again, these strategies should be favoured in order to protect equity portfolios against downside risks and to help continue generating the longer-term outperformance.

Inflation and Growth Regimes:

Defined according to the level of the Unigestion Nowcaster from 31.12.1999 to 31.05.2022. The inflation, respective growth, regime is high when the Nowcaster is above 0.3, the regime is considered medium when the level of the Nowcaster is between -0.3 and 0.3, the regime is considered low when the Nowcaster is below -0.3. Nine regimes are therefore defined: a) High inflation risk with low, medium and high growth prospects; b) Medium inflation risk with low, medium and high growth prospects; and c) Low inflation risk with low, medium and high growth prospects.

Important information

INFORMATION ONLY FOR YOU

This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

RELIANCE ON UNIGESTION

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time. Such information is intended to provide you with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf of one or more Unigestion entities will be involved in managing any specific client account on behalf of another Unigestion entity.

NOT A RECOMMENDATION OR OFFER

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Reference to specific securities should not be construed as a recommendation to buy or sell such securities and is included for illustration purposes only.

RISKS

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Unigestion maintains the right to delete or modify information without prior notice. The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, and may experience substantial & sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

PAST PERFORMANCE

Past performance is not a reliable indicator of future results, the value of investments, can fall as well as rise, and there is no guarantee that your initial investment will be returned. Returns may increase or decrease as a result of currency fluctuations.

NO INDEPENDENT VERIFICATION OR REPRESENTATION

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

FORWARD-LOOKING STATEMENTS

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events and are subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. You are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document.

TARGET RETURNS

Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Target returns are based on Unigestion’s analytics including upside, base and downside scenarios and might include, but are not limited to, criteria and assumptions such as macro environment, enterprise value, turnover, EBITDA, debt, financial multiples and cash flows. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

USE OF INDICES

Information about any indices shown herein is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison. You cannot invest directly in an index and the indices represented do not take into account trading commissions and/or other brokerage or custodial costs. The volatility of the indices may be materially different from that of the strategy. In addition, the strategy’s holdings may differ substantially from the securities that comprise the indices shown.

ASSESSMENTS

Unigestion may, based on its internal analysis, make assessments of a company’s future potential as a market leader or other success. There is no guarantee that this will be realised.

No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of this fund and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses.

Legal Entities Disseminating This Document

United Kingdom

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”).

This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

United States

In the United States, Unigestion is present and offers its services in the United States as Unigestion (US) Ltd, which is registered as an investment advisor with the U.S. Securities and Exchange Commission (“SEC”) and/or as Unigestion (UK) Ltd., which is registered as an investment advisor with the SEC. All inquiries from investors present in the United States should be directed to clients@unigestion.com. This information is intended only for institutional clients that are qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

European Union

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

Canada

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

Switzerland

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Document issued May 2024.

In order to extract informative signals from PPMs, we transform the text embedded in the “Investment Strategy” and “Investment Process” sections of PPMs using the Term-Frequency-Inverse Document Frequency vectorizer (TF-IDF)[1]. Then we feed three ML classifiers (Lasso, Random Forest, and Gradient Boosting) with the TF-IDF features to predict the probability that the ultimate fund’s Total Value to Paid-In ratio (TVPI) will exceed the median TVPI of funds raised in the same vintage and pursuing the same investment strategy (LBO or other private equity funds) reported by Preqin[2]. If this probability is higher than 0.5, the fund is labelled as successful.

We assess the performance of three ML classifiers with the ROC (Receiver Operating Characteristics) curve and the corresponding AUC (Area Under the Curve). This latter metric represents the probability that a randomly chosen successful fund (fund TVPI exceeds the median TVPI of its Preqin peers) is attributed a higher probability of being successful than a randomly chosen unsuccessful fund (fund TVPI is below the median TVPI of its Preqin peers). In these terms, an AUC of 0.5 is equivalent to flipping a coin. Thus, the closer the AUC is to 1, the better the model distinguishes between these two categories.

We leverage a dataset from the PPMs of 304 funds, with performance available as of June 2022, that were raised between 2003 and 2013 to train the three algorithms and test them on 72 funds raised between 2014 and 2016, so-called out-of-sample[3][4].

Figure 1 shows the AUC of the three algorithms. Gradient Boosting achieves the highest AUC (0.659) among the three algorithms. Overall, the AUC in the three analyses remains significantly above 0.5

Related insight

- Equities

- Webinar

Watch as our excellent panelists, Fundamental Analysts Fleura Shiyanova and Joachim Hermann, dissect the potential impact of renewed trade tensions, policy volatility and market sentiment swings – all hallmarks of the Trump playbook.

[…]- Equities

- Perspectives

Emerging managers, those who are launching their first or second funds, are often viewed sceptically by investors. However, these perceptions are often rooted in myth, not reality.

[…]- Corporate

- Press releases

Unigestion, the asset manager focused on private equity’s mid-market leaders, has announced the first close of its third Emerging Manager Choice Fund (EMC III) at EUR 275m. This first closing comes at more than two-thirds of the Fund’s EUR 400m target size.

[…]- Private equity

- Perspectives

The start of 2025 has proved something of a rollercoaster ride for investors. Deal making in the first quarter of 2025 did not have the momentum many had predicted at the end of 2024.

[…]