- Equities

- Papers

- Perspectives

Kim Pochon

Principal, Private Equity,

Unigestion

Borja Fernandez Tamayo

Vice President, Private Equity,

Unigestion

Overview

Emerging managers, those who are launching their first or second funds, are often viewed sceptically by investors. They are perceived as risky due to their limited track record as a team, smaller AUM and lack of institutional backing. However, these perceptions are often rooted in myth, not reality. Instead of relying on preconceived notions, investors should assess both hard facts, such as performance data and strategy, and soft factors like team experience, agility, innovation and alignment of interests. By looking beyond the myths, a more nuanced and informed perspective can help LPs answer the billion-dollar question: “Are emerging managers worth the risk?”

While, as with any private equity investment, risks do exist, emerging managers give access to highly attractive opportunities that are often unavailable through larger, established managers. At Unigestion, we have been investing alongside emerging managers for 30 years. During these past three decades we have learned how to take most of the risk of investing in emerging managers off the table. Our recipe is not as spicy as one would think.

Key points

- Emerging managers can outperform established managers with the same level of risk

- Emerging managers create value differently and rely less on leverage and multiple arbitrage

- Allocating to emerging managers as a category can offer attractive risk-adjusted returns for investors

Myth number 1

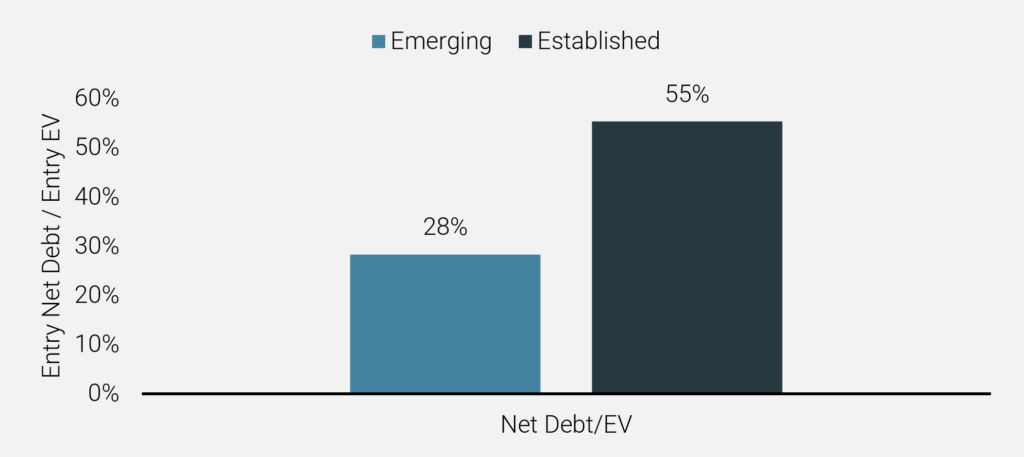

The term “emerging manager” in private equity is a misnomer. Rather than inexperienced newcomers, these managers are typically seasoned private equity professionals with 15-20 years of industry experience who have decided to establish their own firms. Their deep expertise and proven track records make them well-equipped to launch and manage successful investment vehicles. They often bring a distinctive approach to deal-making, and typically employ less leverage in their transactions, as Figure 1 below illustrates, favouring a more conservative capital structure that can better weather market volatility. This approach reflects both their experienced perspective on risk management and their heightened focus on preserving capital.

A key characteristic of these funds is their focus on specific sectors. The founding partners of these firms usually launch funds in industries where they have accumulated deep expertise throughout their careers. This specialised knowledge allows them to identify overlooked opportunities and create value through operational improvements rather than financial engineering alone.

Figure 1: Leverage ratio at entry: emerging vs. established managers

Source: Unigestion. The dataset includes 2,654 realised and unrealised transactions closed between 2000 and 2024

For the founding partners, launching their own fund represents a career-defining opportunity. Unlike established firms where partners might have multiple career options, these entrepreneurs are fully committed to their fund’s success. There is no Plan B. This commitment is further demonstrated through significant personal financial investment: founding partners typically commit 5% – 10% of the fund size from their own capital – and in some cases, even more. This level of personal investment means their wealth is heavily concentrated in the fund’s success, creating a powerful alignment of interest with their limited partners.

Early investors in these funds often have the opportunity to negotiate preferential terms, which can include improved economics, co-investment rights, and greater transparency. This ability to secure advantageous terms can provide significant long-term benefits, especially if the manager goes on to raise larger subsequent funds.

In summary, the combination of experienced leadership, focused strategy, strong alignment of interests, and favorable economics creates a compelling opportunity for investors and can provide advantages in an increasingly competitive private equity landscape.

Myth number 2

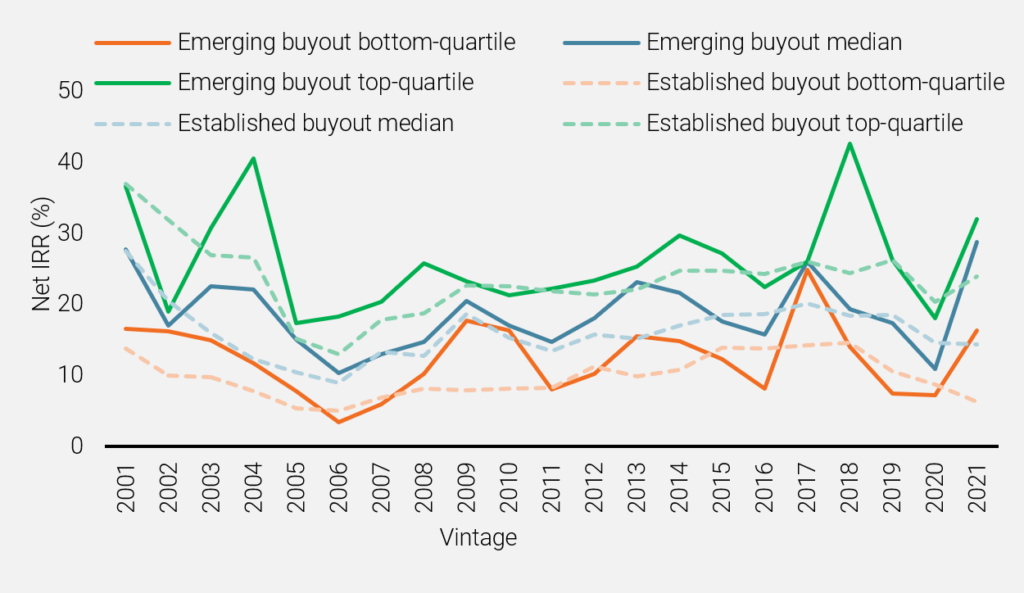

Historical performance data reveals a compelling pattern: emerging buyout managers have consistently outperformed their established counterparts across the return spectrum according to Preqin data (Figure 2). This outperformance was evident not only in the upper quartile of returns but also notably in the lower quartile, suggesting that emerging managers as a category can offer attractive risk-adjusted returns for investors.

Figure 2: Emerging vs established buyout funds performance by vintage

Source: Preqin as of 09.09.2024

The superior performance these funds demonstrated can be attributed to several structural advantages, with fund size being a crucial factor. Emerging managers typically raise smaller amounts of capital compared to established managers and tend to have more concentrated portfolios. With less capital to deploy and more time to create value, these managers can be highly selective in their deal choices, focusing only on the most promising opportunities that align perfectly with their investment thesis and expertise.

One of the most significant advantages emerging managers enjoy is the absence of legacy portfolio management obligations. Unlike established firms that must dedicate substantial resources to managing existing portfolio companies from prior funds, emerging managers can focus all of their attention and resources on identifying and executing new investments. This clean slate allows the investment team to be fully present in the current market. In addition, they are not constrained by historical investment strategies or outdated theses that may be less relevant in the current environment. This flexibility allows them to adapt their investment approach to present market conditions and take advantage of emerging opportunities that established managers might otherwise miss.

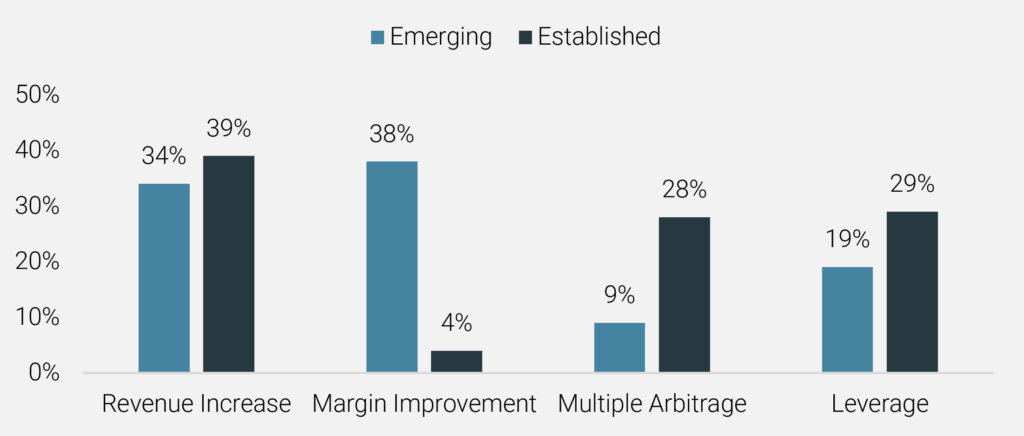

With a smaller number of portfolio companies, the investment team can provide more hands-on attention to each investment, potentially leading to more material operational improvements and value creation (Figure 3). The ability to dedicate significant time and resources to each portfolio company can be particularly valuable in challenging market conditions or when companies require substantial operational improvements.

Figure 3: Emerging vs established buyout funds performance by vintage

Source: Unigestion. The dataset includes 2,654 realised and unrealised transactions closed between 2000 and 2024.

Myth number 3

While the absence of a fund-level track record is often cited as a concern when evaluating emerging managers, this factor alone should not be a show-stopper. In any case, LPs should be careful about interpreting track records. Recent research (Harris, Jenkinson, Kaplan, Stucke, 2023) 1, based on a dataset spanning over three decades and more than 2,300 funds, found that performance persistence in U.S. private equity funds has weakened over time, particularly after 2000. Allocating to emerging managers is not just a matter of diversification, it can also maximise the chance of finding a first quartile fund.

Partnership dynamics serve as a crucial foundation for fund success. This assessment begins with understanding the history of working relationships among partners, examining how their skill sets complement each other, and evaluating their defined roles within the organisation. Special attention should be paid to decision-making processes, as well as the alignment of team culture and values. Similarly, track record attribution requires a granular approach. This involves conducting detailed analyses of individual deal attribution, verifying team members’ specific roles in previous transactions, and performing thorough reference checks with former colleagues and portfolio company CEOs. Understanding each partner’s value-add contributions and reviewing historical investment committee materials provide crucial insights.

Team stability represents another critical dimension and requires careful examination. This includes analysing compensation structures, understanding the distribution of carried interest among team members, and assessing equity distribution within the firm. Additionally, evaluating promotion paths and talent development programs helps predict long-term team cohesion. Again, accurately assessing these factors and associated risks is critical in making informed investment decisions.

For the investor, it’s hard work: dozens of reference calls – most importantly the people not provided on the official reference list – are needed to get a 360-view on the founding partners and their past history. The key lies not just in the evaluation framework itself, but in the investor’s ability to assess and select successful managers across these dimensions.

1 Harris, R. S., Jenkinson, T., Kaplan, S. N., & Stucke, R. (2023). Has persistence persisted in private equity? Evidence from buyout and venture capital funds. Journal of Corporate Finance, 81, 102361. https://doi.org/10.1016/j.jcorpfin.2023.102361

Myth number 4

It may be true that emerging managers typically lack the extensive resources available to established GPs, creating significant challenges across multiple operational dimensions. This resource gap may manifest in difficulties attracting and retaining top talent, building robust operational infrastructure, and achieving the level of institutionalisation investors increasingly expect.

However, several key elements mitigate these challenges. First, emerging managers should focus on attracting entrepreneurial talent deeply committed to building the organisation. These individuals should possess a founder’s mentality rather than corporate thinking – professionals willing to weather uncertainty and contribute beyond their formal roles to ensure the fund’s success and consequently reap the personal rewards.

Second, emerging managers can turn their smaller size into an advantage through greater agility and technological adaptability. By embracing innovative solutions that address operational requirements more efficiently and cost-effectively, emerging managers can build competitive infrastructure without massive capital investments from day one.

Finally, establishing a minimum fund size requirement serves as formal “insurance” against premature operational failure. This threshold ensures sufficient runway to develop track records and organisational capabilities before market pressures become existential threats. With adequate capitalisation, emerging managers can focus on performance rather than mere survival – ultimately creating sustainable investment platforms.

Myth number 5

At first glance, investing in emerging managers might appear to present an asymmetric career risk for institutional investors. If the fund underperforms, one’s judgment might be questioned more severely than when backing established managers. However, this perspective overlooks the substantial strategic advantages and future opportunities that come with being an early supporter of emerging managers.

Being an early investor in these funds provides unique insights into innovative value creation strategies. Emerging managers often bring fresh perspectives and novel approaches to deal-making and portfolio company management. This exposure keeps institutional investors at the forefront of evolving industry practices and emerging market opportunities, demonstrating strategic foresight rather than career risk.

The long-term benefits of early participation are particularly compelling when considering future access rights. Early investors typically secure priority allocation rights in subsequent funds, which can become increasingly valuable as the manager builds a successful track record and raises larger vehicles. These rights often include preferential co-investment opportunities, allowing investors to deploy additional capital alongside the manager on attractive terms.

Furthermore, early supporters have the opportunity to increase their allocation as the manager’s track record develops. This scalability can be particularly valuable for institutional investors looking to build meaningful relationships with high-performing managers. The ability to grow alongside the manager from their first fund creates a strong foundation for a strategic partnership that can extend well beyond traditional limited partner relationships.

Perhaps most importantly, general partners never forget their first investors. This goodwill translates into tangible benefits throughout the relationship, from increased transparency and communication to preferential treatment in capacity-constrained situations. The loyalty factor should not be underestimated – managers often go to extraordinary lengths to ensure their early supporters are well-served, even as their platform grows and attracts larger institutional investors.

Rather than viewing first or second time funds as a career risk, supporting promising emerging managers should be seen as a demonstration of sophisticated investment judgment and long-term strategic thinking.

Key takeaways

Emerging managers, despite their label, are typically led by seasoned professionals with extensive industry experience. Their historical outperformance across return spectrums can be attributed to several advantages: smaller fund sizes enabling greater deal selectivity, absence of legacy portfolio obligations, and strong alignment of interests through significant personal investment.

The research data indicates that the potential rewards of investing with emerging managers can meaningfully outweigh the perceived risks associated with backing a new fund. While the lack of a fund-level track record may raise initial concerns, these can be effectively mitigated through a comprehensive evaluation of partnership dynamics, track record attribution, and team stability.

For institutional investors, backing these managers represents not just a compelling investment opportunity but a strategic advantage in securing valuable future rights and enduring partnerships.

Important Information

INFORMATION ONLY FOR YOU

This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

NOT A RECOMMENDATION OR OFFER

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss.

ASSESSMENTS

Unigestion may, based on its internal analysis, make assessments of a company’s future potential as a market leader or other success. There is no guarantee that this will be realised.

NO REPRESENTATION, INFORMATION SUBJECT TO CHANGE

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends. These reflect Unigestion’s views as of the date of this document with respect to possible future events and are subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Legal Entities Disseminating This Document

United Kingdom

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

United States

In the United States, Unigestion is present and offers its services in the United States as Unigestion (US) Ltd, which is registered as an investment advisor with the U.S. Securities and

Exchange Commission (“SEC”). All inquires from investors present in the United States should be directed to clients@unigestion.com. This information is intended only for institutional clients that are qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

European Union

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

Canada

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

Switzerland

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Related insight

- Private equity

- Perspectives

While exit activity remained subdued in Q4 2025, we continue deliver exits at a consistently high level.

[…]- Private equity

- Perspectives

Monitoring the performance of private equity funds is a critical responsibility for Limited Partners (LPs), as it plays a key role in shaping investment decisions throughout the life of a fund

[…]- Private equity

- Perspectives

Despite geopolitical and macro-economic uncertainties, 2025 has been a largely positive year for investors with public markets posting strong gains.

While investment conditions are far from perfect, inflation globally is moderating, the IMF has slightly upgraded its growth forecasts and many central banks are shifting to a more neutral or easing stance following a significant rate hike cycle that started in 2022.

[…]- Private equity

- Press releases

Unigestion Private Equity, the global specialist in mid-market leaders, is delighted to announce the final close of Unigestion Secondary VI (USEC VI). The fund was oversubscribed at its hard cap of €1.7bn ($2bn).

[…]