Climate impact: the investment opportunity of our lifetime or our legacy to future generations?

Head of Climate Impact, Private Equity, Unigestion SA

Vice President, Private Equity, Unigestion SA

Key Points

- Climate investing has outpaced private equity and venture capital markets. However, the carbon funding gap remains high, as do the financing needs

- Climate investments can deliver top quartile returns as well as quantifiable impact. Our Climate Impact strategy is well positioned to achieve both

- It is time for profitable growth and buyout investments. Transitional businesses remain underpenetrated

- Low carbon premium is just one of the key value creation drivers in our climate track record

- ESG regulation remains difficult to comply with but benefits intentional and quantifiable approaches

Overview

The global economy is taking its first steps into a green revolution that is going to redefine incumbent industries as we know them and create new ones. Climate investment opportunities have already flourished as a result, despite the macroeconomic and geopolitical headwinds. However, for investors pursuing climate investments today, there are multiple challenges: selecting the most attractive segment within the broad climate opportunity, seeking alignment with their own impact objectives, relying on immature track records, benchmarking impact methodologies and keeping up with a fast-changing regulation.

Our 14-year Climate Impact journey at Unigestion has been instrumental in helping us overcome these challenges. We have deepened our expertise, retained lessons learned and enhanced our impact approach, while delivering attractive returns and significant climate impact to our investors.

We are excited to be tapping into the investment opportunity of this century by supporting innovative and high growth companies that will provide the most important legacy to future generations – their survival.

The Climate Tailwind – 2023 under review

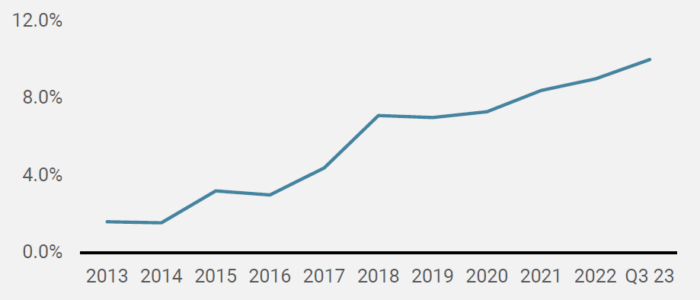

1. Growth in climate investments outpaces broader markets

In 2023, the share of climate investments (as a percentage of private equity and venture capital investments) continued to increase, as shown in Figure 1, defying considerable macroeconomic and geopolitical headwinds. Climate-related private investments outpaced the broader market in 2023 as measured by deal activity and deployed capital. The largest private placement in Europe in 2023, across all sectors, was H2 Green Steel, which raised EUR 1.5bn in equity to build the world’s first green steel plant.

Figure 1: Climate investing as a % of overall PE and VC investments

Source: Pwc

2. Low Carbon Manufacturing is on the rise

Energy Transition and Green Mobility remained the key areas of Climate Impact in 2023, although their share has been declining both in Europe and North America over the last five years. Low Carbon Manufacturing became a new key area of focus in 2023, particularly in Europe where investment levels have doubled. When it comes to newer climate themes, Europe increased its focus on Food, Agriculture and Land use as well as Green Construction. In North America, attention increased for Financial Services, Greenhouse Gas (GHG) data intelligence and GHG capture and storage. In Asia Pacific, Energy Transition and Green Mobility remain the key areas in the Climate Impact space, with Green Mobility enjoying a significant lead since 2022.

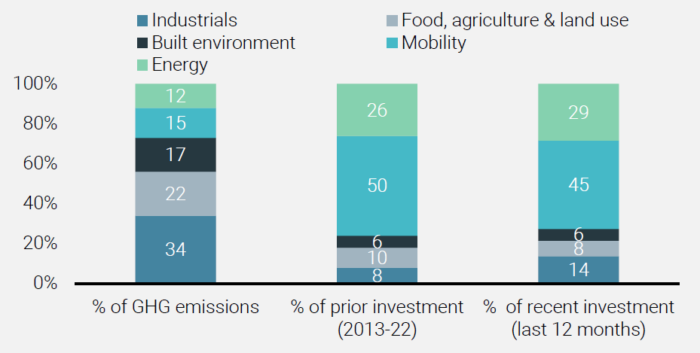

3. The carbon funding gap remains high with new areas of climate impact slowly gaining traction

The mismatch between the global share of GHG emissions and the key areas of Climate Impact across major activities remained in 2023, as shown in Figure 2. Green Mobility, one of the activities with the lowest share of GHG emissions, attracted 45% of climate investments in the period. On the other hand, while Low Carbon Manufacturing (the activity with highest share of GHG emissions) attracted an increase in investment in 2023, it comprises just 14% of the overall climate investments.

Figure 2: Carbon funding gap

Source: Pwc

Carbon removals/capture, green hydrogen, alternative food and biodiversity enhancement are new climate themes that significantly contribute to GHG emissions’ reduction, and have gained traction in 2023. In particular, hydrogen and carbon management recorded the most significant growth in investment inflows since 2019 according to McKinsey. 4. Science-based targets are slowly but surely becoming the net zero reference for private markets

The number of companies validating science-based targets (SBT) doubled in 2023, reaching 4,204. In particular, there continues to be a significant growth in the number of SMEs setting SBTs. Furthermore, the number of companies setting net zero targets increased more than three times (now over 500 companies). However, the real progress on validating SBTs remains slow, with over 2,000 companies having committed to the Science-based Targets Initiatives (SBTi) but not validating their targets in the next 24 months. For each investment in our Climate Impact Fund, we aim to commit to SBTi and validate net zero targets for Scopes 1 to 3 as soon as practical after our initial investment. 5. Dry powder for climate investments has declined but demand for climate financing continues to rise

From 2019 until 2022, the cumulative capital raised for funds related to sustainability and ESG grew threefold, from USD 90bn to more than USD 270bn. It is estimated that climate investments are the core focus for most of this dry powder. In 2023, however, impact and ESG focused funds experienced the same fundraising freeze as the broader private equity market. Furthermore, many investors are still debating whether they prefer a specialised or a general impact strategy in order to address their objectives. Dry powder for climate investments decreased in 2023 as a result, owing to the slower fundraising pace and the robust deployment pace in climate investments over the previous few years.

However, there are no shortage of climate opportunities on the horizon. Achieving net zero emissions by 2050 will mean a major transformation of the global economy and how capital is deployed. For example, McKinsey estimates that, on average, it will require USD 9.2trn in annual capital spending on physical assets for energy and land use systems—about USD 3.5trn more than is spent today[1].

6. Investments in climate solutions have been fully priced but transitional activities remain attractiveConsidering the aforementioned market appetite for climate investments, valuation multiples have risen over the last few years and remained persistently high in 2023 for climate solutions companies. However, the story is different for companies operating in transitional activities[2]. Deep expertise in Climate Impact and high conviction on the success of the green transformation are critical to those pursuing this type of climate opportunity, hence dry powder is selective and entry valuations are more disciplined. In the last 12 months, companies operating transitional activities in our deal flow have shown attractive entry multiples, with an EBITDA multiple typically below 9x.

[1] “The net-zero transition: What it would cost, what it could bring,” joint report from McKinsey, McKinsey Global Institute, and McKinsey Sustainability, January 2022.

[2] Activities for which there are no technologically and economically feasible low carbon alternatives

The Climate Opportunity – key success factors

To fully benefit from the climate opportunity, investors should be aware of the following key trends:

1. The climate opportunity must deliver attractive returns and quantifiable climate impact

As mentioned earlier, significant funding is required to achieve the net zero pathway. That will only be feasible with an attractive investment case. On the other hand, a quantifiable impact approach is paramount to avoid greenwashing risk.

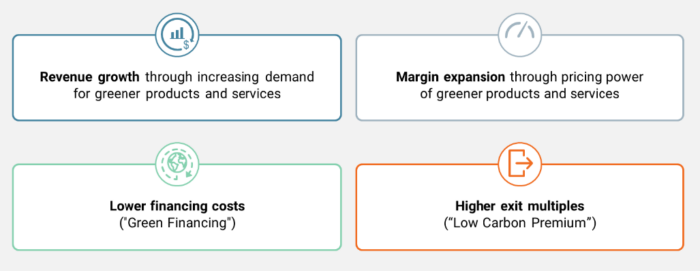

Our experience, based on a 14-year Climate Impact journey, is that the drivers highlighted in Figure 3 will lead to outperformance for climate impact investments:

Figure 3: Drivers of robust returns

Source: Unigestion

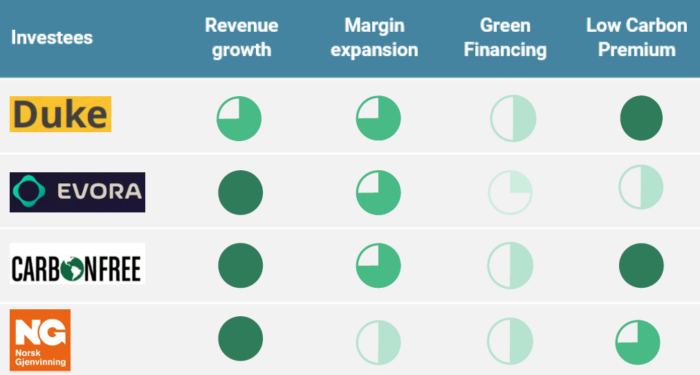

These drivers are reflected across the current portfolio of our Climate Impact Fund as outlined in Figure 4.

Figure 4: Climate Impact Fund – Key return drivers

Source: Unigestion. Refer to the Important Information section at the end of this document, which provides additional information applicable to the material presented. Past performance is not a reliable indicator of future results. For illustrative purposes only.

Quantifying the impact of our investments is a core part of our Climate Impact strategy and therefore also linked to the carried interest of our Climate Impact Fund. Figure 5 summarises the impact thesis for the current portfolio of the Climate Impact Fund.

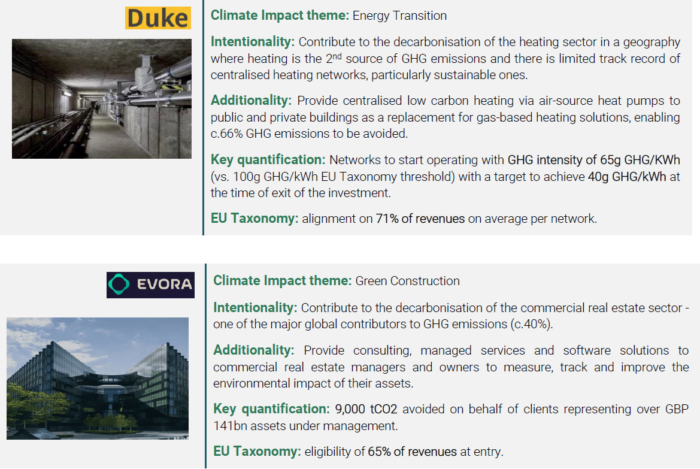

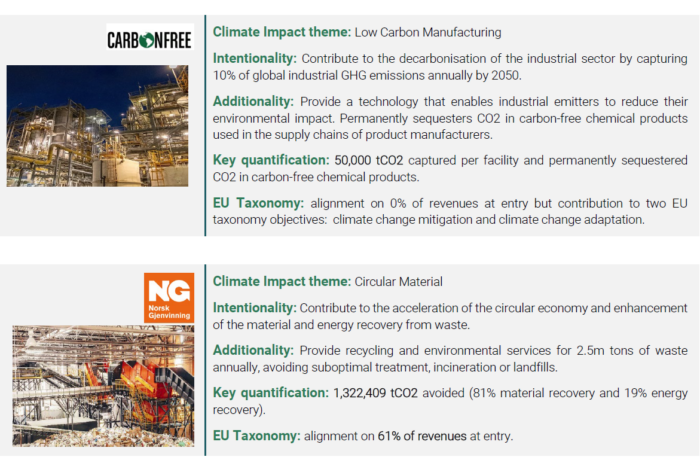

Figure 5: Impact thesis of our current investments in the Climate Impact Fund

2. The climate opportunity cuts across the real economy

Almost every industry in the real economy – from mobility, agriculture to energy storage – is ripe for change. We are in the early days of a green revolution that is going to completely redefine incumbent industries. Our Climate Impact strategy relies on the following climate impact themes listed in Figure 6 and where Unigestion has strong experience in delivering top quartile returns, as well as significant climate impact. Diversification in Climate Impact will enable investors to benefit from broader and uncorrelated success stories.

Figure 6: Unigestion Climate Impact Sectors

Source: Unigestion. Examples of Unigestion’s climate investments listed above

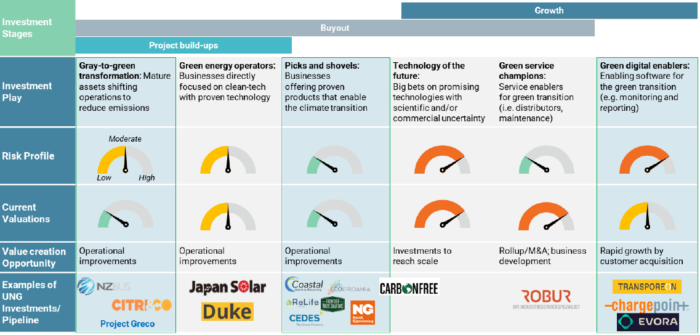

3. The time for buyout and profitable growth companies

While the climate opportunity is spread across several investment stages (see Figure 7), we believe that the most attractive opportunity remains in the buyout and profitable growth stages for the following reasons:

- Consistent returns with reasonable holding periods – our 14-year track record in Climate Impact has achieved a realised return of 2.5x net TVPI and 33% net IRR[3] with an average holding period of four years, no write-offs and only one investment below cost to date (see Figure 9).

- Sizeable investment opportunity – the investment universe is already sizeable today with our strategy having reviewed over 150 opportunities in the last 12 months. Furthermore, this opportunity set is well-positioned to experience high growth in the next few years, due to the substantial amount of capital that has recently been allocated to venture capital and early growth investments. According to Roland Berger, the revenues from climate focused companies globally are expected to grow from USD 5trn in 2020 to USD 12trn in 2030.

- Proven offering and operational performance – commercial scale production or offering is already available or with a clear path with high visibility on hitting performance and costs thresholds. The products and services meet a near team need to customers to make them willing to buy it.

- Quantification of the climate impact – with or without external support, companies in these stages are able to report on their significant climate impact (see Figure 12).

[3] As of 31 December 2023.

Figure 7: Broad range of climate opportunities showing diversified risk profile and value creation focus

Source: Bain & Company. Light blue shaded columns for the most likely opportunities. Pipeline of investments in blue font.

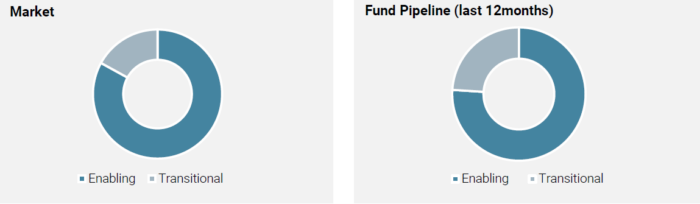

4. Transitional businesses are equally important but understated.

Most climate investments focus on companies providing climate solutions that are expected to prevail in the low carbon economy. However, an attractive opportunity also lies among businesses that have a significant footprint today and need to transition to low carbon. Deep expertise in Climate Impact and high conviction on the success of the green transformation are critical for those seeking to invest in opportunities like these – it is no surprise that dry powder is selective and entry valuations more disciplined for such deals. Furthermore, the climate impact of such transitional activities is also significant and must not be neglected if investors are to ensure the narrowing of the carbon funding gap highlighted earlier in Figure 2.

While we are yet to invest in a transitional business in our current Climate Impact Fund, we have some attractive opportunities in the pipeline (e.g. a green aluminium manufacturer), have reviewed many and historically have invested in this type of company in the past. Indeed, in 2019 we invested in a bus transportation provider in New Zealand, whose green transformation enabled us to secure an attractive exit to a strategic investor in 2022 at 3.8x net TVPI and 71% net IRR. Figure 8 illustrates the under representation of transitional activities against enabling activities in the market (proxied by transactions closed over the last two years recorded in Preqin) over the last two years. Given that our Climate Impact strategy targets both profitable growth and buyout investments, our pipeline is more weighted towards transitional activities than the market.

Figure 8: Transitional activities remain underpenetrated

Source: Unigestion analysis based on Preqin data

5. Climate Impact experience is paramount

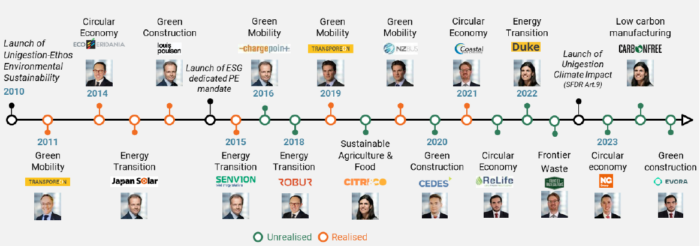

Our private equity team has long recognised the importance of environmental responsibility within our investment strategy. We launched our first environment-focused fund in 2010, followed by an ESG-focused direct mandate for a large client in 2014. Our experience was critical to deliver on both objectives. In our 14-year Climate Impact journey, we have invested close to EUR 250m in 23 climate investments as outlined in Figure 9.

Figure 9: 14 years of Climate Impact Experience

Source: Unigestion as at December 2023. Realised investments shown as orange circles.

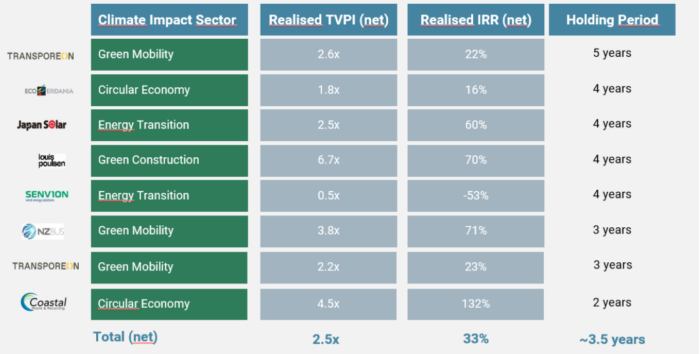

Importantly, a significant part of the track record fully attributable to Unigestion’s private equity team is already realised today. Out of eight investments exited to date, we delivered an aggregated return of 2.5 x net TVPI and 33% net IRR across several climate impact sectors and geographies (Europe, North America and Asia Pacific), with an average holding period of four years. We did not experience any write-offs and only one investment was below cost as set out in Figure 10.

Figure 10: Uncompromised private equity returns

Source: Unigestion as at 31 December 2023

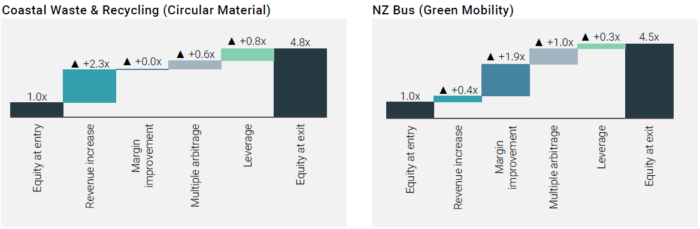

Looking deeper at the rationale behind these attractive returns, one can find similar value creation drivers as highlighted earlier in Figure 4. In the case of Coastal Waste & Recycling – a US-based waste recycling company in which we invested in 2021 – the key return driver was strong revenue growth. This was driven by increased demand for its green services, as showed in Figure 11. We sold the company in June 2023 to an infrastructure investor, achieving 4.5x net TVPI and 132% net IRR. This strong return was underpinned by revenue growth and some multiple arbitrage resulting from the climate tailwinds impacting the company’s industry – the so-called low carbon premium.

For NZ Bus, a New Zealand-based bus transportation provider in which we invested in 2019, the value creation story was slightly different. Given the transitional nature of this business, the low carbon premium played a much more important role in the value generated when we exited. Furthermore, NZ Bus’ key return driver was EBITDA margin improvement resulting from the transformational operational changes executed during our ownership – as shown in Figure 11. We sold this investment in 2022 to a private equity-backed company, delivering 3.8x net TVPI and 71% net IRR.

Figure 11: Value creation of two exited climate investments

Source: Unigestion. Analysis done on the basis of gross returns

As outlined in Figure 4 above, we expect to benefit from similar value drivers in our current climate investments. We also believe that a decline in low carbon premiums will occur over time as climate solutions get more mature, achieving cost parity and high adoption rates. However, this is only one of the value creation levers from which our climate investments have benefited.

Managing an SFDR Article 9 fund

The implementation of the European regulation, Sustainable Finance Disclosure Regulation (SFDR), since March 2021 has triggered a revolution in the impact investing industry. It has forced greater standardisation, transparency and measurability. We are proud to be one of the pioneer asset managers to launch a private equity fund with an SFDR Art.9 classification. As of end of 2023, Pitchbook estimated 214 funds in private markets classified as SFDR Art.9, of which only 55 are in private equity and 31 in venture capital.

15 months into the management of this strategy we are in favour of the quantification of the impact and simpler benchmarking between strategies. However, there have been several challenges, such as in data collection, resource intensity (internal and external) and associated additional costs. Furthermore, the regulatory environment is changing at a very fast pace and asset managers in this sector have to stay on top in order to minimise the regulatory risk. Two years since its implementation, SFDR is currently under review and we expect material changes to be implemented in the next 12-18 months.

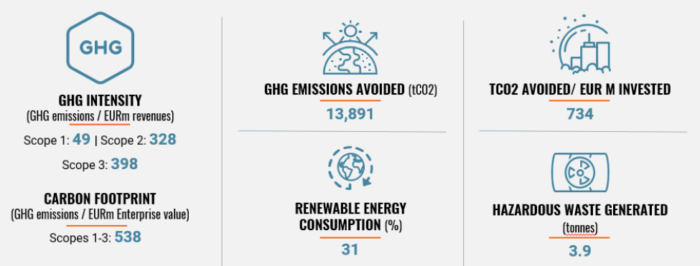

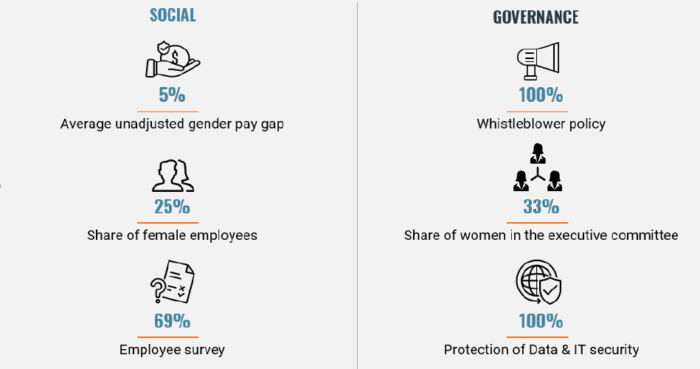

Nevertheless, without this regulatory push and subsequent development of sustainable finance, it would be much harder to quantify and report today on the impact our portfolio is delivering. Figure 12 outlines some of the key climate impact KPIs reported for every investment in the portfolio. Figure 13 shows a sample of a few key social and governance KPIs as part of our assessment on “Do Not Significantly Harm (DNSH)” and “Good Governance”. The evolution of such KPIs will be tracked on a company-by-company basis at entry and annually thereafter. These data reflect the entry point of the portfolio as all the investments in it have been held for less than one year, with the exception of one that is a project build up situation.

Figure 12: Unigestion Climate Impact Fund – Selective climate KPIs

Note: Based on latest available revenues and enterprise values. “GHG intensity Scope 3” based on estimates. “GHG emissions avoided” on an annual basis. “EUR m invested” includes the Climate Impact Fund only. Source: Unigestion as of 31 December 2023 based on investments’ self-reported data

Figure 13: Unigestion Climate Impact Fund – Selective DNSH and Good Governance KPIs

Source: Unigestion as of 31 December 2023 based on investments’ self-reported data

Looking ahead – 2024 outlook

Investment in Climate Impact has now a more solid foundation. Yet a huge amount of capital deployment will be required in the upcoming years to meet the commitments of private- and public-sector leaders around the globe. Identifying and backing the most promising and resilient opportunities in the next few years will affect the long-term prospects of the entire climate solution space. Such investments will also determine our ability to accelerate and achieve at-scale decarbonization in the years ahead.

The new climate themes mentioned earlier – carbon removal / capture, green hydrogen and nature and biodiversity – will continue to expand in 2024. Biodiversity in particular is now on the top of the list, partially driven by the emergence of the Taskforce on Nature-related Financial Disclosures (TFDN), which already accounts for over 300 commitments around the globe. While the real impact of TFDN on biodiversity conservation remains an open question, investors should carefully consider the potential risks and opportunities associated with the biodiversity profile of investments. We have been reviewing investment opportunities seeking to address biodiversity loss but we are yet to find one with the adequate risk return profile. We also expect transitional activities to attract more investments in 2024 as well as more artificial intelligence being used to accelerate energy transition and adaptation.

Momentum seems set to continue in 2024 as governments, corporations and investors are finally taking action and accelerating investment into the Climate Impact sector. In 2023, around 140 countries had proposed or set net-zero targets that cover c.90% global GHG emissions. Government actions – whether in form of mandates (such as emissions reductions), subsidies (such as investment or production tax credits), or market design (such as carbon pricing) — continue to be major catalysts for climate solutions. Despite the political changes expected in several core geographies, we remain confident that Climate Impact will remain high on the government agendas. From private investors’ point of view, the year has started well with some encouraging signs on fundraising. There is scope to believe that impact fundraising can rebound in 2024.

Continued macroeconomic and geopolitical uncertainty means that investors in climate will need to remain disciplined in the years ahead. Investors need to ensure that their investments are able to leverage a wide range of climate tailwinds but also to deliver on critical business fundamentals while simultaneously delivering measurable impact.

We believe our Climate Impact strategy is well positioned to achieve top quartile returns and significant climate impact, despite the uncertain times, for the following reasons:

- attractive initial portfolio of innovative, high growth companies with intentional and quantifiable climate impact and visibility on imminent valuation uplift

- differentiated market positioning, targeting profitable growth and buyout investments

- 14-year of Climate Impact experience

Important Information

INFORMATION ONLY FOR YOU

This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

RELIANCE ON UNIGESTION

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time. Such information is intended to provide you with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf of one or more Unigestion entities will be involved in managing any specific client account on behalf of another Unigestion entity.

NOT A RECOMMENDATION OR OFFER

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Reference to specific securities should not be construed as a recommendation to buy or sell such securities and is included for illustration purposes only.

RISKS

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Unigestion maintains the right to delete or modify information without prior notice. The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, and may experience substantial & sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

PAST PERFORMANCE

Past performance is not a reliable indicator of future results, the value of investments, can fall as well as rise, and there is no guarantee that your initial investment will be returned. Returns may increase or decrease as a result of currency fluctuations.

NO INDEPENDENT VERIFICATION OR REPRESENTATION

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

FORWARD-LOOKING STATEMENTS

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events and are subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. You are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document.

TARGET RETURNS

Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Target returns are based on Unigestion’s analytics including upside, base and downside scenarios and might include, but are not limited to, criteria and assumptions such as macro environment, enterprise value, turnover, EBITDA, debt, financial multiples and cash flows. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

USE OF INDICES

Information about any indices shown herein is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison. You cannot invest directly in an index and the indices represented do not take into account trading commissions and/or other brokerage or custodial costs. The volatility of the indices may be materially different from that of the strategy. In addition, the strategy’s holdings may differ substantially from the securities that comprise the indices shown.

ASSESSMENTS

Unigestion may, based on its internal analysis, make assessments of a company’s future potential as a market leader or other success. There is no guarantee that this will be realised.

No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of this fund and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses.

Unigestion Climate Impact Fund (Climate Impact) has been created as a SCS-SICAV-RAIF in Luxembourg and qualifies as an Alternative Investment Fund (AIF) within the meaning of the law dated 12 July 2013 on Alternative Investment Fund Managers implementing the Directive 2011/61/EU (AIFMD). As a result, units of this vehicle may be offered only to professional investors and may not be distributed on a public basis in or from any country where such distribution would be prohibited by law. This document contains a preliminary summary of the purpose and principal business terms of an investment in Climate Impact. This summary does not purport to be complete and is qualified in its entirety by reference to the more detailed discussion to take place with the AIF. Climate Impact has the ability in its sole discretion to change the strategies described herein. Before making a decision to invest in Climate Impact, you are advised to consult with your tax, legal and financial advisors.

Legal Entities Disseminating This Document

United Kingdom

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (« FCA »).

This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

European Union

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (« AMF »).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

Canada

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (« OSC »).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

Switzerland

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (« FINMA »).

Document issued April 2024.