Private Equity Market Insights

-

Private equity capital raising continued to increase in the third quarter, despite slower investment and exit activity.

-

The development of new types of specialised transactions, such as GP-led fund restructurings, is transforming the secondary market.

-

Demand for innovative new sources of liquidity from both LPs and GPs is likely to fuel continued growth in the secondary market, irrespective of broader market trends.

Overview

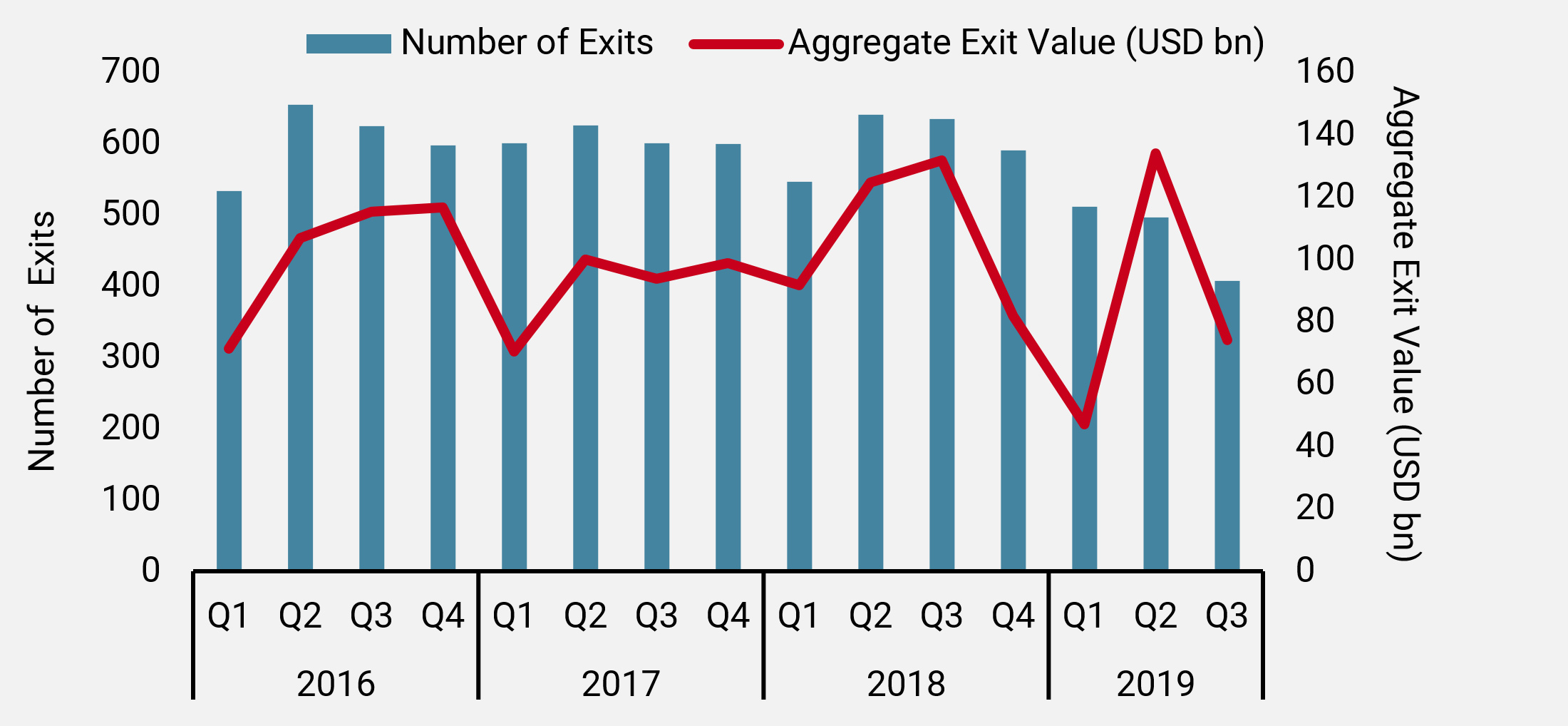

Continuing the downward trend seen in the first half of 2019, global investment activity in the private equity market was again lower in Q3 compared to the same quarter a year ago. Similarly, after a strong second quarter, global exit activity recorded a sharp fall in Q3. However, investors in private equity funds are seemingly unperturbed by market events. Fundraising recorded its largest third quarter total in the last five years, with the large end of the market particularly strong.

Investment and Exits Down, Fundraising Up

The global aggregate value of private equity deals closed during the first three quarters of 2019 was USD 269bn, 25% down on the same period last year1. While contributions by region show volatility by quarter, the overall downward trend is similar across North America, Europe and Asia.

The same story is being told by global exit activity. Despite the high level of exit activity in Q2, the global aggregate value of exits for the first three quarters of 2019 was USD 256bn, 27% down on the same period last year2. The biggest contributor to this fall was IPO volume, which was almost 40% lower.

Nevertheless, this global slowdown in investment and exit activity is clearly not putting investors off. The third quarter showed another uptick in aggregate capital raised by private equity funds, pushing up year-to-date fundraising to USD 417bn3. This is 21% ahead of the amount raised in the same period a year ago. As a result, dry powder inched up higher to USD 740bn.

Figure 1: Value (USD bn) and Number of Exits

The large end of the market continues to dominate the headlines. In the third quarter, firms such as Permira (EUR 11bn) and, in particular, Blackstone (USD 26bn), raised record-breaking funds. Notably, of the private equity firms currently fundraising, only 13% are targeting fund sizes of USD 500m or more, yet this represents more than two thirds of the aggregate capital being targeted4. Thus, the vast majority of private equity firms on the road are the lesser-known, small buyout fund managers.

While the large end of the market continues to dominate the headlines, the majority of private equity firms on the road are small buyout fund managers.

Similarly, while newspapers may find more interest in stories such as the GBP 4bn take-private of UK aerospace and defence supplier Cobham by Advent at 15x EBITDA, the numerous deals at the small end of the market give a more interesting indicator of what is happening in the “real” economy. For example, in May 2019, one of our fund managers acquired an Italian aluminium extrusion die manufacturer for EUR 170m or 8x EBITDA. The company employs 700 people at its headquarters in Italy and sells its technologically advanced products to over 250 customers worldwide in the transportation and construction sectors.

The Evolution of the Secondary Market

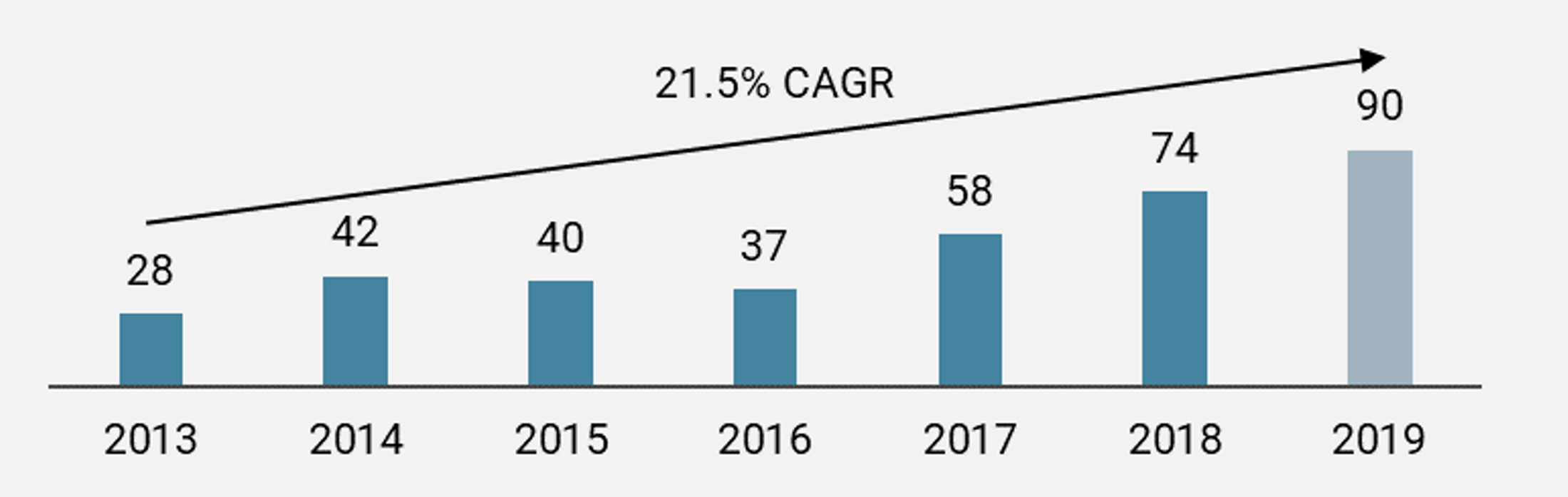

While overall private equity investment activity has been somewhat subdued in 2019, secondary investment activity is on course for a record year. In fact, the secondary market has grown at a CAGR of 21.5% since 2013, more than trebling in that time. This fast-paced growth has raised concern amongst investors that the market is becoming overheated.

Figure 2: Secondary Transaction Volume (USD bn)

On the one hand, average secondary prices have been hovering close to 100% of NAV, suggesting that the discount traditionally expected by secondary buyers has all but evaporated. On the other hand, the secondary market has transformed in recent years with the development of a range of new types of specialised secondary transactions.

The rise of GP-led transactions

Up until around 2012, close to 100% of secondary deals completed were traditional acquisitions of limited partner (LP) stakes in private equity funds where the general partner (GP) had little involvement. In 2018, almost a third of all secondary transactions were “GP-led”. In other words, GPs have increasingly been utilising the secondary market as a proactive fund management tool.

GPs have increasingly been utilising the secondary market as a proactive fund management tool.

The most common GP-led transaction is a fund restructuring, whereby a GP sets up a new “continuation fund” in which it transfers some or all of its portfolio companies from a maturing fund. By doing this, LPs have the choice to roll over their investment into the new fund or exit via the capital from incoming secondary investors.

In theory, this can be a win-win for all parties involved. LPs have the option to get early liquidity at a fair price set by the market. Secondary investors are able to get exposure to potentially attractive, mature assets. Meanwhile, the GP can obtain more time to maximise the value of its portfolio and thus maximise its carried interest payout, especially since it will have reset its incentives in the continuation fund.

In practice, it is never so simple. For example, there are certain conflicts of interest that both LPs and secondary investors need to navigate carefully. When a GP transfers one or more portfolio companies into a continuation fund, carried interest in the mature fund will typically be generated. Secondary investors will often insist that the GP invests most of its crystallised carried interest into the continuation fund in order to maintain a decent alignment of incentives.

There is also the question of which portfolio companies should be transferred to the continuation fund. While both secondary investors and the GP may want to focus only on the most attractive companies, certain LPs might prefer that the entire fund is transferred and thus liquidated.

Secondaries at Unigestion

At Unigestion, we have participated in multiple fund restructurings in the last five years as both an incoming secondary investor as well as an incumbent LP. As a secondary investor, one of the key advantages is that it is possible to do very detailed due diligence on each of the underlying portfolio companies with the full support of the GP. This entails meeting management teams, taking key references and running financial models – the same level of diligence that would be typically done for a direct investment.

At Unigestion, we have participated in multiple fund restructurings in the last five years, gaining access to high quality portfolios at attractive discounts.

In early 2019, Unigestion co-led a secondary transaction consisting of six mature portfolio companies which were hand-picked from three different funds managed by Televenture, a Nordic technology investor. The GP had previously attempted to execute a full restructuring of all three funds (consisting of 22 companies) but this failed due to disappointing pricing. This gave us the opportunity to approach the GP with a more tailored liquidity solution.

This was a complex transaction which required multiple due diligence sessions with the GP and the company management, as well as careful negotiation with the original LPs. However, we ultimately gained access to a high quality portfolio of fast-growing companies at an attractive 18% discount to NAV. After less than 12 months, two companies are already in the process of being sold at an attractive mark up to our entry cost.

We believe that the secondary market will continue to grow, fuelled by the desire of both LPs and GPs to gain liquidity utilising increasingly innovative methods, especially when overall private equity exit activity is trending downwards. By the end of 2018, the total assets under management in the private equity market was over USD 4tn5. Thus, at USD 90bn, the secondary market is still only scratching the surface.

1Preqin

2Preqin

3Preqin

4Preqin

5Preqin

Important Information

This information is issued by Unigestion (UK) Ltd (“Unigestion”), which is authorised and regulated by the UK Financial Conduct Authority (“FCA”). Unigestion is also registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for professional clients, institutional clients and eligible counterparties, as defined by the FCA, and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

It must not be published, reproduced, distributed or disclosed (in whole or in part) by recipients to any other person without the prior consent of Unigestion. The information provided should only be considered current as of the date of publication without regard to the date on which you may access the information. Unigestion maintains the right to delete or modify information without prior notice. This presentation is a promotional statement of our investment philosophy and services and does not constitute an offer or solicitation to acquire, sell or subscribe to any securities or financial instruments described or alluded to herein which may be construed as high risk and not readily realisable investments and may experience substantial and sudden loss including total loss of investment. The securities mentioned in this document may not be authorised for public distribution in certain jurisdictions and are not offered or distributed on a public basis in or from any country where such distribution would be prohibited by law. The investments described herein are not suitable for all types of investors. All investors must obtain additional information needed to evaluate a potential investment and provide important disclosures regarding risks, fees and expenses. Investors shall in particular conduct their own analysis of the risks (including any legal, regulatory, tax or other consequence) associated with an investment and should seek independent professional advice.

No separate verification has been made as to the accuracy or completeness of the data included in this presentation, which may have been derived from third party sources, such as fund managers, administrators, custodians and other third party sources. As a result, no representation or warranty, express or implied, is or will be made by Unigestion as regards the information contained herein and no responsibility or liability will be accepted. The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Past performance is neither guaranteed nor a reliable indicator of future results. The value of investments may go down or up. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. An investment with Unigestion, like all investments, contains risks, including the risk of total loss. Unless otherwise stated, the performance data source is Unigestion.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document does not purport to be complete and is qualified in its entirety by reference to the more detailed discussions relating to the strategies mentioned. Unigestion has the ability in its sole discretion to change the strategies described herein.

This document is being provided to you on a confidential basis solely to assist you in deciding whether or not to proceed with a further investigation of a strategy or Unigestion. Accordingly, this document may not be reproduced in whole or part, and may not be delivered to any person without the consent of Unigestion.

Nothing set forth herein shall constitute an offer to sell any securities or constitute a solicitation of an offer to purchase any securities. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such formal offering documents contain additional information not set forth herein, which such additional information is material to any decision to invest in a strategy.

No information is warranted by Unigestion or its affiliates or subsidiaries as to completeness or accuracy, express or implied, and is subject to change without notice. This document contains forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document.

These materials should only be considered current as of the date of publication without regard to the date on which you may receive or access the information. Unigestion maintains the right to delete or modify information without prior notice.

Charts, tables and graphs contained in this document are not intended to be used to assist the reader in determining which securities to buy or sell or when to buy or sell securities.

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance. The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, sources are Unigestion, Bloomberg and Compustat.