- We expect a continuation in the recovery and see too much pessimism in current growth and earnings forecasts for 2020.

- We see very limited inflationary pressures for three reasons: savings, slack and secular trends.

- We remain overweight growth assets, in particular equities. They should remain supported by a re-rating of growth across forecasts and analysts’ estimates.

- Sentiment is less supportive than before, while valuations are becoming a clear headwind for growth assets.

- Potential risks in Q4 include the US elections, US-China relations, and a pick-up in coronavirus cases.

Overview

The last quarter of 2020 will close an agitated year, holding many of the necessary answers to a successful asset allocation in a period of extraordinary uncertainty. Three elements are currently catching our eye: first, we see overly pessimistic growth forecasts that translate into a 2021 earnings recovery, not 2020. However, we think a greater chunk than expected of this recovery will happen in Q4 and that this growth re-rating will provide a material support to the equity markets. Second, we see rumours of inflation being on the rise: we disagree and still think that inflation should once again undershoot targets and forecasts this quarter. This will keep central banks on the supportive side for longer than expected. Finally, we see three potential volatility sources: valuations are stretched post the summer rally, while positioning has considerably normalised; we think the US election could bring its lot of shaky days; lastly, we think that the China issue lies in front of us, not behind us. The health situation also remains preoccupying. All of these factors will require staying nimble while being focused as much as possible on fundamentals – with an overweight in equities – rather than on the noise.

Part 1 – The Underated Economy

As initiated by the Fed and other central banks, the intense fiscal stimulus has created one of the fastest recoveries the world has ever experienced. Now, the slowdown in this growth momentum brings its own set of questions that investors need to answer: Will the recovery continue? If so, how strong can it be? If too strong, can it trigger an inflation wave leading central banks to adjust their market-supportive policies?.

We expect a continuation in the recovery and see too much pessimism in growth and earnings forecasts for 2020. We fail to see strong prospects for inflation and, more importantly, see no turn in the position of central banks.

The Macro Recovery is Probably Under Anticipated

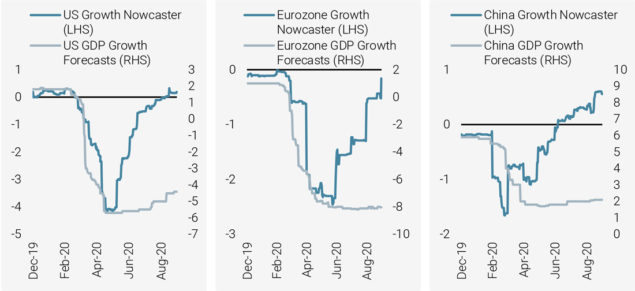

Growth prospects at the end of June looked gloomy. Back then, professional economists expected growth of -5.6% in the US for 2020 and -8% in the Eurozone. Since then, we have seen a wide stream of improving data giving a clear indication of a V-shaped recovery. Both of the Fed’s nowcasting indicators are showing higher growth in Q3 (+20% for the NY Fed’s and +30% for the Atlanta Fed’s). However, as of the end of September, economists’ forecasts had not been revised up in a significant manner, except in the case of the US (GDP growth revised from -5.6% to -4.7%).

We disagree with the tepid enthusiasm of economists. As highlighted in Figure 1, our proprietary Growth Nowcasters point in one direction – that of a rapid economic improvement across the US, the Eurozone and China. We firmly believe that China is on the way to a stronger recovery than expected: our Chinese Growth Nowcaster has reached a very high level (+0.6 standard deviation). At the same time, the US one has just climbed its way back into positive territory, while the Eurozone’s is following suit. This leads to a paradox that is illustrated in Figure 1: the majority of data hints at an almost complete normalisation of economic activity over Q3-Q4 while the average economist remains extremely cautious, barely revising up their growth forecasts.

Figure 1: Daily Growth Nowcasters Per Country vs. Private Economists’ GDP Growth Forecasts

Source: Unigestion, Bloomberg, Ravenpack. Data as at 30.09.2020.

Source: Unigestion, Bloomberg, Ravenpack. Data as at 30.09.2020.

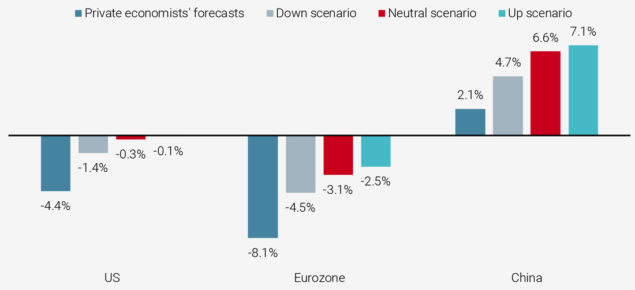

Investors need to take a stance on this issue. Ours is that we should see positive surprises throughout Q4 when it comes to the growth situation. Figure 2 provides the GDP growth forecasts derived from our nowcasting indicators for the three major zones, using three scenarios for Q4 (negative, neutral and positive). Even the gloomiest of our forecasts (a scenario implying negative GDP growth in Q4) suggests higher GDP growth than that forecast by economists. We therefore see the potential for positive surprise until the end of the year.

Figure 2: Nowcaster-Implied GDP Growth Scenario for 2020 Compared to Private Economists’ Forecasts

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

Reading note: the “Down” scenario implies a deteriorating Q4, “Neutral” a stabilisation in Q4 and “Up” a further economic improvement.

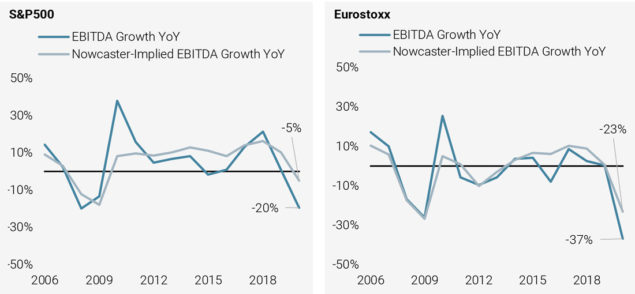

We have been calling a stronger recovery than generally expected for some time now and we still think that the Q3 earnings season will clearly show the undervalued strength of it. Consistent with the pessimism of economists, the earnings growth expectations of analysts are low. Figure 3 illustrates an important element about them: in the case of both the S&P 500 and the Euro Stoxx, analysts expect a recovery for next year while remaining pessimistic for this year. Consistent with our growth scenario, we disagree with them and expect a positive revision to these numbers. Consequently, we see room for positive surprises on the equity front, as 2020 will probably not be as bad as what they seem to think.

Figure 3: Expected Earnings Growth vs. Nowcaster-Implied Earnings Forecast Per Year

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

No Inflation Surprise in the Medium Term

The cautious investor, even if convinced by the intensity of the recovery, will still be worried about intensifying rumours that inflation will make a comeback in the economy. If we are of the opinion that growth is underestimated, we would expect it to return with very limited inflationary pressures for three reasons, the three “S’s” of inflation:

- Slack: there is still a significant amount of slack in the world economy. Production capacity utilisation rates are low (71.4% in the US and at 72.1% in the Eurozone) and unemployment rates are declining while still being more elevated than six months ago. We agree with the Fed that about 1% of the workforce in the US should remain unemployed by the end of next year. We would need to see this slack gone before we see higher inflation.

- Savings: saving rates have massively increased since the start of the lockdowns and have only slightly retreated across developed economies (17% in the US). Corporates are also saving, increasing their cash holdings (+2% so far in 2020). This will dampen and smooth the impact of any fiscal stimulus – before it hits the economy full speed, it is likely to take time.

- Secular trends: beyond these cyclical elements, the crisis has accelerated secular trends instead of curbing their pace. The digitalisation of the world economy is not an inflationary factor – quite the opposite actually. This factor is, in our view, a key medium-term determinant for inflation.

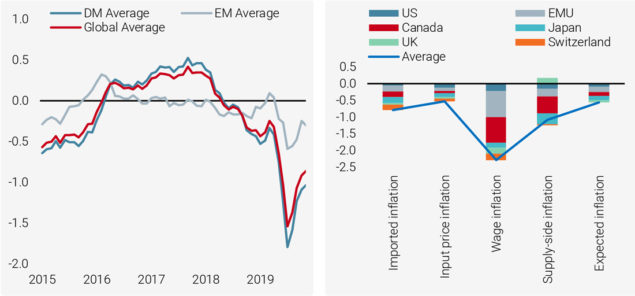

All of that finds ample reflection in Figure 4, which illustrates our Inflation (surprise) World Nowcaster over recent months. For now, it remains in negative territory despite a tepid recovery rooted in the recovering macro data that our Growth Nowcasters are capturing. Having said that, the three “S’s” are echoed by the most macro part of our indicator (wage and supply-side inflation). In our opinion, we need to see these recover before we can start talking about a genuine inflation tide. This will not happen in Q4.

Figure 4: World Inflation Nowcaster (Left) and Breakdown by Source of Inflation (Right)

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

Central Banks Will Remain on the Economy’s Side

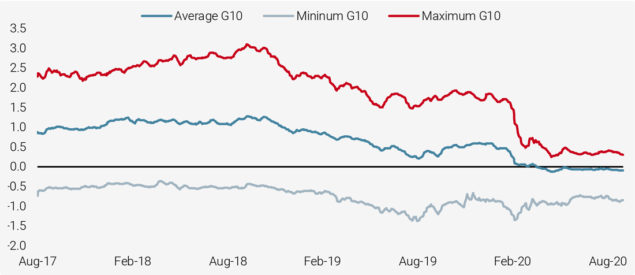

With the massive fiscal stimulus unleashed by a large number of governments, short-term rates need to remain low. Many governments have financed a substantial part of their pandemic package using short-term bonds such as, in the case of the US, T-bills. These bonds are heavily influenced by the evolution of the Fed’s decision rate. In addition, the economy itself needs at this stage all the stimulation it can get. Figure 5 shows the recent evolution of the market’s expectations for future central bank decision rates in the G10 for the next two years. Since 2017, this average expected rate has declined from 1% to 0%. The highest decision rate (New Zealand) has collapsed from 2.5% to 0%, leaving Norway as the highest decision rate of the G10 group (0.5%). Not only have rates been lowered by central banks, they have also converged towards the same level: it is now hard to expect any hike over the next two years given the current level of uncertainty – something that is clearly well understood by market participants.

Figure 5: Central Bank Expected Decision Rates in the G10 Universe (Average, Minimum and Maximum)

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

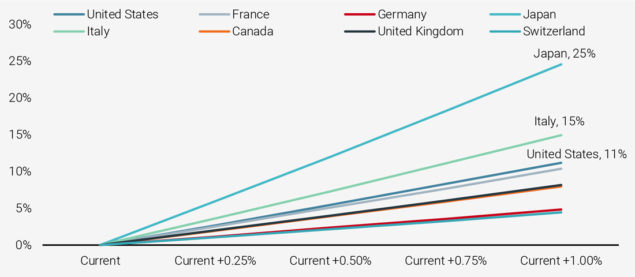

The Fed has made this quite clear in its latest statement: longer-term rates (e.g. 10-year rates) will also be kept low for the foreseeable future. As spelt out in the FOMC’s September report, central banks are likely to seek inflation instead of fighting against it. The Fed’s official change in objective to “inflation moderately above 2% for some time so that inflation averages 2% over time” is a pledge in that direction. Also, now that government debt has increased significantly, it will become harder for the government to keep this debt under control if longer-term rates are on the rise. Figure 6 shows a simulated 10-year forward evolution of debt-to-GDP ratios as a function of increasing longer-term rates: the higher the debt-to-GDP ratio, the stronger the impact of rising rates. In the case of Italy, a 1% increase in rates would lead to an increase in the debt-to-GDP ratio of 15% in 10 years. Even if not as extreme as Italy, the US would see their debt ratio rise by 11%. Think of the actions of the BoJ over the past 20 years: a strong indication for investors regarding the future of monetary policy, with low long-term rates for long as nobody can afford higher rates.

Figure 6: Simulated Increase in Debt-to-GDP Ratio as a Function of Rising Longer Term Rates over the Next Ten Years

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

Reading note: the projected debt/GDP ratio across countries are obtained from the following classical equation to describe the evolution of this ratio: Debt ratio at time t = ((1+rates)/(1+nominal growth)) x debt ratio at time t-1-primary deficit at time t. The parameters have been chosen consistent with IMF data and projections from the 2019/2020 world economic outlook reports. Interest rates are assumed to be kept around August 2020 levels.

If we were in 2017, we would be calling this period a Goldilocks period (solid growth without inflation) and would recommend to overweight growth assets. But we are in 2020 and the enthusiasm coming from the macro picture needs to be curbed because as we approach year-end we see a rather long list of potential volatility triggers.

Part 2 – Volatility Triggers Looming In

Sentiment Is No Longer a Tailwind

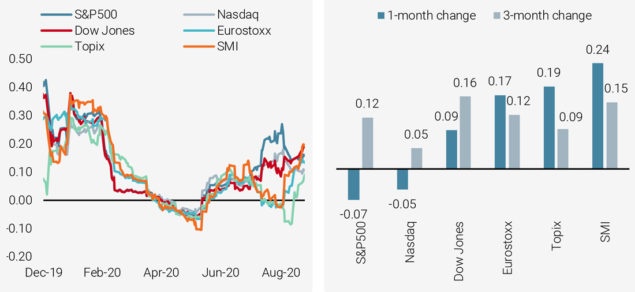

Entering into the summer, investor positioning in equities was low, despite the strong equity performance of Q2. At that point, we saw this sentiment-related indicator as a potential tailwind for equities. Equity markets had a hot summer as hedge funds increasingly bought into the recovery story, raising their equity beta. In the first few days of September, this beta had reached its highest point since the lockdowns, as shown in Figure 7. Since then, positioning has ceased to be a tailwind for markets. As illustrated, it entered into a period of reshuffling, with the exposure to technological stocks reduced and reallocated elsewhere. This reshuffling towards value cushioned the drop in these stocks in September. The conclusion of this analysis is that sentiment is not as strong a supportive factor for stock markets now as it was prior to the summer. If then we expected positive surprises from it, now, we expect the earnings season to takeover that role. Meanwhile, a certain rotation seems to have started in the equity space, with value getting marginally more traction.

Figure 7: Hedge Fund Beta to Regional Equities (Left) and Recent Changes in these Beta (Right)

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

Valuations are a Clear Headwind, If Not a Trigger

Beyond the ups-and-downs of sentiment, one potential source of concern for the rest of the year is asset valuations, as the opportunities we saw at the end of June have deteriorated following a strong summer run. Whereas developed and emerging market equities were inexpensive three months ago, they are now closer to fair value. At the same time, other growth-oriented assets such as credit and cyclical commodities remain fairly valued to modestly expensive, while hedging assets such as duration, inflation breakevens, and gold are also fairly valued to expensive. Altogether, this cross-asset perspective paints a cautionary picture: without any obvious opportunities, the risks are at the forefront.

Figure 8: Cross-Asset Valuations

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

Source: Bloomberg, Unigestion. Data as at 30.09.2020.

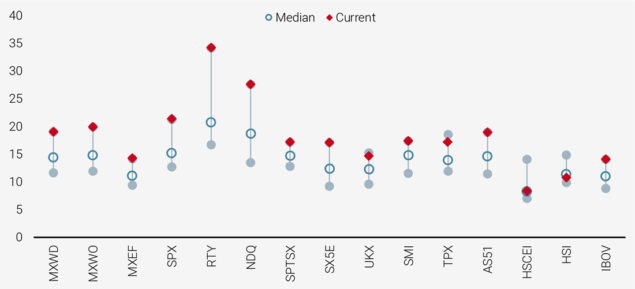

Digging a bit deeper and taking an equity-specific perspective, valuations remain a concern when we look at equity indices. Nearly all markets are above their 90th historical percentile when considering their price-to-earnings ratio on a next-twelve-months (NTM) basis. By this metric, Chinese equities (HSCEI and HSI) appear the most attractive but are acutely exposed to a deterioration in US-China relations (see Figure 9).

Figure 9: NTM P/E by Equity Index

Source: Bloomberg, Unigestion as of 30.09.2020.

Source: Bloomberg, Unigestion as of 30.09.2020.

Reading note: ranges denote 10th to 90th percentiles based on full history.

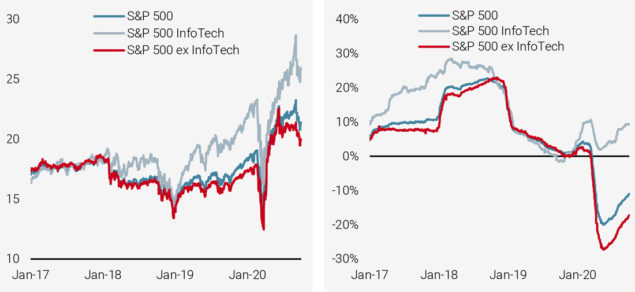

It is important to keep in mind that these historically high valuations are not necessarily irrational: low rates across bond maturities, a massive amount of asset purchases from central banks, and a global economic recovery have naturally fed equity buying. The lockdowns have also put into sharp focus the competitive advantages of “new economy” firms over “old economy” ones. For instance, valuations in the technology sector have started to raise eyebrows to an extent that the 2000 dotcom bubble burst comes to mind. It is clear that multiple expansion in the technology sector has outpaced others. However, earnings growth here has also outpaced that of other sectors and has indeed remained positive on both a last-twelve-months and next-twelve-months basis.

Figure 10: NTM P/E (Left) and NTM EPS YoY Growth (Right)

Source: Bloomberg, Unigestion as of 30.09.2020.

Source: Bloomberg, Unigestion as of 30.09.2020.

Downside Triggers are Gathering for the End of The year

While valuations may not be the cause of a market sell-off, they could act as an accelerant should there be a spark. Looking ahead to the upcoming quarter, we see three potential triggers: US elections, US-China relations, and a pick-up in coronavirus cases that could lead to another round of wholesale lockdowns.

-

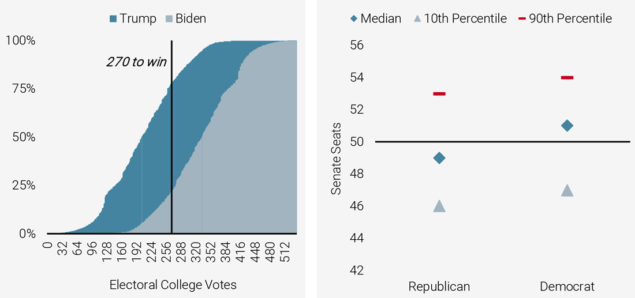

- In our view, the risks emanating from the US elections are not the ones that typically concern investors, such as changes in tax policy, spending and its impact on US yields, etc. Rather, we see potential uncertainty about the outcome, especially for the presidential election, as the eminent risk. Given Senator Biden’s healthy lead in polls, the relatively low number of undecided voters, and President Trump’s poor marks on the coronavirus response thus far, we expect Biden will win the presidency. Of course, there is still a month before the election and an October surprise is not yet off the table. However, as Figure 11 shows, Trump’s chances are low: according to Fivethirtyeight, there is currently a 21% chance he will earn the 270 Electoral College votes needed to win (vs a 78% chance for Biden). Polling has remained stable with Biden’s advantage over Trump remaining in the 8%-10% range, a stark contrast to 2016 when Clinton’s polling lead over Trump contracted to less than 1% at times and never exceed 8% in the months before the election.

-

- Moreover, who will control the Senate is the key question; as a potential President, Biden would be limited to enact policy if Republicans continue their hold on the upper house of Congress. Currently, control of the Senate largely remains a toss-up. While forecasts from Fivethirtyeight give Democrats a 62% chance of taking control of the Senate; the results will depend on just a couple of key close races. Indeed, their median forecast has Democrats holding just a two seat advantage over the Republicans. Nevertheless, any majority control is likely to be thin, making massive policy changes (like a complete rollback of corporate tax cuts) unlikely. Thus the crosscurrents for markets are somewhat offsetting (partial rollback of corporate taxes, increasing spending especially for infrastructure, less mercurial foreign policy) of the election results. However, Trump has refused to commit to honouring the results of the election (including during the first presidential debate), expressing doubts about the reliability of mail-in voting, which will play a large part in the election due to the coronavirus. A disorderly transition (assuming Trump loses) creates uncertainty about the future path of policy and would weigh on investor sentiment.

Figure 11: Cumulative Probability for Electoral College Votes in US Presidential Election (Left) and Forecast for US Senate Seats by Party (Right)

Source: Fivethirtyeight, Unigestion, as of 30.09.2020.

Source: Fivethirtyeight, Unigestion, as of 30.09.2020.

-

-

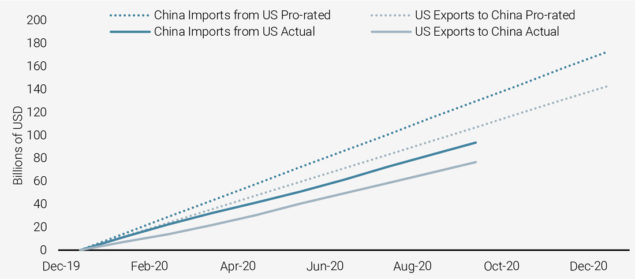

- Another key source of risk for the upcoming quarter is US-China relations. In addition to recent wrangling over the likes of TikTok and WeChat, the first year of the two-year Phase 1 trade deal will be coming to a close. As part of the agreement to lift some tariffs, China agreed to purchasing a fixed amount of US goods and services in 2020 (USD 173bn using Chinese import statistics, USD 143bn using US export statistics). As Figure 12 shows, if purchases continue at the pace they have kept so far, China will fall far short of their commitments. While there may be a diplomatic path that would avoid the reinstatement of tariffs, there is a strong possibility that the Trump administration will move to re-impose tariffs given that China did not meet its commitments. Such a move would then restart the trade war that has mostly faded from investors’ minds.

-

Figure 12: Exports and Imports Comparison to Trade Deal Commitment

Source: Bloomberg, Peterson Institute for International Economics, Unigestion, as of 30.09.2020.

Source: Bloomberg, Peterson Institute for International Economics, Unigestion, as of 30.09.2020.

-

-

- Finally, the rise in new coronavirus cases globally continues unabated and presents a tail source of uncertainty. Following the lockdowns seen earlier this year, governments are now choosing to take surgical, targeted approaches to deal with outbreaks. Local lockdowns, mandatory masks, or limits on large groups are all ways to manage the pandemic, and the rate of new deaths has been flat for some time. A successful vaccine would be a significant upside surprise, as the uncertainty that has kept various sectors of the global economy contained would fade. However, until there is a vaccine, this uncertainty will linger, especially since there remain many unanswered questions about the virus itself. We therefore continue to keep a close eye on the evolution of the pandemic, even if we do not think it currently presents a likely threat to the global economy and markets.

-

Conclusion

In Q4, we expect trend to outpace volatility. The re-rating of growth across forecasts and analysts’ estimates should be a medium-term supportive factor for growth assets. For that reason, we think it still makes sense to remain overweight growth assets, with a preference for equities. We are also of the opinion that the last quarter of the year will not be a straight line: the volatility triggers listed above should affect the pricing of markets as uncertainty will mutate into risks or into opportunities. Our overall message remains the following: keep your eyes on fundamentals as the noise is likely to get louder and, in our opinion, misleading.

Important information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission. Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN). Unigestion SA has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against Unigestion SA.

Document issued: October 2020.