Recent price action has reminded market participants that trees don’t grow forever, and often require some pruning to continue growing. In July and August, a rising tide lifted all boats on smooth summer seas but September has brought crosscurrents and choppy headwinds. Is it time to brace for rougher swells, or will an Indian summer offer markets a sufficiently benign environment to keep on thriving?

Sleep With One Eye Open

The link between monetary and fiscal support has rarely been so tight and necessary. Without it, the world economy would have slipped into what could have been one of the worst recessions and longest market shocks on record. The swift and gigantic global response from policy makers not only prevented such an event, it also allowed a rapid reversal in economic activity and a revival in financial markets. And the improvement is meaningful. Our proprietary Growth Nowcaster – a point-in-time systematic indicator of aggregated economic activity – currently indicates a broad-based recovery, albeit showing signs of stabilisation in the last few weeks. Diffusion indices – measuring the proportion of improving/deteriorating data – have converged at 50% after reaching 75% on average in July and August. Other signs of this stabilisation can be found in various public macro indicators including surprise indices and Baltic Dry freight activity and railway transportation, corroborating central bank declarations that the pace of the recovery has been losing steam. In light of this fading macro momentum, looking forward, we can expect support to remain alive and well for the foreseeable future. Major central banks recently held their respective monetary policy meetings and we believe the outcomes remain very supportive, both for the real economy and financial markets. In the US, the FOMC meeting, held last week, leaves no room for doubt: liftoff in rates will not happen until employment reaches full capacity and inflation runs for some time above their 2% target. This second element is a new addition to forward guidance and makes it likely that monetary action will remain very accommodative until at least 2023. Dot plots show a great level of homogeneity amongst voters with all but one seeing no rate hikes until 2022, and all but four until 2023. As a result, the current pace of asset purchases should remain intact for the next two years at least, or one year before potential liftoff. Such guidance is extremely positive, as it removes uncertainty and provides market participants with visibility over a medium-term investment horizon. In Europe, both the ECB and the BOE confirmed their willingness to increase support, invaluable help at a time when the health situation is deteriorating and political measures are becoming more stringent. The BOE recently changed course, surprisingly considering negative interest rates for the first time in its history, as the spectre of a messy no-deal Brexit resurfaces. Expectations for asset purchases also indicate another GBP 100bn increase in November, as tail risks are increasing, jeopardising the longevity of the recovery. In continental Europe, the ECB delivered the same message: economic projections for 2020 have been revised up, inflation pressures remain lacklustre while the balance of risks to growth are tilted to the downside, primarily due to the resurgence of virus cases across the Euro area. The scale of the Pandemic Emergency Purchase Programme (PEPP) is likely to be raised by year-end to meet additional financing needs from governments and corporations. As flows – or guidance – matter more than inventory, i.e., already known and discounted information, we believe that central banks will continue to increase accommodation in the months to come to meet growing fiscal needs, support growth and employment, and provide a stable and dependable framework for financial markets. This is a strong positive for assets in general, and for riskier premia in particular. So far in September, sentiment has been in the driver’s seat, pushing volatility higher and risk assets lower, albeit heterogeneously. Short-term realised volatility (15 days) on the Nasdaq Composite index has more than tripled over the month, jumping from 12% to 38%, its highest level since March. Over the same period, the same measure barely moved on the Euro Stoxx 50 and S&P 500 indices, hovering around 18% and 17%, respectively. Implied volatility, a measure of the cost to protect against adverse market scenarios, remains elevated in light of the upcoming political events. The S&P 500 put call ratio (measuring the proportion of traded volumes on puts vs. calls) traded back to Q2 levels, yet another indication that money managers have put on their life jackets to face rougher seas. The correction observed in US assets is thus more technical than fundamental, affecting mostly risk premia where optimism and positioning have reached extreme levels. We are of the view that, in spite of supportive macroeconomic and policy support, the road to higher ground will be bumpier than it has been over the summer. Elsewhere, momentum has faded more than it has reversed. Credit remained largely unaffected by market jitters, meaningfully outperforming equity counterparts: in the US, the Barclays US High Yield index is only marginally down month-to-date while the S&P 500 is down 4%. Historically, it should have dropped about 2%. The explanation confirms the non-fundamental nature of the correction and the lack of rotation. In the near future, political risk is set to be the main sentiment driver. In the US, the result of the presidential elections through three main elements will guide the path of assets in the weeks to come: the stance on fiscal policy, the tax environment and foreign affairs. The three will have broad implications on risk appetite, and more specifically on certain sectors, such as technology and healthcare. Various polls are indicating a Democrat victory may have weighed on technology sentiment of late, and is likely to continue as election day gets closer. In Europe, Brexit came back to the forefront and is very likely to add to the fragility and volatility of European assets. Although the probability of a deal has diminished, it cannot be completely discarded, but it will probably be surrounded by elevated headline risk, taking its toll on financial assets, with currencies on the front line. Fundamentals remain sufficiently supportive to envisage a positive year-end for most assets. With governments backstopping Main Street from falling back into recession and central bankers ready to do whatever it takes to support growth, we stick to our medium-term view that risk assets, especially equities, should benefit from such an environment. Real yields are set to stay deeply negative, pushing investors to deploy cash in higher yielding risk premia to escape the value erosion trap created by policymakers, so far successfully. Political potholes could shake sentiment temporarily and lead us to remain partially hedged against tail risks.What’s Next?

Fundamentals remain strong, despite a slowdown in the second derivative

Is sentiment at risk?

Positively exposed

Unigestion Nowcasting

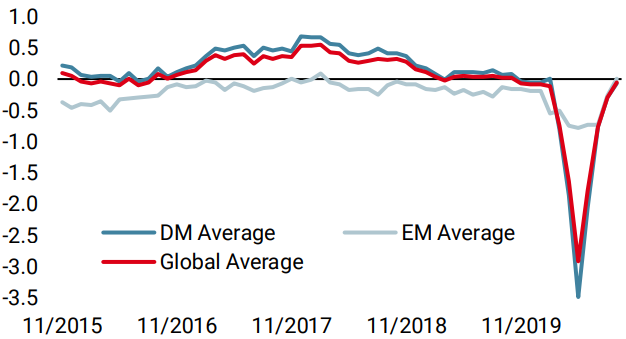

World Growth Nowcaster

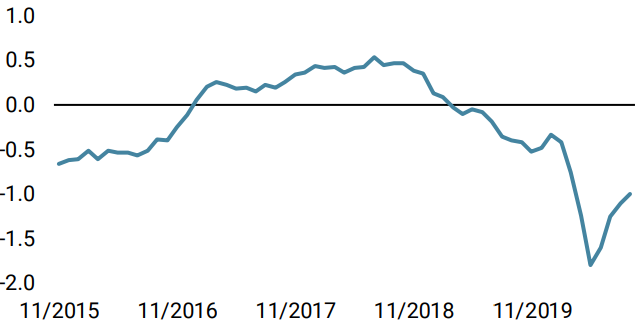

World Inflation Nowcaster

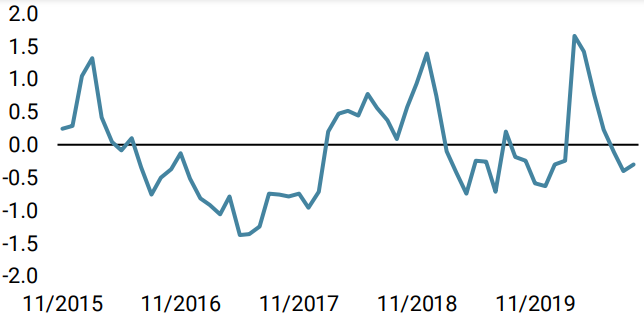

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster rose last week as a fresh batch of solid US, Canadian and Chinese data was released.

- Our World Inflation Nowcaster was stable for another week, as limited inflation pressures surfaced in the data.

- Last week, our Market Stress Nowcaster remained stable in spite of negative equity momentum, highlighting limited appetite to increase hedging positions.

Sources: Unigestion. Bloomberg, as of 18 September 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).