Private Equity Secondaries: The Opportunity of the Decade?

-

We expect the impact of COVID-19 to be significant in private equity markets in the months ahead.

-

Secondary prices and volumes are likely to be heavily impacted before bouncing back next year.

-

We believe that the current market turmoil will present some excellent opportunities for the experienced secondary investor, particularly at the smaller end of the market.

Overview

COVID-19 has dominated the news headlines in recent weeks and we can expect to see more of the same in the months ahead. In addition to the humanitarian toll, which has been immense, the outbreak has had significant implications for global financial markets. While the main focus so far has been on equities, bonds, commodities and currencies, the impact on private equity markets, which are much less liquid, will be felt in the months ahead.

The global financial crisis (GFC) of 2007/08 presented investors with a once in a decade opportunity to invest in secondaries at highly attractive valuations, with investors ultimately rewarded with outstanding returns. In this paper, we assess if there are any similarities between the GFC and the current crisis and where potential secondaries opportunities may lie.

Are there any parallels to be drawn between the GFC and the current crisis?

In 2007/08, a negative shock in the US housing market was the catalyst for a financial crisis that spread from the US to the rest of the world through linkages in the global financial system. While the catalyst for the crisis is different this time, the strong global economic growth, robust financial markets and over-inflated valuations heading into this crisis represented very similar conditions to those prior to the GFC. Nevertheless, we are navigating very different conditions and investor expectations this time around. For example, there are several sectors such as travel, restaurants and leisure where revenues will be close to zero for a number of weeks as a consequence of the lockdowns in many countries. Having said that, observations from the GFC can still be relevant, when adjusted to the new environment.

What does this mean for the secondary market?

We believe that the current crisis will spark exceptional secondary opportunities ahead. The crisis will uncover different weaknesses from different investors in different timeframes, hence there is a need for investors such as ourselves to be ready to seize both short term and long term opportunities.

A majority of the current Unigestion team (including the Investment Committee) worked together during the last financial crisis. We therefore have the experience to understand and exploit the right secondary opportunities in a crisis environment at the right time.

Who were the sellers during the GFC?

The key sellers and the main drivers of deal volumes during the GFC were distressed financial institutions, such as banks and insurance companies, selling off their own balance sheet portfolios. This was mainly due to a need for liquidity, for regulatory requirements, as well as for equity underpinning reasons.

At the smaller end of the market, we saw sellers ranging from overcommitted family offices to hedge funds suffering large redemptions as a result of the financial crisis.

Who will the sellers be this time?

In recent years, the biggest investors in private markets (private equity, private debt and infrastructure) have been large pension funds, insurance companies, financial organisations, sovereign wealth funds and pools of high net worth private clients.

Heavy inflows into private markets were already causing the build-up of certain risks which are set to intensify during the COVID-19 crisis.

Prior to the COVID-19 crisis, we already saw certain risks building up, not least because the heavy inflows into the asset class caused investors to lower their guard. Such risks included:

- The excessive use of leverage:

-

- by fund managers at the company level to finance highly priced acquisitions,

- by fund managers at the fund level to bridge capital calls and investments, and

- by secondary investors at investment level in an attempt to boost returns in a high purchase price environment

- Aggressive over-commitments based on strong historic distributions and growing valuations, especially into venture capital and large buyout funds

- Aggressive deferred payment mechanisms used by secondary players

These risks are now materialising. As a result, certain investors will be under pressure to seek liquidity solutions in the secondary market. We believe that secondary opportunities will originate not only from the investors mentioned above, but also secondary funds and fund managers who need capital to support their portfolio companies.

What will happen to secondary prices and volumes?

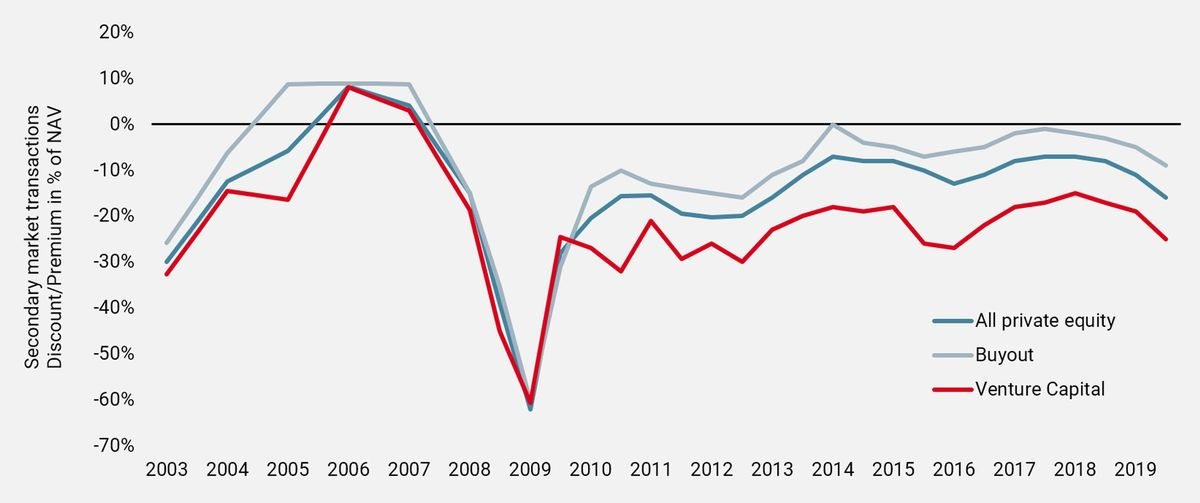

Secondary prices are cyclical and adjust quickly to public markets and the overall economic situation. In previous recessions, particularly during the GFC, average prices dropped rapidly and massively, down to discounts of around 50% to 60%. However, they recovered fairly quickly and returned to “ordinary” levels after just four quarters (albeit on lower NAVs). We could well see the same trend this time.

Secondary prices are cyclical and adjust quickly to the overall economic situation.

Figure 1: Crisis times lead to higher discounts and to attractive opportunities

Secondary volumes are also cyclical. The volume drop during the GFC was mainly demand-driven, since buyers were overly cautious at the peak of the crisis, demanding prices much lower than those which sellers would accept.

We expect PE buyers to be more bullish than during the GFC.

We expect secondary investors, who are now typically more sophisticated and experienced than in 2007/08, to be more bullish this time around. However, we still expect overall deal volumes to drop over the course of 2020 to as low as USD 50bn (down from USD 88bn in 2019). We could possibly then see a strong rebound of volumes in 2021, climbing up to between USD 80bn and USD 100bn.

When will secondary opportunities begin to emerge from the crisis?

Unless there are investors in serious financial trouble within the next two to six months, we expect most potential sellers to wait for the publication of Q1 and / or Q2 reports in order to get a clearer understanding of the impact of the COVID-19 crisis on both valuations and operational performances. Anecdotally, most buy-side processes have been put on hold pending the publication of the Q1 and Q2 reports.

We therefore expect the first opportunities to emerge in the next six to nine months.

What opportunities do you expect to see in the short term?

In the short term, most, if not all, GP-led restructurings will be put on hold, due to the inability for LPs to conduct on site due diligence and a mismatch in price expectations. We expect in particular that large single asset restructurings will no longer take place, as GPs will find it hard to complete them without steep discounts.

We expect the first opportunities to arise in the next six to nine months. In both the short and longer term, there will be a whole range of opportunities

The first sellers are likely to be liquidity strapped sellers – institutional investors, financial organisations, secondary funds and so on. We can expect to see opportunities in the following areas:

- Deeply discounted deals in high quality portfolios, where the price overcompensates the valuation / portfolio risk. For example, in 2013, as Spain was emerging from a protracted slowdown, we were able to source a portfolio of Spanish funds from a Spanish bank which was urged by the National Bank of Spain to immediately sell all remaining private equity holdings off its balance sheet. We paid a 57% discount to NAV. Ultimately, this deal achieved a 2.3x and 34% IRR for our investors.

- Acquisitions of single LP stakes in high quality portfolios at deep discounts. For example, in 2009, we acquired a stake in a blue-chip Central and Eastern European fund for a 60% discount, ultimately making a 2.3x for our investors.

- Acquisitions of LP stakes in partially funded portfolios from investors forced to reduce open commitments. For example, in 2009, we were able to acquire an LP stake in an immature fund managed by a blue-chip, difficult to access Benelux GP. We acquired the position, which was less than 20% funded, from a distressed Belgian family office at a 50% discount.

- Acquisitions of portfolios from secondary investors who are forced to sell due to breaches of leverage / deferred payment covenants. Given the increase in popularity of the use of such structures, we expect there to be a large number of such deals coming out of this crisis.

In all cases, it will be critical that secondary investors perform detailed bottom-up due diligence and valuations on each underlying company given the uncertainty around NAVs at the fund level in the short term.

And what about longer term opportunities?

Looking beyond 2020 and into 2021, we expect the following opportunities to arise:

- Acquisitions of LP stakes in funds which have been valued down. For example, in 2010, we acquired an LP stake in a US buyout fund. The portfolio was valued at 0.7x cost but we knew the GP well and through our due diligence saw that the companies were of high quality and were at an inflection point in their revenue growth. Ultimately, we made a 2.3x and 28% IRR for our investors.

- Funding of cash-strapped growth, venture capital or buyout funds. We expect that we will be able to source opportunities to set up preferred structures in sidecars or single asset restructurings. For example, we recently set up a sidecar for a US growth capital manager who had run out of capital from its fund to support its best companies. Within six months of our investment, the first of the seven company portfolio was sold, achieving over 11x cost.

- Fund restructurings, formation of sidecars or single asset restructurings led by GPs wanting to support their best companies until the exit window reopens.

- Acquisition of portfolios from lenders, such as banks, who would have taken possession of over-leveraged secondary portfolios. We already hear that those banks who have been the biggest lenders to secondary players are already considering their options.

The COVID-19 crisis should present excellent investment opportunities to the experienced secondary investor.

To conclude, the secondary market has been the strongest growing segment within private equity for the past couple of years. While the current crisis will inevitably halt this growth and set the market back in terms of prices and volumes, we believe that it will also present some excellent opportunities for the experienced secondary investor.

The nature of the opportunities that we will see are ideally suited to secondary investors targeting the small end of the market, where there is less competition. In addition, it will be vital to have the skills and resources to perform detailed bottom up valuations on all companies in a portfolio and, where required, provide tailored liquidity solutions to GPs.

Finally, the current crisis is demonstrating the pitfalls of using too much leverage. At Unigestion, we continue to believe that the use of leverage is not a requirement to generate superior returns.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Additional Information for US Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”).

This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

US

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EU

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (“OSC”).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

SINGAPORE

This material is disseminated in Singapore by Unigestion Asia Pte Ltd. which is regulated by the Monetary Authority of Singapore (“MAS”).

Document issued March 2020.