- Our Nowcasters detected inflation risk very early in 2021, prompting a shift into real assets

- Inflation should cool in the new year, while growth remains healthy

- In this environment we prefer US equities, Quality and Tech stocks and the US dollar in general

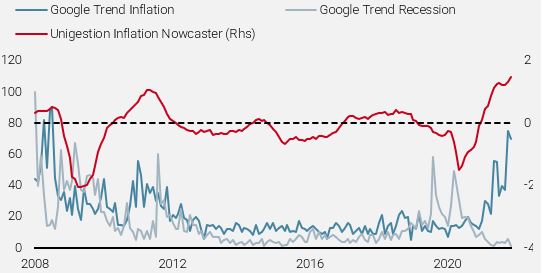

Like a phoenix rising from the ashes, inflation reemerged from the depths of Covid in 2020, accelerating throughout 2021 to heights not seen for decades in the Western world. This post pandemic surge was not expected, as evidenced by online searches for the term “inflation”, which only started taking off mid-2021. Contrast this with our Inflation Nowcaster, which already had identified the potential for inflation surprises late in 2020 and early 2021.

Figure 1: Unigestion Global Inflation Nowcaster vs Online Searches Since 2008

Sources: Unigestion, Bloomberg, Google as of 30.11.2021. The Inflation Nowcaster index is a proprietary, real-time synthetic measure of inflation surprises. A reading above (or below) 0 of the Inflation Nowcaster signifies that inflation is growing at a higher (or lower) pace than expected inflation.

Inflation Sways the Markets in 2021

When it comes to assets performance, 2021 marked a seismic shift in perceptions as well as positioning in the markets. Still reeling from multiple waves of Covid and renewed restrictions during the winter months, the world seemed braced for another year of uncertainty on the economic front. As the situation started to improve thanks to vaccination rollouts, ample government support and seemingly limitless accommodation by the world’s most powerful central banks, so did the financial narrative, which took on the form of “reflation”.

In this environment:

- Real assets outperformed

- Investors rotated from defensive to cyclical, and from nominal to real assets

- Dispersion within and across assets was considerable

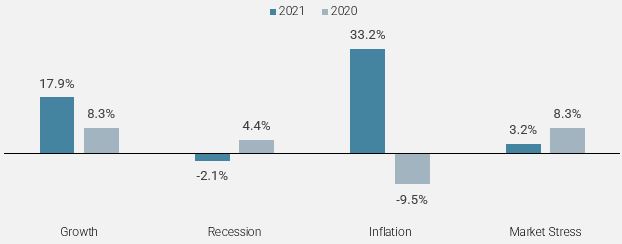

This broad rotation across and within assets is closely mirrored by the performances of our macro baskets, a range of assets corresponding to key macro regimes, the themes that ultimately drive financial markets. Unsurprisingly, real assets within the “inflation” basket performed extremely well in 2021, as opposed to 2020, when the “recession” macro basket delivered positive performance and inflation-related assets declined significantly (Figure 2).

Figure 2: Unigestion Macro Basket Performance (2021 vs 2020)

Sources: Unigestion, Bloomberg as of 30.11.2021. Growth Basket is a blend of HY and Global Equity indices, Recession Basket is represented by Duration, Inflation Basket is a combination of cyclical commodities and Inflation breakevens, Market Stress Basket is made up of the Vix future and AUDJPY. All Macro baskets are hypothetically derived and for illustration purposes only.

This reflation narrative has persisted over the last twelve months, morphing into a full-blown ‘inflation’ story

A Momentous Shift in the Macro Narrative

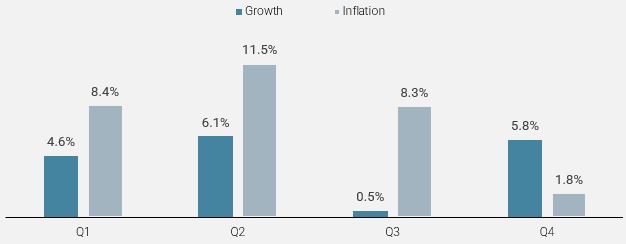

This reflation narrative has persisted over the last twelve months, morphing into a full-blown “inflation” story, with real assets outperforming growth assets most of the time in 2021.

Figure 3: Quarterly Performance of Unigestion Growth Basket vs Inflation Basket

Sources: Unigestion, Bloomberg as of 30.11.2021. Growth Basket is a blend of HY and Global Equity indices, Recession Basket is represented by Duration, Inflation Basket is a combination of cyclical commodities and Inflation breakevens, Market Stress Basket is made up of the Vix future and AUDJPY. All Macro baskets are hypothetically derived and for illustration purposes only.

It only took one year for real assets to recover all their losses accumulated since 2014, reflecting the breadth and magnitude of the inflation surprise and its subsequent price adjustment.

How did Adaptive Global Macro Navigate in this Terrain?

The fiscal stimulus – first used by households and companies as precautionary savings, then as consumption – added a demand effect to the initial supply shock, resulting in a monumental inflation surprise. Our Nowcasters, combined with a thorough analysis of the post-Covid supply chain – which exhibited low inventories and an overdependence on certain geographical areas and specific components – revealed at a very early stage that the risk of a supply shock would be the most important factor for inflation in 2021. We consequently adjusted our exposure:

The main change was in real assets, where we went from short to long within a couple of months (figure 4).

Figure 4: Historical Allocation to Real Assets in Adaptive Global Macro

Sources: Unigestion as of 30.11.2021

The multiple contributors to performance in 2021 result from both directional and relative value trades

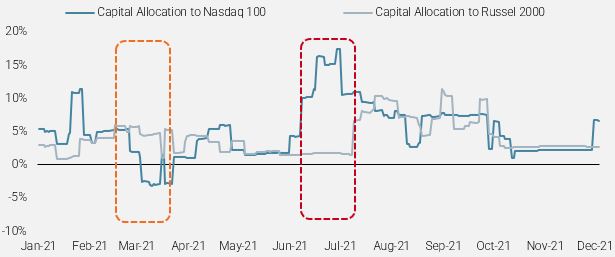

Our tactical tilt towards the reflation theme was not limited to real assets. Within growth-oriented assets, we also implemented key relative value trades. Early in the year, we went long the Russell 2000 vs the Nasdaq 100, mainly because of the higher implied duration embedded in the tech segment of the US equities market (figure 5). We also felt that unloved and under-owned sectors such as energy or financials would outperform, as evidenced through higher commodities prices and steeper yield curves. After five months of underperformance, coupled with a steep rise of 35 basis points in US 10yr real rates over that period – which considerably affects the tech sector – we turned more positive on the Nasdaq 100 mid-May and went long in our portfolio. By June, once the tech index had vastly outperformed the broader equity index, the strategy benefited from this tactical bet. As a result, the contribution of growth-oriented assets to the strategy’s performance proved significant in H1 2021, illustrating the benefits of the flexibility in our views and the depth of our investment universe.

Figure 5: Historical Capital Allocation to Nasdaq 100 and Russel 2000

Sources: Unigestion as of 30.11.2021

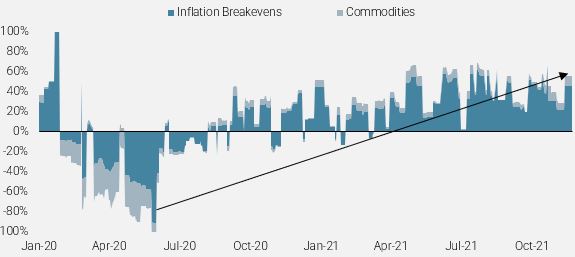

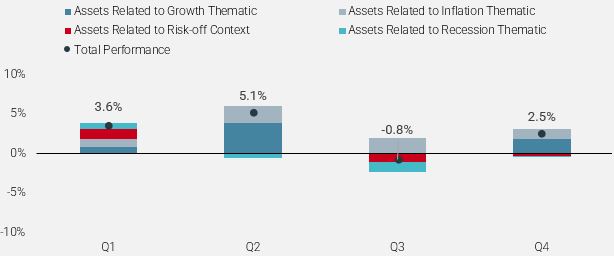

The multiple contributors to performance in 2021 result from both directional and relative value trades. As we base our dynamic allocation on macro risk factors, the bulk of our performance came from assets related to inflation such as cyclical commodities and inflation breakevens (Figure 6). Nevertheless, growth-oriented assets such as developed and emerging equities, credit spreads or cyclical currencies contributed positively as well, mainly in Q2 and Q4. Interestingly, real assets contributed more in aggregate than growth-oriented assets over the year (Figure 6).

Figure 6: Contribution to Adaptive Global Macro Strategy Performance by Assets

Sources: Unigestion as of 30.11.2021. Past performance is not a reliable indicator of future results, the value of investments can fall as well as rise and there is no guarantee that your initial investment will be returned. Returns may increase or decrease as a result of currency fluctuations. Please refer to the Important Information section for further information and disclosures.The performance of the Unigestion Adaptive Strategy is the hypothetical performance from 01.01.2015 to 31.08.2021, gross of fees chained from 01.09.2021 with the live performance of the first actual portfolio managed by Unigestion adopting this strategy. The hypothetical performance is based on the carve out of the most representative account of the Multi Asset Risk Targeted Composite, leveraged 5x to target an ex-ante volatility of 10%. Performance returns are shown net of management fees, with dividends reinvested. Please refer to the GIPS Compliant Presentation at: /unigestion-global-macro-10-target-volatility/

We see a gradual and telegraphed reversal, where employment matters most, much like the one engineered by Yellen back in 2016

No “Volcker Massacre” in 2022

Our central scenario for 2022 calls for an easing in supply bottlenecks, lower growth, and tighter financial conditions, which in turn should cool inflation. As such, we do not expect Powell to tighten anywhere near as shockingly and aggressively as Volcker did in the late 1970s, where the fight against inflation was his only priority. Rather, we see a gradual and telegraphed reversal, where employment matters most, much like the one engineered by Yellen back in 2016.

With the market having absorbed three rate hikes next year, starting in March or May, the question for investors is whether they expect more or fewer hikes. We are squarely in the camp of fewer.

Our core view for next year: Inflation normalises

For 2022, monitoring real rates and the US yield curve will be key to assess to what extent the expected tightening by the world’s major central banks could derail the bullish trend in both earnings growth and returns for growth and real assets.

What if We are Wrong?

We see two alternative scenarios that could derail our core views for 2022:

- The dreaded “Monetary Policy Mistake”

In this scenario, inflation peaks later than we anticipate, leading central banks to tighten earlier and more than expected. Worse, central banks could slam on the breaks even sooner, shifting to a narrative of “durable” inflation, even though it has already peaked and is starting to fall. As a result, bond yields would rise across the board, punishing growth assets, triggering a vicious cycle of position liquidation, and deleveraging.

- Covid lingers, gets worse

Vaccine effectiveness could wane, new and more dangerous variants would appear, leading to increased lockdowns and restrictions on a global scale. Households and companies would then pull back into “precautionary savings” mode, while central banks start stimulating massively again to avoid deflation and cascading defaults, pushing bond yields significantly lower. Meanwhile, governments ramp up fiscal stimulus again, issuing huge amounts of debt.

Two alternative scenarios that would challenge our core view:

The US Dollar should benefit from stronger US GDP and higher liquidity

Navigating in a Year of Normalisation: From “Low and Rising” to “High and Falling”

We see next year as more challenging for beta, hampered by tighter financial conditions combined with waning fiscal and monetary support, as well as higher growth uncertainty due to the uneven sanitary crisis.

Against that backdrop, we would prefer:

- Quality segments in equities that offer solid earnings growth and higher visibility in terms of profitability

- US equities versus the rest of the world, thanks to a more flexible US policy mix and its corporate leadership in key sectors

- A US Dollar that should benefit from stronger US GDP and higher liquidity in its capital markets, both of which should drive flows into US assets

- We would also be less exposed to real assets than we were in 2021, as current pricing in both inflation breakevens and energy prices reflect a durable expansion period in the global cycle, which in our view, given the potential headwinds identified for next year, seems too optimistic.

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision. Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein. To the extent that this report contains statements about the future, such statements are forward looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modelling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance. No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Hypothetical Performance Disclaimer

Hypothetical, backtested or simulated performance is not an indicator of future actual results. The results reflect performance of a strategy not currently offered to any investor and do not represent returns that any investor actually attained. Hypothetical results are calculated by the retroactive application of a model constructed on the basis of historical data and based on assumptions integral to the model which may or may not be testable and are subject to losses. Changes in these assumptions may have a material impact on the hypothetical (backtested/simulated) returns presented. Certain assumptions have been made for modelling purposes and are unlikely to be realized. No representations and warranties are made as to the reasonableness of the assumptions. This information is provided for illustrative purposes only. Specifically, hypothetical (backtested/simulated) results do not reflect actual trading or the effect of material economic and market factors on the decision-making process. Since trades have not actually been executed, results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity, and may not reflect the impact that certain economic or market factors may have had on the decision-making process. Further, backtesting allows the security selection methodology to be adjusted until past returns are maximized.

Hypothetical performance results have many inherent limitations, some of which are described below. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular trading program. One of the limitations of hypothetical performance results is that they are generally prepared with the benefit of hindsight. In addition, hypothetical trading does not involve financial risk, and no hypothetical trading record can completely account for the impact of financial risk in actual trading. For example, the ability to withstand losses or to adhere to a particular trading program in spite of trading losses are material points which can also adversely affect actual trading results. There are numerous other factors related to the markets in general or to the implementation of any specific trading program which cannot be fully accounted for in the preparation of hypothetical performance results and all of which can adversely affect actual trading result

Additional Information for U.S. Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat. This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors. This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control

Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns. Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss. The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

This material is approved and disseminated by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”) and registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients. This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).