Unigestion Global Macro: A Unified Approach for Systematic and Discretionary Macro Investing

- Unigestion Global Macro combines systematic and discretionary macro investing to capture a large set of market drivers and deliver a diversified portfolio. Its approach is flexible and nimble enough to adapt to the prevailing macroeconomic conditions, generating attractive risk-adjusted returns regardless of market conditions.

- Thanks to its ability to adapt to macro and market environments, the strategy has provided a diversifying returns source during particularly challenging environments, either by boosting returns or reducing risk.

- On an absolute basis, its return profile has exhibited an attractive asymmetry, with positive skewness and thin tails.

- Regardless of the macro scenario that plays out, we expect the strategy to continue to perform because of its adaptive nature, which is the result of its underlying components, each of which are built with this inherent dynamic.

Global Macro and Its Role in a Broader Investor Portfolio

All investors construct their portfolios to achieve the goals that matter most to them, while contending with their constraints. These goals and constraints vary, but most investors are aiming to achieve a level of return while mitigating the risks they bear to meet the return objective. While risk is sometimes discussed as an abstract concept, it is concrete: failure to manage it may mean undelivered pension benefits, tuition grant cuts, etc. The role of diversification and how best to achieve it are thus key questions for investors.

Within this broader portfolio context, global macro strategies can offer some key benefits: a dynamic investment approach that has benefited in the past from significant market dislocations, typically a broad and liquid opportunity set across asset classes and economies, and a returns source exhibiting low correlation to traditional assets. However, a plethora of styles and approaches to global macro investing can lead to a significant dispersion in returns and high manager selection risk.

In general, global macro managers can be classified along two axes: systematic vs discretionary and fundamental vs technical. While nearly all managers are some combination of systematic and discretionary, it is the balance of the two that matters. For example, a systematic manager will likely employ a discretionary “kill switch” to turn off their models when conditions warrant it. At the same time, a discretionary manager may produce systematic dashboards that inform their decisions. The second axis indicates the nature of the information set used to make investment decisions. Fundamental managers will place more emphasis on macroeconomic conditions within and across countries, examining growth and inflation dynamics, fiscal and monetary policy, supply and demand, etc. Technical managers, on the other hand, will place more emphasis on price dynamics, potential for reversion to some neutral value, the relative attractiveness of holding one security compared to another similar security, etc.

Our Approach: Unigestion Global Macro

At the core of our investment approach is the belief that macro fundamentals are the ultimate drivers of financial returns over the medium- to long-term. At the same time, we know that other market drivers can dominate over the short-term and that ignoring them can destroy capital. Therefore, in order to achieve our objective of delivering attractive absolute and risk-adjusted returns in any environment, it is critical to assess multiple market drivers and adapt our strategy accordingly.

We combine systematic and discretionary strategies to capture multiple market drivers and deliver a portfolio that can generate alpha regardless of rising or falling prices.

From our experience as macroeconomists, traders, and quants, we know that some drivers are best captured systematically, while others should be handled on a discretionary basis. From the beginning, our systematic and discretionary engines were viewed as peers with a common investment universe on which to form views that would then be translated to a portfolio using a common risk model. This approach has a few key consequences that are noteworthy:

- The discretionary process is neither a validation of the systematic signals nor an override;

- As peers expected to generate diversifying returns, the systematic and discretionary engines must capture different drivers and generate independent signals;

- These signals may offset each other, leading to a low conviction view that will directly correspond to a small exposure, or they may reinforce each other, leading to a high conviction view and large exposure;

- A unified and harmonised framework is necessary to capture both systematic and discretionary signals and translate them into a portfolio.

Figure 1 shows the high level composition of the strategy, indicating the three primary sub-strategies (or “books”) and their long-term target risk budget:

- Systematic Macro Allocation (40%): a regime-based asset allocation approach that assesses the prevailing macro and market regime and takes long/short views on global assets;

- Discretionary Macro Allocation (40%): a team of experienced portfolio managers that have flexibility to express their views across and within assets;

- Systematic Macro Trading (20%): a suite of rules-based quantitative signals, using both fundamental and technical analysis, on individual financial securities.

Figure 1: Target Risk Allocation of Unigestion Global Macro by Component

Source: Unigestion, Bloomberg. Data as at 28.02.2021.

Each of the three books represents an approach to global macro investing, with its own information sets, decision frameworks, and return profiles. Many investors are already aware of the benefit of combining these strategies in their portfolio. However, by constructing and managing these strategies ourselves, we are able to reap netting benefits with lower fees for investors as well as profit from the complementary nature of the books.

Unigestion Global Macro’s monthly returns highlight the strategy’s strong upside and limited downside capture.

Figure 2 compares the monthly returns of the Global Macro strategy to global equities, illustrating its strong upside and limited downside participation. It also shows the complementary return profiles of the sub-strategies: Systematic Macro Allocation is the reliable but linear return engine, Discretionary Macro provides good convexity on both upside and downside but is less reliable as humans can err, and Systematic Macro Allocation provides reliable downside convexity without degrading returns on the upside. This behaviour underscores the rationale for combining the books as we do.

Figure 2: Strategy Returns Against Global Equity Returns with Quadratic Fit

Source: Unigestion, Bloomberg. Data as at 31.01.2021.

The aim of our Global Macro strategy is to deliver attractive returns with positive asymmetry through a diversified set of macro signals. However, it is important to note that the strategy is neither a tail hedging nor a carry strategy. All trading signals, whether systematic or discretionary, are expected to generate positive returns over the full investment horizon, whatever the macro and market environment. This is not the case for tail hedging strategies that can offer protection but with a critical cost that is at odds with our goal of positive returns in different contexts. Meanwhile, carry strategies are structurally at risk during economic shocks and exhibit negative skewness (see Figure 3, left). As a result, our strategy, as well as its sub-components, is lowly correlated to tail hedging or carry strategies, as shown in the table on the right of Figure 3.

Figure 3: Skewness of Monthly Returns (left) and Strategy Correlations (right)

Source: Unigestion, Bloomberg, Data as of 31.01.2021. Reading note: Carry strategy returns are those of the corresponding Bloomberg GSAM index. Tail Hedging returns are calculated as the return of the CBOE S&P 500 5% Put Protection Index over the S&P 500 index.

Expectations for Unigestion Global Macro in Changing Environments

A successful global macro strategy should be resilient to many environments, adjusting its exposures dynamically to profit from opportunities and avoid risks. Below we walk through how the Global Macro strategy would be expected to navigate and adapt to three different scenarios that are especially relevant today:

- a central scenario of solid growth with muted inflation pressures;

- an upside scenario of strong growth and an inflation overshoot;

- a downside scenario of another recession.

The strategy is responsive to the prevailing macro and market environment and can deliver alpha under almost any conditions.

While the strategy is expected to perform well under all three scenarios, even if none of them transpire, we expect it will adjust in due time and still deliver on its objective.

Central Scenario: Goldilocks Returns

After a year full of economic lockdowns to contain the coronavirus pandemic, 2021 has the trappings of a broad economic and market recovery:

- Vaccinations, economic normalisation, accommodative monetary policy, and a resumption in capital deployment are powerful tailwinds for a broad economic and market recovery in 2021.

- These factors allow for rotation from crowded trades to unowned sectors and styles, raise headwinds for the US dollar, and support cyclical commodities as global trade accelerates.

- A supportive mix of fiscal and monetary policy also leads to lower realised and implied volatility, further supporting the “risk on” context.

Under our central scenario we would expect the strategy to strongly capture upside while managing short-term market stresses.

In such an environment, nearly all assets should perform well. Beta strategies would benefit through their exposure to growth-oriented assets, while any negative impact from fixed income exposure should be limited as any pickup in yields would be contained. We expect the Global Macro strategy to also benefit, capturing the upside and managing any shorter-term bouts of market stress.

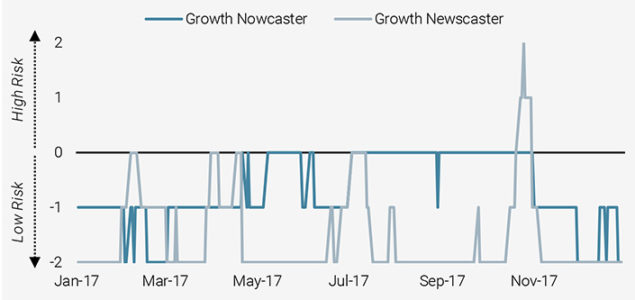

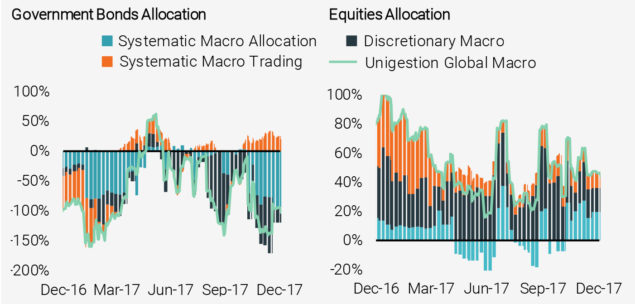

Such an environment is akin to 2017, where growth was healthy, inflation pressures limited, but valuations stretched. Figure 4 shows how our two indicators on global growth within the Systematic Macro Allocation book pointed to no significant risk to global growth during the year.

Figure 4: Recession Risk Assessment During the 2017 Goldilocks Environment

Source: Unigestion, Bloomberg. Data as at 28.02.2021.

During this period, the strategy was positioned to benefit from the positive context by going long equities and short bonds. This view was reinforced by the other two books, as shown in Figure 5. Importantly, this consensual view led the strategy to take on a significant amount of risk (though within set limits) and dynamically capture more upside.

Figure 5: Asset Class Exposures of Unigestion Global Macro During the 2017 Goldilocks Environment

Source: Unigestion. Data as at 28.02.2021.

Upside Scenario: Inflationary Spiral

While a long-only portfolio with broad, stable exposure to assets will post strong results in the central scenario above, its performance will be seriously challenged if there is an upside surprise:

- The vaccination rollout is successful and economies quickly normalise.

- Pent-up spending from households and businesses leads to a demand surge at the same time supply is constrained.

- Inflation picks up dramatically, even if on a temporary basis, leading to higher yields and raising the prospect of central banks reducing their support.

- With many asset valuations at all-time highs, especially in equities, a higher discount rate presents a major headwind and leads to a broad market sell-off.

Leveraging the right macro views through specific instruments can add absolute returns to diversified portfolios, even in less favourable market conditions.

This environment would be especially painful for the classic 60/40 portfolio and even potentially a risk parity portfolio with a large duration exposure.

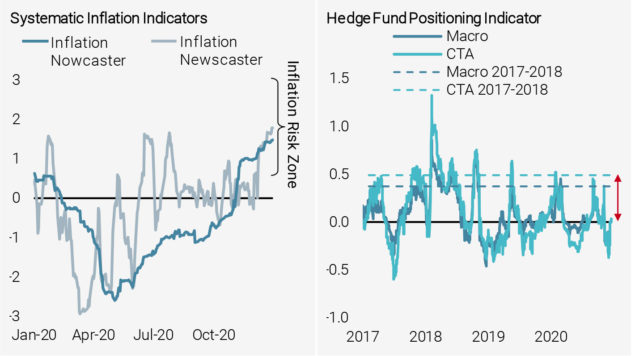

Indeed, our investment processes have been picking up signs of inflationary pressures since the end of 2020. The left hand chart in Figure 6 shows our two indicators tracking global inflation in the Systematic Macro Allocation book: both pointed to elevated inflation risk in late 2020 and continue to maintain these levels. At the same time, our discretionary portfolio managers assessed that investors were underexposed to inflation assets at the end of last year, as shown in the right hand chart of Figure 6.

Figure 6: Inflation Pressures Building but Mispriced in Late 2020

Source: Unigestion. Data as at 31.01.2021.

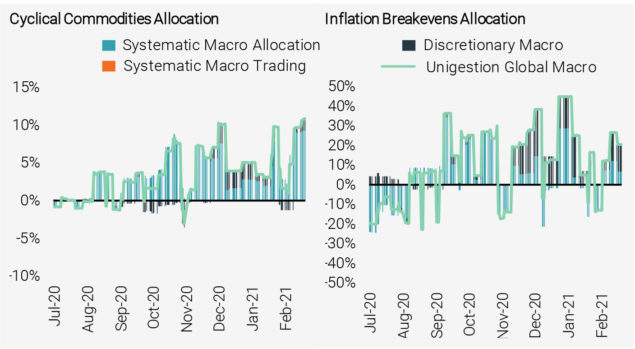

Combined with their views on further stimulus from the US and which markets stand to benefit most from an inflationary shock, the discretionary portfolio managers have at points reinforced the inflation exposures of the Systematic Macro Allocation book while offsetting it at other points, as shown in Figure 7. (It should be noted that the Systematic Macro Trading strategies did not allocate to those markets during this period.) If inflationary pressures continue to build, the strategy will remain long inflation-sensitive assets.

Figure 7: Asset Class Exposures of Unigestion Global Macro Since 2H 2020

Source: Bloomberg, Unigestion, as of 28.02.2021.

Downside Scenario: Another Recession

On the other side of our central scenario is another economic contraction:

- Vaccine failures or a new and dangerous coronavirus variant leads to major economic lockdowns yet again.

- Alternatively, premature austerity or some other unknown source constrains the recovery and growth plummets.

- Importantly, we estimate a very low probability of such an event in the coming months.

The strategy adapts to changing macro environments, benefiting from market dislocations and trends, and actively manages risk to preserve capital.

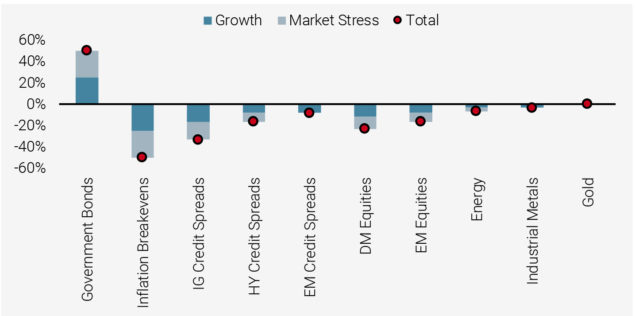

A high risk of recession and market stress, as assessed by our Nowcasters, would see them positioned within the Systematic Macro Allocation book as shown in Figure 8. They would be short nearly all assets outside of government bonds. Importantly, as our Market Stress Nowcaster is one of our fastest moving indicators, it would likely react first and push this book and the overall strategy into a more defensive stance.

Figure 8: Nowcaster Allocation by Asset

Source: Bloomberg, Unigestion, as of 28.02.2021.

As part of the systematic signals, we assess historical and cross-asset valuations in order to long/short assets that are under/overvalued. Ahead of the recession, valuations for growth-oriented assets would be high as investors price in the recent experience of healthy growth. However, as the recession materialises, they would become cheaper, reflecting the dire economic situation. In such a context, the valuation signals would lead the strategy to enter the recession with a short position in such assets, reducing it as these markets collapse before eventually moving long.

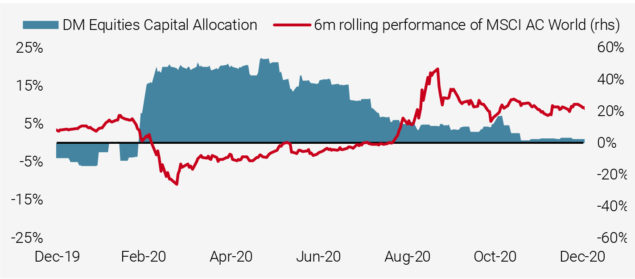

Figure 9 illustrates the net allocation to DM Equities of our valuation signals in 2020: before the COVID crisis in February, we were short on the back of strong 2019 returns. As the crisis unfolded and equity markets fell dramatically, the valuation indicators reduced their shorts and moved long, peaking at 20% on March 16 and maintaining that position through the April rally. Starting in May and continuing to the end of the year, as equity markets continued to rally thanks to fiscal and monetary support, the long exposure was progressively reduced.

Figure 9: Capital Allocation of Valuation Signals to DM Equities

Source: Bloomberg, Unigestion, as of 28.02.2021.

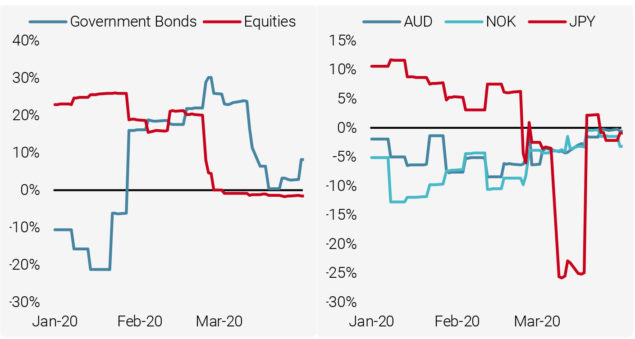

In addition, the Systematic Macro Trading book includes two strategies, Trend Following and FX Value, that are expected to and have exhibited defensiveness during prolonged market collapses. Trend Following is expected to perform well in durable market downturns as it adapts its positioning, while FX Value takes long/short positions in those currencies that are under/overvalued with respect to their PPP exchange rate. Ahead of a recession, this strategy is typically short high-beta currencies like the Australian dollar and Norwegian krone and long safe-haven ones like the Japanese yen as the former are bid and the latter offered by investors extrapolating past conditions into the future. As investors adjust their expectations in light of the recession, the strategy typically reduces these exposures automatically, thereby preserving its gains.

Trend Following and FX Value are key components of Systematic Macro Trading and act as the first line of defence during down markets.

Figure 10 shows the allocation of Trend Following and FX Value to key assets during the COVID crisis, demonstrating how the two strategies adapted in such a turbulent time. During such market environments, it is critical to have trading strategies such as these that can be among the first line of defence to protect capital while the rest of the portfolio adapts to the new reality.

Figure 10: Capital Allocation of Trend Following (left) and FX Value (right)

Source: Bloomberg, Unigestion, as of 28.02.2021.

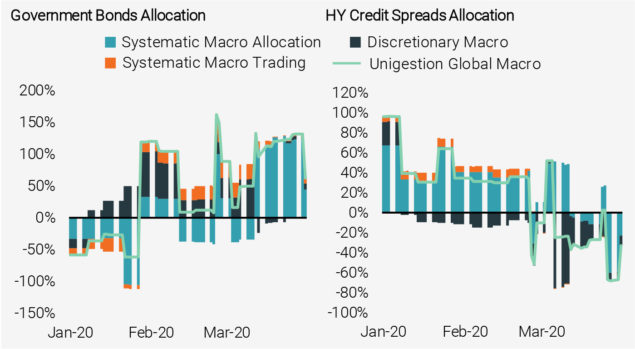

Finally, Figure 11 provides the allocation of the three sub-strategies during the COVID crisis to government bonds and high yield credit spreads. This recession was particularly unique given the exogenous source and its short but severe nature. Thus, the slower moving signals, such as those tracking growth and inflation, were behind the curve. Nevertheless, the systematic indicators tracking market conditions, such as the Market Stress Nowcaster and valuations, did aid in moving the portfolio to a more defensive stance.

As mentioned above, Trend Following built a net long exposure to government bonds in early February 2020 as reports of the virus spreading beyond China broke. As the crisis hit in late February, Trend Following added to this defensiveness by shorting high yield spreads, as shown in the right hand chart of Figure 11. At the same time, the discretionary portfolio managers had already been building a short high yield spreads exposure and added to it in late February and early March as they assessed that these markets were most exposed to a global recession.

Figure 11: Asset Class Exposures of Unigestion Global Macro During the COVID Crisis

Source: Bloomberg, Unigestion, as of 28.02.2021.

Conclusion

While global macro investing can be executed in many ways, any successful strategy must provide value to investors in nearly any market condition. Such a lofty goal demands a robust approach that captures a large set of market drivers and can adapt itself to almost any environment. We believe such an approach requires that diversification be embedded into the dimensions of an investment process: diversification across data, horizons, decision frameworks, styles, and markets to name a few. Unigestion Global Macro is the embodiment of this belief, encompassing systematic and discretionary macro investing to assess fundamental macro trends and market technicals, thereby generating attractive risk-adjusted returns in nearly any environment.

The strategy has provided a diversifying returns source during particularly challenging environments, either by boosting returns or reducing risk.

Our experience so far has confirmed the robustness of this approach. On an absolute basis, the strategy’s return profile has exhibited an attractive asymmetry, with positive skewness and thin tails. All three books have positively contributed and performance is not driven by any one asset class. The strategy has provided a diversifying returns source during particularly challenging environments, either by boosting returns (as in the case of the Brexit vote, February 2018, and March 2020) or reducing risk (as in the case of Q4 2018) in typical strategic allocations. On a relative basis, equity beta has been in line with expectations, gearing up when equities rallied and shifting to flat when equities fell. Correlation to asset classes has been minimal, as has correlations to other macro managers and indices.

Looking ahead, we expect the strategy to continue to perform because of its ability to be flexible and adapt to changing market environments. Its adaptive nature is the result of to its underlying components, each of which are built with this inherent dynamic. Hence the strategy does not need a healthy (but not too healthy) growth environment, an inflation overshoot, or a second recession to perform. If any or none of these scenarios transpire, the strategy is expected to continue adding returns, reducing risk, or both for its investors.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Document issued April 2021.