Source: Unigestion, Bloomberg as of 1 December 2021

We have been communicating since the end of last year that inflation would be a key macro force in 2021 and drive market returns, as the post-crisis demand recovery would meet supply and labour constraints. We reiterated that it would prove more durable than central bankers expected and not simply the result of base effects.

However, heading into 2022, we believe inflationary forces will peak through a combination of slower (though still healthy) demand, a gradual resolution of supply issues, and constraints on the capacity of the economy to absorb higher prices. This does not necessarily mean inflation will fall back to the 2% target, but rather that it will ease considerably, thereby relieving pressure on the Fed to tighten too fast.

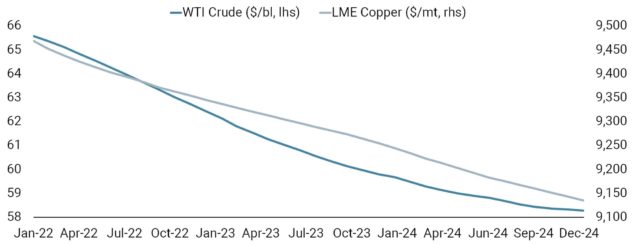

Savings rates have declined significantly, so we do not see a massive source of pent-up demand. At the same time, new capacity is being brought online and supply issues are expected to be largely cleared up in the early part of next year. Moreover, food, energy and other commodities are responsible for over half of headline inflation this year while less volatile components such as shelter and medical care grew at an elevated but more sustainable pace and only contributed 1.9% to the 6.2% y/y rise in the CPI. Absent an extraordinary surge in these core components, food and energy prices would need to see another upswing like the one in 2021 to keep inflation at these levels, implying oil trading at over 100 USD/bl. Indeed, market pricing suggests that commodity prices are set to fall in 2022, as shown in our chart, which aligns with lower demand and increased supply expected next year.

Important Information

The information and data presented in this page may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this page present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this page contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion.

Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.