Source: Unigestion, Bloomberg as of 26 November 2021.

Will the inflation premium continue to adjust upwards?

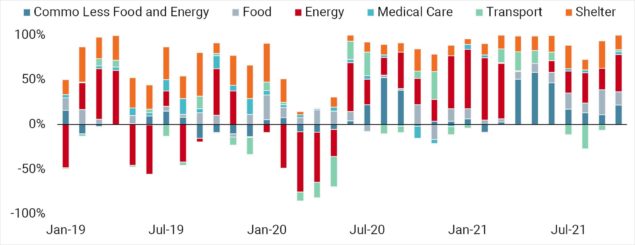

To answer this question, we need to analyse the contributors to the inflation surprise, distinguishing between what comes from « supply » and what comes from « demand » and separating the cyclical from the more structural. Our charts shows the contribution of the main components to monthly changes in US headline inflation between 2019 and 2021.

Two key elements stand out:

1) The most cyclical items, which are also the most volatile (food, energy and other commodities) and account for 41% of US CPI, explain most of the decline in inflation in 2020 and represent the bulk of the sharp rise in 2021.

2) More stable components such as “shelter” and “medical care” also rose more strongly than usual over the period but at a more sustainable pace.

Based on IMF growth forecasts and EIA studies, it is difficult to imagine a further increase of more than 50% in food and energy prices over the next 12 months. At the same time, an analysis of the forward curves shows that most energy commodities are in « backwardation », even signalling expectations of lower prices for coming quarters. In addition, the US household savings rate has “normalised”, falling from 17% to 6% within a few months, thereby reducing the risk of excess demand for goods and services in the near future.

As a result, even if the other components were to grow at a higher rate than the average over the last 20 years, notably « shelter » and « medical services », it is very unlikely that headline inflation will remain above 3% in 2022. We therefore see the current situation on the inflation front as a peak and not as the starting point of a demand shock cycle.

Important Information

The information and data presented in this page may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this page present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this page contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion.

Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.