At this stage of the recovery in both markets and the economy, we have a selective preference for the US dollar. This preference is based on all the factors guiding our dynamic allocation. On the macro side, growth differentials between the US and the rest of the world have narrowed, but inflation differentials are likely already supporting the greenback. Investor sentiment for the dollar has recently recovered and its valuation is not excessive. In a context where there is a risk of inflation shock – opening the door to episodes of market stress – a selective preference for the US currency makes sense to us.

I Need a Dollar

What’s Next?

Cycle gaps as a factor

Among the many reasons for having an exposure to the US dollar, the economic cycle is foremost. A number of academic research papers, including “Business Cycles and Currency Returns”1, show the role that macro momentum differentials can have on currency markets. To quickly summarise the key conclusions, the currencies of countries with the most dynamic macro cycles tend to outperform the currencies of less dynamic countries. Various measures have been proposed to approach this dynamism gap. We looked at nowcaster differentials and found that they largely corroborate the conclusions in the literature. This conclusion was confirmed for currencies associated with both developed and emerging countries and for our growth and inflation indicators. The currencies that appreciate the most are those with the highest nowcaster levels. So what is the message of our indicators lately?

A more even recovery

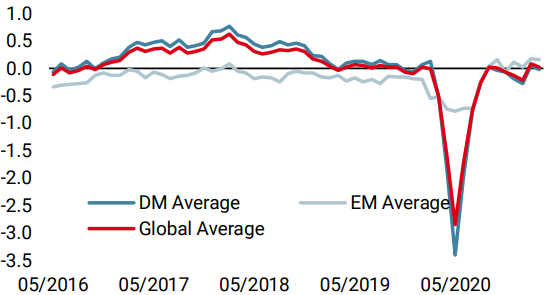

First of all, in terms of growth, the US economy has recently shown renewed dynamism after a period of volatility in its economic data. This dynamism is largely confirmed by our US Growth Newscaster: the indicator was already high at the beginning of March (+1.5 standard deviation) and continued to rise during the month, reaching +2.1 standard deviation, a figure close to historical highs. The growth argument is not, however, the one pushing for an overweight to the dollar. In February, the US was clearly ahead in terms of growth recovery but, since then, our indicators have clearly shown a strong convergence of the 83% of world GDP that we follow through our indicators. The recovery in March benefited from a global rebalancing and the gap between our Growth Nowcasters in the US and in the rest of the world has significantly reduced. If we stick to these growth signals, we are simply led to prefer the US dollar to the Canadian dollar, the euro or the Norwegian krone.

Heterogeneous inflation

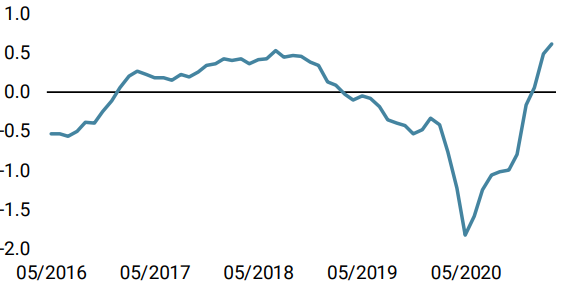

The highlight of the last few weeks is rather the rotation we have observed in our indicators. While the heterogeneity of our growth indicators has reduced, the heterogeneity of our inflation Nowcasters has increased. In line with the revision of the Fed’s inflation forecasts at its March meeting (PCE revised from 1.8% to 2.4% for 2021), our Nowcaster indicates that the US is the economy with the highest inflation pressures. Our US indicator is ahead of the one for the Eurozone, Switzerland, Great Britain, the Nordic countries, Japan and Australia. It is even ahead of several emerging countries (notably Russia and Mexico) where food inflation is running hot. These global Nowcaster spreads justify an overweight to the US dollar, and the signal intensity is equivalent to February 2018, when we observed a marked appreciation in the dollar, beyond the “Volmagedon” episode. This was also the case in 1993, 1997-1998 and 2005, periods that were all followed by a broad-based increase in the dollar’s value.

Given the magnitude of the fiscal and monetary stimulus that the US will receive over the next few months and the faster relative pace of its vaccination campaign, we find it hard to imagine that our US indicators will “underperform” the rest of the economies. We see a continuation of this situation.

The dollar could benefit from other supports

Beyond these macro drivers, two other dimensions are likely to play in favour of the dollar: sentiment and valuation.

In terms of market sentiment, two elements seem to us to be potentially supportive of the dollar. First, speculative positions on the dollar have changed significantly since the beginning of the year, going from a strong short dollar conviction against a wide range of currencies to a global neutralisation of these positions. If the market entered 2021 with the conviction that the US dollar would be the big loser of the recovery, the situation is now very different. Positioning on the dollar is now “cleaner” than it was three years ago, and we find it difficult to see this as an overshoot. If there is any exuberance, it is rather on the side of the equity markets. High equity valuations have created the risk of a reversal in the near term, which combines worryingly with rising interest rates. A long US dollar position seems to make sense from this point of view: the dollar has a negative correlation with equities during periods of stress. If this stress is triggered by a rise in interest rates, this rise will probably be stronger in the US than elsewhere and here again, this should benefit the dollar the most, with the exception of the yen.

Finally, in terms of valuation, the dollar remains an interesting currency. Although its short-term carry has collapsed, it still lies at the higher end of the G10 world, justifying higher valuations – even if against emerging currencies this argument becomes less compelling. In terms of “Purchasing Power Parity” valuation, the dollar’s valuation is not excessive, as our calculations place it around its “fair value”. It is difficult to find negative elements in these valuations. US assets remain attractive in absolute terms, with a bond carry rate of around 3% and an earnings yield for the S&P 500 at around 3.27% (vs. 1.95% for the Eurostoxx). Here again, a weakening of the dollar – if it occurs – could prove limited.

In conclusion, an aggressive overweight to the US dollar makes sense at this stage of the economic and market recovery. Our overweight to the dollar is notably against the euro, the Swiss franc, the Swedish krona and the New Zealand dollar. In line with our inflation theme, we remain long commodity-related currencies and long the yen for its protective qualities in case of market shocks.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

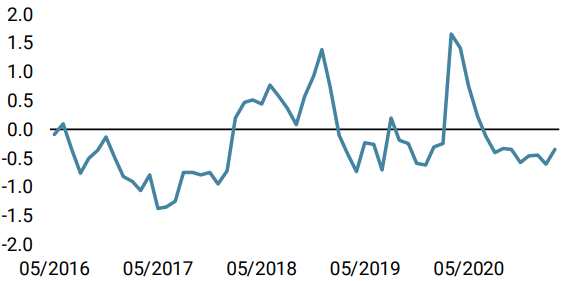

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster declined slightly as US data declined again. Recession risk remains low, as the majority of data continues to improve.

- Our World Inflation Nowcaster increased rapidly last week, as US and Canadian data rose sharply to elevated levels. Inflation risk is still very high.

- Our Market Stress Nowcaster remained broadly unchanged last week as volatility remained on the lower end of its recent range ahead of the Fed meeting.

Sources: Unigestion. Bloomberg, as of 19 March 2021

1Colacito, R., Riddiough, S. J., & Sarno, L. (2020). Business cycles and currency returns. Journal of Financial Economics, 137(3), 659-678.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).