Earnings season is now in full swing, and investors are getting a clearer picture of the toll that the coronavirus-induced restrictions are taking on businesses. With a low hurdle rate, many firms have posted positive surprises on both sales and earnings. However, these encouraging results need to be balanced with the more somber outlook that emerges when looking below the surface and putting the results in a larger perspective. In our view, the results reported thus far colour a picture of decent and stable growth, building inflation pressures, and a recovery that will continue to require fiscal and monetary support.

Colors

What’s Next?

Under-promise, over-deliver

Q4 2020 earnings season is upon us, providing an important perspective on spending, corporate profitability and capital flows. With elevated macro volatility, the results should provide some clarity on how firms are coping with the varying degrees of lockdown. In the US, 70% of the firms in the S&P 500 have reported, accounting for 80% of the index’s market cap, while in Europe, nearly 45% of firms in the Stoxx Europe 600 have reported, representing 55% of the market cap. The picture that has emerged thus far is one of a recovery underway but with significant signs of concern.

Going into this earnings season, analyst expectations were fairly dour and thus relatively modest results were enough to clear these low hurdles. For firms in the S&P 500, EPS growth stands at 7% on a year-on-year (yoy) basis, surprising by 19%. Indeed, the EPS of nearly 80% of firms beat expectations. Sales tell a similar, if less dramatic, story: they are up 2% on a yoy basis, with 73% of firms beating their estimates with an aggregate surprise of 4%. While the reporting season in Europe is not as far along, results there are also noteworthy: EPS growth is down -15% on a yoy basis, but 70% of firms have beat their estimates with an aggregate surprise of 12%. Sales growth however contracted nearly -15% versus last year, and only 49% of firms beat their estimates with a negative aggregate surprise of -1%. Clearly, Europe’s tighter restrictions at the end of last year had a significant impact on demand, though firms seem to be leaner and better able to absorb the loss in revenue.

Despite the significant positive surprises relative to analyst expectations, the market reaction has been strongly asymmetric to the downside. When looking at the price action of firms missing on their EPS estimates versus those that beat, it is clear that misses were penalised much more than beats were rewarded. This suggests that investors, in contrast to analysts, were expecting some combination of better past results or more optimistic future prospects.

Stability but no recovery yet

While the depth of the coronavirus crisis was akin to the Great Financial Crisis (GFC), the rapid recovery, thanks to the coordinated policy response, has meant that spending has not plunged as starkly as it did in 2008. Thus, while sales for S&P 500 firms fell nearly 12% in the GFC, they have held up in 2020 and are showing signs of stabilisation. Here, the S&P 500 also benefits from the growth of tech stocks, which saw sales accelerate during the crisis as working from home became the norm. The Stoxx Europe 600, which doesn’t benefit from such a heavy tech bias, has seen sales fall similar to their 13% collapse during the GFC. Importantly however, sales for European firms also seem to have stabilised last quarter. In a similar vein, profitability for US corporates has held up, with margins stabilising at 7.3% for the S&P 500 versus 10.2% at the end of 2019 and 2.2% during the GFC. For European firms, margins are now down to 3% versus 6.6% at the end of 2019 and a bottom of 2.1% in 2009. The dynamic at play is noteworthy as well. While headline figures are no longer collapsing, they have yet to show signs of a recovery, suggesting that the impact of restrictions continues to weigh heavily on firms’ income and balance sheets.

Looking more granularly at reporting in the US, where enough firms have posted results that we have a reasonable picture at the sector level, it is clear the crisis has led to significant disparity across firms. The Energy and Industrials sectors have seen sales fall by -34% and -12% respectively compared to a year ago, and earnings have fared worse: EPS shrunk -110% and -43%, respectively. On the other hand, the Consumer Discretionary (which includes Amazon) and Financials sectors have seen their EPS expand by 36% and 18% respectively. Again, the market action belies analyst expectations: though S&P financial firms beat estimates by 35% on aggregate, they were down nearly 1% on average the day after their announcement.

Planting seeds for an inflation surprise

One of the important figures we follow closely is capex, as it helps inform our outlook on the macroeconomy. By leveraging the capex figures already reported, we see that capex is likely to have collapsed by around 10% in 2020 for S&P 500 firms in aggregate. Despite positive news on the vaccine, Q4 is likely to see little additional capex, indicating that firms remain unwilling or unable to invest. By our calculations, the aggregate level of capex spending in 2020 as a percentage of GDP will be around 3% for the S&P 500, among the lowest levels going back to 1990 (the GFC saw capex collapse to 2.9%).

As we have communicated for some time, we believe the key risk for 2021 is inflation, as pent-up demand meets constrained supply in the context of a successful vaccination programme. When firms hold back investments, they naturally lay the foundation for an eventual inflation overshoot as new and more efficient capacity is not brought on line. The micro picture we are getting from businesses is corroborating our view that inflation pressures are brewing and investors who are currently only pricing in reflation will be taken by surprise. In the meantime, we continue to believe the risk-reward for risky assets has diminished in the short term, which so far has been confirmed by the earnings season. We therefore retain a cautious exposure to our longer-term pro-growth and inflation view.

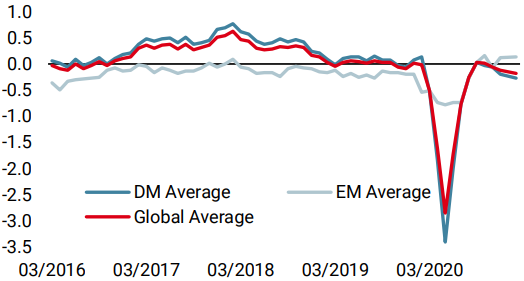

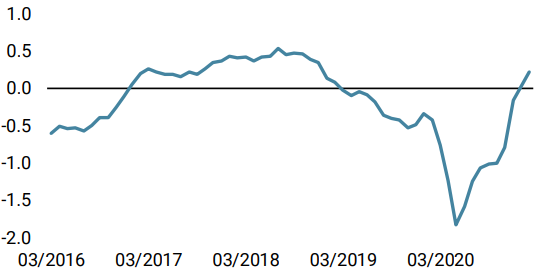

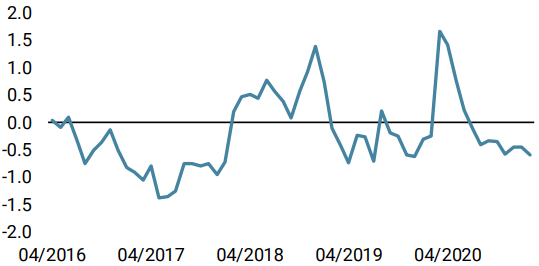

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster increased as US and Japanese data improved. Recession risk is back to being very low.

- Our World Inflation Nowcaster decreased marginally after several weeks of increases. Inflation risk remains very high.

- Our Market Stress Nowcaster remained stable, showing signs of investor bullishness.

Sources: Unigestion. Bloomberg, as of 12 February 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).