Since mid-January, financial markets have largely been driven by news surrounding the Coronavirus outbreak. The scale of the impact that the virus will have on the global economy and financial markets is impossible to predict at this early stage. The reaction in fixed income, commodity and currency markets has been driven by fear and high uncertainty. In January, copper fell over 12 consecutive days, representing its longest ever losing streak, crude oil lost 25% off its peak, US yields dropped by 40bps and defensive currencies rallied aggressively versus risk-on currencies (AUDUSD -4.9%, JPYKRW +4%). On the other hand, equity investors seem to be expecting the outbreak to have a large, but short-lived effect on China, with very little spill-over on the global economy. The support of the PBOC, which reduced the reverse repo rate by injecting CNY 1.7 trillion into the Chinese banking system last week via open market operations, and the ample liquidity offered by central banks around the globe and their readiness to act, are encouraging equity investors to buy on any market dips. It seems that fearful macro investors are running for the hills, while greedy equity investors are bathing in an ocean of liquidity.Fear vs. Greed

Greed, Godsmack, 2001

Greed

What’s Next?

Is the epidemic a buying opportunity?

There has been a lot written in the media about previous epidemics to get a playbook for the global economy and financial markets in the coming months. The S&P 500 index posted a gain of 14.59% six months after the first outbreak of SARS back in 2002-03, and 12 months after that point, the index was up 20.76%. Ultimately, the severity of the virus will dictate the market’s reaction and, just because it has managed to shrug off the contagion from outbreaks in the past, it does not mean that this will be the case this time.

To put SARS into perspective: In 2003, the Chinese economy was much smaller and it represented only 4.4% of global GDP (15.4% in 2019). China was also much less integrated in the global supply chain than today and therefore the risk of an economic shock spreading to the rest of the world was much less likely. Furthermore, the extensive efforts to contain the Coronavirus have been unprecedented and this will cause the Chinese economy to slow down abruptly.

The initial disruption was driven by the fear factor (demand shock) that restricted people’s mobility and led to a temporary decline in related activities, such as tourism, offline retail sales, transportation, catering services and entertainment. But once the New Year holiday was extended for most of the country, keeping factories, shops and restaurants shut, and leaving ships trapped at the port, it became clear that the supply shock would have a major influence on all sectors of the economy. So far, 14 provinces and cities across China, including the main industrial centres of Shanghai, Jiangsu, Guangdong and Fujian, have told businesses not to reopen until the week commencing 10th February. These places account for around 77% of China’s GDP and 80% of its exports. Given that China is now at the heart of many global supply chains, this may have knock-on effects around the world. A large chunk of what Asian countries export to China are intermediate products, which are then assembled before either being consumed in China or shipped off to the rest of the world. Developments over the next couple of weeks will be critical because the magnitude of the supply shock will depend on the pace of production recovery.

Historically, epidemics have proved to be great buying opportunities for equity markets, but, as already highlighted, the outbreak of the Coronavirus cannot be compared to any other epidemic. As an example, the SARS virus hit at a time when global stock markets were starting to bottom out following the bursting of the dot-com bubble, the Fed had cut rates significantly, the USD was falling giving a lift to emerging markets and the US had just entered into a war with Iraq. In contrast, heading into the Coronavirus epidemic, the Chinese economy and global trade was already faltering, valuations are very rich and equity markets are in the longest expansion phase ever. It begs the question why global equity markets are up 2% and emerging markets are only slightly lower year-to-date despite all this uncertainty. Waiting for a dip to buy has been a tough strategy when markets are flooded with liquidity.

Repo facility: QE or not? It does not matter

The PBOC’s latest policy easing was necessary to address the near-term shock and to avoid permanent damage to the economy. After the trade war issues settled in December, the Coronavirus outbreak provides a new excuse for central banks around the globe to stand ready or to continue their liquidity measures. They have responded to each crisis in the same way and every time they find that it takes more aggressive action to produce the same effects. Looser financial conditions do not help when the economy has no productive uses for the new liquidity. With most industries already having enough capacity, the money has nowhere to go but back into the banks and, respectively, into financial assets.

Whether it is called QE or not, buying bills (swapping reserves for short-term bonds), injecting liquidity into the market place and growing the balance sheet affects risky assets. Market conditioning (the Pavlovian effect) since the GFC is that stock markets cannot go down when the Fed is growing the balance sheet. Additionally, the Fed’s extremely aggressive response to the repo blowout in September is another signal to markets that it has a very low tolerance for market fluctuations.

History does not repeat, but it does rhyme

The “temporary” repo facility that started in September last year feels much like the injections of liquidity back in 1999, delivering a similar outcome. The special lending facility that started in late 1999 to support the feared Y2K computer glitch offers a historical analogy to the current period. The day the Fed opened its Y2K lending facility on October 7th 1999, the Nasdaq started its 103% advance until March 24th 2000, two weeks before the facility was closed. The liquidity-driven high marked the end of the dot-com bubble. The USD 120bn facility might not sound enormous in the current climate, but it is significantly more than on 9/11 and on a par with the support offered during the GFC. And it was not until last year, when the Fed’s repo operations finally saw meaningfully higher levels.

It is clear that the Fed balance sheet and repo facility cannot explain the stock market’s movement in isolation, but we believe that it should not be underestimated simply because it is not called QE. When the Fed injects money, the liquidity generally flows into momentum stocks (most of the high momentum names can currently be found in the Nasdaq). Since the repo facility opened last September, the Nasdaq has advanced 21% without looking back. Financial markets will listen closely to get some hints if the Fed will end T-bill purchases and repo support in Q2, the current projected end date, because investors are well aware of what happened after QE1, 2 and 3 ended.

The Coronavirus hits the global economy at a time when our growth Nowcaster has just started to improve and inflation has bottomed. The positive momentum was confirmed last week with a set of strong macro data that pushed the S&P 500 index to new highs, closing out its best week in six months. Strong data, stretched positioning and stimulus expectations triggered a violent factor rotation. Growth sharply underperformed Value, Momentum fell, crowded stocks underperformed and Cyclicals rallied. This improvement in data is partially driven by the trade war resolution, but there is a risk it will be short-lived once the demand and supply shock in China shows up in global data. The epidemic is yet another reason for a delayed and weak global recovery and sluggish global trade. It has just intensified the contradicting message that equities and commodities have given for quite some time. The reason is simply that central banks have not managed to stimulate the real economy as much as they have financial assets. It will take some time before we are in a position to assess the extent of the damage as the calculation of macro statistics were halted during the extended New Year break. That is why, besides following the news regarding the epidemic, our focus for equities will remain on the potency of central banks. On the other hand, the immediate outlook for oil will be dominated by the supply side (OPEC) and, for raw materials, the focus will be on the fiscal response of the Chinese government.For all of its uncertainty, we cannot flee the future

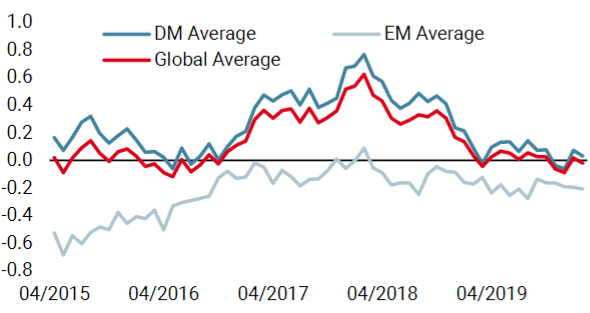

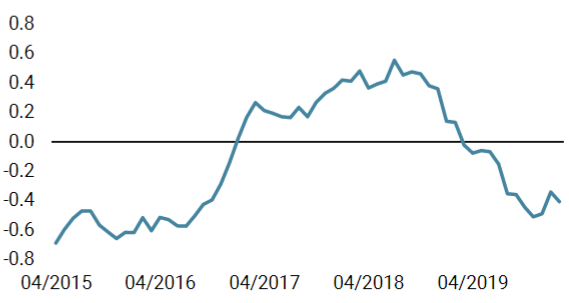

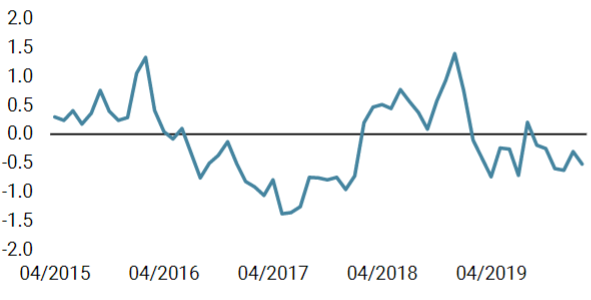

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster was down modestly over the week, as lower momentum from the US was partially offset by improvement in Canada and Japan.

- Our world Inflation Nowcaster increased slightly, due to a broad-based increase in developed world inflation pressures. However, inflation risk remains neutral.

- Our Market Stress Nowcaster receded after the rally last week and is back to showing a low level of risk.

Sources: Unigestion, Bloomberg, as of 10 February 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).