Inflation is nowhere to be seen, yet it is increasingly at the centre of discussions in the investment world. If inflation were to rise rapidly, an important part of the recovery could be derailed, from the bond world to the “duration” effect in equity markets. Our message is the following: although inflation remains a risk, it is not a scenario for us at this stage. The problem is that this risk is difficult to hedge given the associated costs, whether using instruments such as energy, gold or inflation breakevens. An inflation shock is therefore difficult to navigate, but at this stage unlikely: Nevertheless, let’s remain vigilant.

Pay the Price

Each period of recovery comes with a period of inflation normalisation: as economic activity declines during a recession, prices of goods and services fall – a mechanical effect of depressed demand. During the 2008 crisis, OECD inflation thus fell to -0.6% in July 2009. The months following a trough in the economic cycle are generally accompanied by a gradual resumption of inflation without any marked acceleration: in June 1983, US inflation rose from 2.8% to 5.2% by mid-1984. In December 2003, US inflation rose from 1.1% to 2.8%, and in 2009 it increased from 1.3% to 1.8%. Since the United States is a relatively closed economy and the dollar is the currency of raw materials, this normalisation has been rather smooth over the last 30 years. This is less the case for countries that trade a lot with the rest of the world, such as Great Britain or Switzerland. The normalisation phase in the United Kingdom between 2008 and 2009 saw inflation rise from -1.4% in mid-2008 to +5% in mid-2010: a much more violent increase than that observed in the United States. What these phases of normalisation have in common is their short duration: inflation rises above the central bank’s target for a few months before returning to its long-term trend. One of the main reasons for this is the typical origin of this normalisation: as household demand and investment pick up, commodity markets – especially energy – see their prices rise, mechanically leading inflation to a moderate, but above all, temporary acceleration. This was the case in the recoveries of 1994, 2003, 2009 and 2011. In June, the OECD’s inflation growth rate stood at less than 1%, a marked decline from its 2018 peak (+3.1%). One can reasonably expect this figure to start rising in the coming months, but to what level? A first approach to answering this question is to explore the forecasts of economists, national and international bodies and market pricing. Market economists expect inflation in the United States to be around 1% in 2020 and 1.7% in 2021. In the Eurozone, it should rise from 0.4% in 2020 to 1% in 2021. Finally, global inflation is expected to rise from 2.3% in 2020 to 2.6% in 2021: there is no sign of an acceleration in inflation in these forecasts. The forecasts of the Fed, the ECB and the IMF also point in the same direction: the Fed sees the “Core PCE” not exceeding 1.7% until 2022; the ECB does not anticipate inflation above 1.5% until 2022. The IMF expects global inflation to be between 3 and 3.5% over the same period. From the market’s perspective, it is not much different: the 10-year breakevens in the United States anticipate an inflation of 1.64% over that period while pricing for the Eurozone points to 0.7%. From whatever angle you look at it, inflation seems to be dead and buried. Is this really the case? Three elements could temper the pessimism of these forecasts at the macro level. Firstly, the initial cause of the recovery in inflation is economic activity. The various fiscal stimulus packages implemented around the world have led to a “V” shaped recovery and with it a faster-than-usual normalisation of inflation data. Our global inflation Nowcaster is clearly regaining ground, while remaining negative. Right now, 70% of its underlying data is on the rise: despite an only slight increase in energy prices, the speed of the economic recovery is enough to give our inflation surprise indicator a boost. If the recovery continues, inflationary pressures should fall back into line. The second important element for us is what economists call monetary inflation: monetarist theories predict, among other things, that strong growth in the money supply – the number one “QE” effect – should lead to a symmetrical rise in the price level. Recent historical experience belies this effect: since the implementation of quantitative easing policies, inflation has tended to fall and its volatility to decrease. However, this remains a medium-term risk. The third element we are looking at is the media treatment of the inflation theme: our inflation “Newscaster” currently points to a higher than usual risk of inflation surprises in a majority of developed economies. If inflation is not in the numbers, it is on everyone’s lips. Why is this? Today, this inflationary risk should not be underestimated for one reason: it is not anticipated by economists or by the financial markets. Even if an inflation shock is not part of our key scenario, it remains a risk that deserves our attention, and the danger it poses is a reflection of two elements. The first is that the current recovery is deeply dependent on the level of interest rates financing the increases in government debt. The bond world would be the first victim of an inflation shock, and a rise in rates could create shock waves through contamination in various markets. The central banks seem to be ready and willing to prevent a sharp rise in rates, but once again, it is a question of thinking about the risks more than the scenario itself. The second of these elements is that it has become very difficult to hedge against this risk because of the cost of hedging against inflation. Different inflation-related assets such as energy, gold or inflation breakevens are all expensive for different reasons. The term structure of oil barrel futures prices is ascending: hedging the risk of an inflationary shock with oil currently costs 5% per year on the WTI market. Gold, which is driven by multiple factors such as uncertainty, real rates, the dollar and inflation has seen its price soar, leaving it vulnerable to corrections as we have seen in recent days. Finally, inflation breakevens have risen rapidly from 0.6% to 1.6% and are now displaying a negative carry, with actual inflation remaining below expected inflation at this stage. As such, it is currently difficult to hedge inflation risks with these assets in view of their risk and cost. There seem to be two solutions left: the first one is to dynamically allocate inflation-linked assets based on data and news (our Nowcasters and Newscasters) in order to limit a prolonged exposure to these costly hedges. The second is to seek positive carry risk premiums that historically react well to inflation. This is the case, for example, with FX-based carry strategies. At this stage, our indicators recommend an overweight in the energy market, with limited conviction, and a neutral position on the remaining inflation-hedging assets. Currency carry strategies remain a source of negative returns for the moment, further evidence that inflation remains more of a risk than a scenario at this stage.What’s Next?

The unlikely rise in inflation

How high can inflation go?

The dialectic of under-anticipated risks

Unigestion Nowcasting

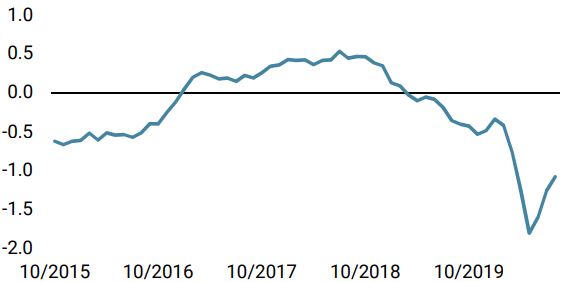

World Growth Nowcaster

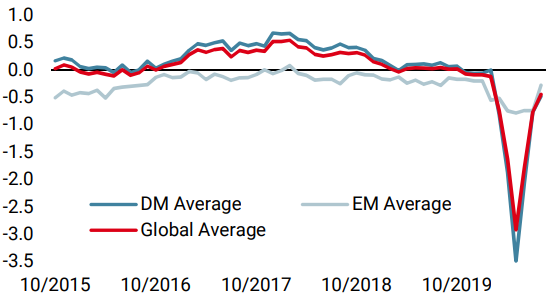

World Inflation Nowcaster

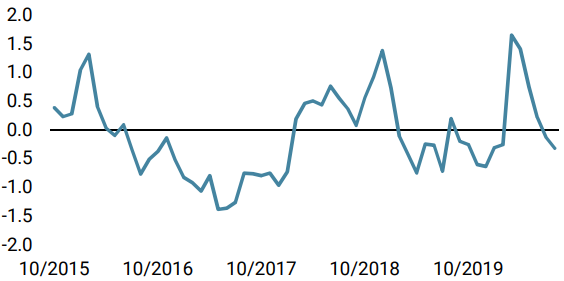

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster increased last week, as new improving data came out for Canada and the US.

- Our world Inflation Nowcaster increased last week, in a parallel to what happened on the growth side.

- Our Market Stress Nowcaster decreased last week, as volatility decreased.

Sources: Unigestion. Bloomberg, as of 24 August 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).