We remain positive on both growth and inflation assets for the year ahead, but price action in January and the first few days of February demand greater caution over the short term. On one hand, volatility is increasingly visible in the macroeconomic data that makes up our Nowcasters; on the other, exuberant investor sentiment has driven market valuations to levels that we find concerning. The macroeconomic situation is still solid and we are by no means defensive, but we have moderated our dynamic growth exposures towards a more neutral positioning.

The Neutral

What’s Next?

Agitated macro data

We see several reasons to adopt a certain neutrality in the dynamic allocation of our portfolios. Until recently, the macro picture was a strong driver of our positive conviction for growth assets but now we are seeing some shadows in the picture here and there.

To be clear, an analysis of our macroeconomic indicators – be it our Nowcasters or our Newscasters – clearly shows that the recovery in the vast majority of economic zones is not in doubt. Yet, with the volatility that we have seen in recent times in economic figures, our indicators show unusual volatility levels. At the beginning of December, Chinese consumption figures experienced a singular decline, plunging our Chinese growth Nowcaster below the recessionary threshold. However, this situation resolved itself a few days later and our indicator returned to positive on 1 February.

Then it was the turn of the US to show volatility. To put it into perspective, US indicators plunged to unprecedented lows in March 2020 as containment took hold. When it ended, these same indicators rebounded in proportion to their fall. Since January 15, 2021, a spectrum of indicators have begun to show signs of erosion. For example, the ISM manufacturing index’s “new orders” component reached highs in early January (67.5) not seen since the recovery of 2003. Such levels are generally unsustainable in the medium term, and it has since begun to normalise rapidly, falling back to 61.1 early last week. The same is true for retail sales, consumer confidence indices, overall employment figures, and surveys of wages and investment expectations.

All of this is not necessarily worrying at this stage. These various figures have seen pronounced upward movements, reflecting the intensity of the recovery in the US, just as the Chinese consumption figures reflected the intensity of the country’s recovery. Europe is only slightly affected by this phenomenon: the intensity of the fiscal stimulus was lower and this can be seen today in the speed at which its figures are increasing. Overall, it seems difficult at this stage to see this decline as a signal beyond the noise of variations. This is all the more the case since our Newscaster indicators remain indicative of good economic conditions in China, Europe and the US. For the moment, our systematic indicators show that we are not on the verge of a recession.

Consistent exuberance

Perhaps what concerns us more is market sentiment. It was positive in December but became exuberant in January. Two figures provide some perspective on this idea of exuberance. The S&P 500 index is more than 400 points above its 200, 100 and 50-day moving averages, and it’s not the only one. All of the world’s major equity indices are also above their 200-day moving average and 98% are above their 50-day moving average. US equities are up an average of 3.26% over 50 days, European equities are up 1.99% and Asian equities are up 3.23%: the upward movement is broad, deep and affects all global equity markets. The second figure is an intra-index figure. Within the S&P 500, 85% of its constituent stocks are above their 200-day moving average. The last two months in equity markets have been truly exceptional, both in the magnitude and consistency of the upward movement. It seems clear to us that the sense of euphoria that currently drives investors is exaggerated and that current valuations are a significant risk. Moreover, our Market Stress Nowcaster is showing rapid variations, reflecting the volatility that markets could potentially experience at the slightest catalyst, be it health, economic or a communication error by a central bank. The market is currently being driven by anticipations and promises. Let’s hope that the former are justified and the latter are met.

Ambitious valuations

The main consequence of this investor craze for equities is elevated price levels. The S&P 500’s PE ratio is now 25 but this overall figure hides strong disparities between sectors: Consumer Discretionary has a PE of 36, the Energy sector has a PE of 32 while Financials are at 13. However, it has become very difficult to interpret these figures for two reasons: the level of rates and the extent of variations in company results.

An important part of last year’s market recovery was due to the sensitivity of many equities to interest rates. This is a well-known channel of monetary policy that has been exploited for several decades. Estimates vary but the 1% drop in rates in 2020 explains between 10 and 20% of the recovery from the end of March. Rates remain low to date, maintaining the valuation of shares at high levels. Our equity valuation metrics, which subtract rates from earnings yields, are therefore in neutral territory as the rate effect counterbalances the rise in prices.

The second element is the magnitude of the earnings variations. S&P 500 company earnings declined 13.7% in 2020 and are expected to rise by 23.5% in 2021. In the case of the Stoxx Europe 600, the decline to date stands at 18.6%, with an increase of 32% expected by analysts in 2021. So how can we judge high share prices in February 2021 using PE ratios? Using “trailing” or “forward-looking” data gives very different figures, creating another source of confusion when assessing the prospects of equities today.

Time for neutrality

Thus, we find ourselves today in a situation where, on one hand, the image conveyed by the economic figures reflects a degree of uncertainty that the markets still seem to be totally ignoring. On the other, these same investors have propelled equities to high levels without considering fair valuations. At this stage, we believe that a neutral dynamic positioning makes sense from a tactical perspective. We have therefore considerably reduced the biases of our dynamic allocation: we are now neutral on growth assets globally, and only exposed to energy and commodity currencies as far as our active inflation bias is concerned.

Unigestion Nowcasting

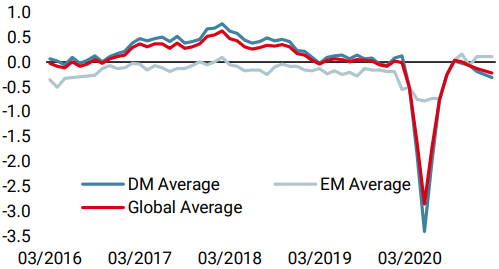

World Growth Nowcaster

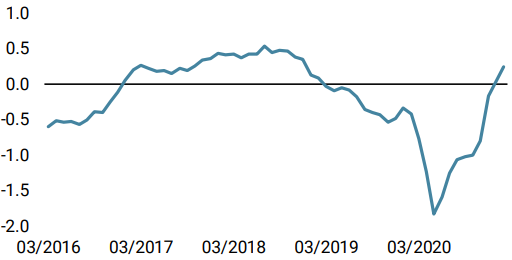

World Inflation Nowcaster

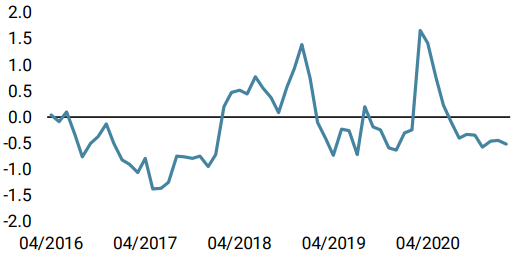

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster declined, as European, Canadian and Japanese data lost some ground.

- Our World Inflation Nowcaster increased again last week, mainly driven this time by European data.

- Our Market Stress Nowcaster decreased last week, showing yet another sign of the market exuberance.

Sources: Unigestion. Bloomberg, as of 5 February 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).