Stock markets have shown signs of resilience lately, despite dire macroeconomic data and mixed newsflow on the pandemic front. The fight between central banks and the impact of containment measures on growth is raging, but investor sentiment remains of the essence. As long as unlimited support persists, downside risks to holding risky assets will prove limited. Nevertheless, dispersion across and within asset classes remains elevated, market breadth is nowhere to be seen and the ripple effects of the current economic meltdown have yet to be measured. Cautiousness and selectivity remain key to navigating these cross-currents, as well as a deeper look beneath the surface to assess whether the current sentiment shift will be long lasting, or short lived and fragile.Sentiment Shift Vs. Macro

Cautious Man

After a few weeks of waiting to see the true impact of the pandemic in the economic data, we now are in no doubt that recession is here, well established, and large. As measured by the diffusion index of our proprietary Growth Nowcaster, 68% of its 700+ component data series are deteriorating, and the level of the indicator itself indicates a level of activity comparable to the 1990 and 2001 recessions, with a strong probability that it will drop to 2008 levels. Surveys and leading indicators have already plunged either to, or below, these levels: The German IFO of business expectations is 10 points lower than 2008 levels while, in the US, Philadelphia and Empire state business conditions indices have plummeted to unprecedented levels: -80 and -57 respectively, compared to -40 during the GFC. US unemployment rose by 26m in a month (approximately 10% of the labour force), and the nature of the shock makes it hard to tell whether most of this job destruction will recover in the near future. Every segment of the economy is taking a big hit, with investment, consumption and expectations being the most severely affected. Current GDP economist forecasts for 2020 are for a contraction of -3.4% in the US and -5% in Europe, in line with pandemic research which, under a “core scenario”, points to a contraction of -3% in the US and -4% in Europe. The key to resolving a very complex economic equation is to compare the negative impact from quarantine measures with stimulus promised by central banks and governments. So far, the response has been appropriate, massive and sufficient to weather the shock (a priori), with a total of USD 4tn in promised money between asset purchase programmes and loans to the economy bundled in COVID-19 special packages. However, more than the scale of the current damage, it is the duration of the pandemic that is the most important factor. It will be determined largely by the effectiveness of quarantine measures and the time it takes to create a vaccine. After focusing on the devastating economic impact of the virus in terms of human loss and on economic growth, investor sentiment has turned more positive. We remain of the view that the impact will be longer lasting than currently anticipated, but have market participants become overly optimistic, and is sentiment therefore still fragile? Given the dismal macro context, sentiment looks, from the surface at least, overly optimistic. The MSCI All Country World index is down ”only” 15.9% year to date, after posting a strong 6.9% rise in April, as of 24 April, and up 23% from its March 13th low. The S&P 500 is showing even better figures, down 11.6% year to date and up almost 10% in April. Obviously, the unprecedented amounts that the Fed has thrown at financial markets to keep liquidity afloat and safeguard against systemic risks is the main factor behind such a rapid recovery. The “focus shift” by the investment world has been phenomenal, switching from “the current economic meltdown is the worst since 1929’s great depression” to “no matter what happens, central banks and governments will save the day”. However, it appears that this view is not shared across a wide spectrum of market participants: fixed income, credit, commodities and equity risk takers do not convey the same message. Dispersion is becoming extreme across and within these different asset classes, while breadth – the proportion of stocks advancing versus those declining – has reached alarming levels. Bond investors, primarily driven by economic developments in growth, inflation, and quantitative support, are reflecting a deep, prolonged type of shock. Global sovereign yields are only 9bps shy of recent historical lows of 0.50%, despite the supply wall created by trillions of dollars of fiscal support to the real economy. The US 10y Treasury yield has been trading in a tight 0.75-0.55 range since late March and yield curves remain pretty much flat, with the US, German and UK 2y-10y segment trading at 37bps, 23bps and 22bps respectively, an indication that future growth and inflation in particular will not recover soon. Initially, credit spreads saw very positive momentum linked to growing risk appetite and the inclusion of sub-investment grade names in the Fed and ECB’s respective corporate purchase programmes. However, they have started to widen again and disconnect from their equity peers. In the US, risk-adjusted returns from high yield credit spreads vs the S&P 500 have delivered a level of underperformance not seen since the GFC on a weekly basis. Creditworthiness has been strongly deteriorating, and defaults are expected to surge materially to double-digit levels in the next 12 months. In the commodities world, dispersion between precious metals and growth-driven energy is striking. Gold is up 17% year to date, while the first WTI futures contract plunged 77%, having fallen into negative territory for the first time ever as demand collapsed and storage space for freshly pumped oil became scarce. Longer-dated contracts currently indicate supply and demand could find a balance later this year, with the 12-month vs 1-Month contango spread standing at USD 14, a level not seen since December 2008. Finally, within equities, only a limited number of sectors have fuelled the rebound, namely Tech, mega caps and defensives such as Healthcare. Energy and Consumer Discretionary names in the S&P 500 are on average 50% below 52-week highs, while IT, Staples and Healthcare are only down 10%. Breadth, measured by the percentage difference between index and median stock distance to highs is extreme, indicating that a very concentrated number of stocks are thriving. This has historically been a leading indicator of large drawdowns, and it questions the strength of the current “rally”. As a result, the share of the five largest S&P 500 companies has reached a stunning 20%, higher than ever before. Investors have favoured quality, blue chips, defensive and highly profitable tech names over cyclical, small cap, value names. Thus, in spite of the questions around sentiment strength, investors have not moved into value (traps?) yet. For now, analysts are pricing a 20% earnings contraction for 2020, which is consistent with current levels of negative growth expected this year. However, expectations also incorporate a meaningful recovery in 2021, implying that containment measures will not be prolonged or renewed. According to our calculations, current market levels are discounting 0% earnings growth over the year and we remain of the view that equities actually still look expensive. Finally, the current positioning in growth related assets seems low: the significant deleveraging that occurred over the last few months saw a reduction by half in equity exposures on average in multi asset funds, whose beta to stocks dropped from almost 0.4 to below 0.2. Systematic leveraged strategies have been forced to do the same, as volatility spiked and remained elevated. A stabilisation in sentiment for risk assets will lead to a soft landing in volatility, mechanically pushing these strategies to increase their exposures. This is an important element to keep in mind, as it could well give the rally some legs. The competing forces described above lead us to remain cautious with regards to asset allocation. Uncertainty remains elevated, as does volatility and broader risk measures, which sytematically keep our risk reduction mechanisms activated. In terms of dynamic asset allocation, our preference goes towards investment grade credit and precious metals, at the expense of high yield and emerging credit, and cyclical commodities. Indeed, central bank purchases of high grade paper in the secondary market will help support the asset class, also favoured by yield hungry investors, while speculative-grade spreads do not seem well aligned to future default expectations. Considering the possibility of a continued push higher in equity markets, we seek to gain exposure via convex optional structures to help dynamically improve upside participation, should sentiment continue to grind higher.What’s Next?

Recession is settling in

Has sentiment really improved?

De-lever and stay selective

Unigestion Nowcasting

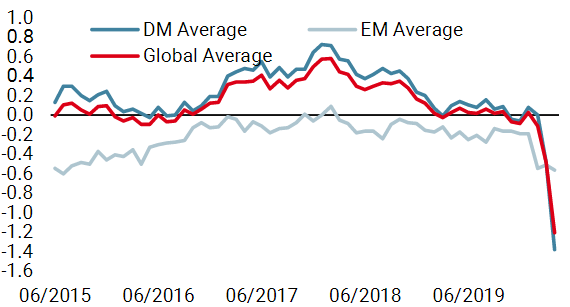

World Growth Nowcaster

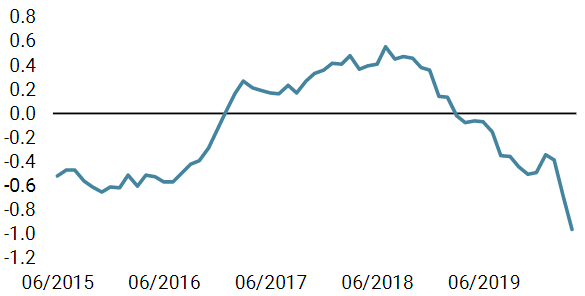

World Inflation Nowcaster

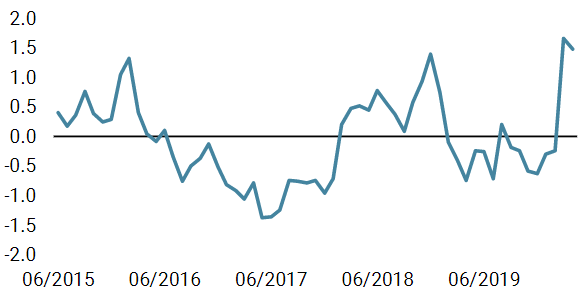

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster decreased again last week, mainly in the US, Canada and the UK. Our world indicator has now reached a value of -1.21 standard deviations, indicative of a very high risk of recession.

- Our world Inflation Nowcaster also fell, mainly in Canada, the US and Switzerland. This decline mirrors what is happening on the growth front.

- Our Market Stress Nowcaster remained stable last week as all three components (liquidity, volatility and spreads) showed comparable stability.

Sources: Unigestion. Bloomberg, as of 24 April 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).