With the third quarter earnings reporting season behind us and investors looking at what’s ahead for equities, it is helpful to distinguish between short-term and longer-term factors. Over the short term, the context for stocks looks supportive, if perhaps less so than it did a couple of months back. However, pressures are building that may become significant headwinds for some firms. Though it is difficult to know when these pressures will hit a tipping point, in our view it seems too early for callin’ it quits, thinkin’ in a bad way, losin’ your grip.Equities: Short-term positives, but headwinds gathering

Sunflower – Post Malone & Swae Lee, 2018

Sunflower

The third quarter of 2019 was a difficult one for firms. For constituents of the S&P 500 index, aggregate sales grew by 3.6% over the previous year but earnings were down 1.0%. Firms in the STOXX Europe 600 index saw their aggregate sales up slightly at 1.0%, but earnings growth was flat at 0.2%. Profit margins contracted further, though they remain elevated for both regions (10% for the S&P 500, 7% for the STOXX Europe 600). Interestingly, increased costs were mostly attributed to higher tariffs rather than wage pressure or other typical causes as firms looked to have absorbed the impact of the trade war on their profit margins rather than increase the prices of their goods. However, market moves are based on expectations, and the low expectations going into the earnings reporting season helped support stocks: 79% of firms in the S&P 500 had a positive earnings surprise, while for the STOXX Europe 600 the figure was 57%. While earnings expectations for 2020 are on the high side (10% globally), they are relatively muted for this year (under 1% globally, with the US a bit above 1%), indicating that a strong finish to the year would be a modest positive surprise for the market.What’s Next?

Short-term factors remain positive

Looking beyond corporate fundamentals, we continue to see supportive factors for equities in the short term. Global growth has remained stable around potential for a few months now and, if the peak tariff impact is behind us, it could pick up as expectations about the future improve. While the markets look to have priced out a few tail risks (trade war, Brexit, etc.), they do not look to have priced in a healthier growth scenario. Indeed, the primary component of a principal component analysis of a broad basket of asset returns – the growth factor – has improved markedly since the beginning of the year, but it remains below its levels from late 2016 when global growth was also stable around potential. Furthermore, flows into global equities have been strongly negative over the year, especially among retail investors. Interestingly, institutional flows started turning a few months back and now appear to be net positive, though not sufficiently so to offset the drag of retail flows that are only now showing signs of turning.

As we communicated last week, valuations have started moving up for equities so they are no longer cheap, but that is not to say they are very expensive. For example, the P/E ratio for the MSCI ACWI index is currently at 15.8 on a 12-month forward basis, just a touch above its long-term average of 14.4. Even splitting between developed and emerging markets does not change the picture much: the MSCI World index (developed markets) has a current P/E of 16.4 vs a long-term average of 14.9 and the MSCI Emerging Markets index has a current P/E of 12.3 vs a long-term average of 11.5. Moreover, from a cross-asset perspective, the dividend yield for most equity indices is above the local government 10-year bond yield, a reflection of the even more expensive valuation of sovereign nominal bonds.

While the picture for stocks looks fairly positive to us in the near term, there are clouds gathering on the horizon we are closely watching. First, monetary policy has been the major tailwind for stocks this year. For instance, EPS for firms in the S&P 500 have been essentially flat this year, while the 10-year bond yield has fallen about 100bps. Holding the equity risk premia constant, this change in the discount rate would imply about a 20% price return, accounting for nearly all of the 24% return on the S&P 500. However, barring a significant economic slowdown in 2020 (which is not our base case), monetary policy looks likely to be on hold for most of 2020, removing an important support for equity markets. Easy financial conditions have allowed firms, especially in the US, to finance themselves via borrowing at low rates. For much of the post-GFC expansion, this higher leverage was offset by rising profits. Thus, while net debt for the Russell 3000 index on aggregate has grown consistently every quarter for the last five years, it has remained at about 1.5x EBITDA steadily until the last couple of quarters, when it hit 2x as net debt growth outpaced profit growth. Of course, the aggregate picture can obfuscate pockets of risk, but when we look more granularly, the picture is concerning but not worrisome: since 2010, net debt as a multiple of EBITDA has picked up for US firms but remains below the levels seen before the GFC. Indeed, the median firm’s net debt is now 2x EBITDA, but that is well below the 3.5x multiple it averaged from 2002 to 2006. The same picture holds for firms’ interest coverage ratios – they have deteriorated but are not alarming. However, if these trends continue, either due to more borrowing, higher interest rates or declining earnings, investors may start to question the ability of firms to maintain profitability in the face of their debt obligations.However, we are keeping an eye on long-term factors

Finally, fiscal policy in the US will move to the forefront of investors’ minds early next year as we move into the presidential primary season. From statements made thus far, it looks like all of the current Democratic candidates would reverse the 2017 tax cuts, including lifting the corporate tax rate from 21% back to 35% (at least). As the tax cuts led to a nearly one-to-one improvement for EPS, it is likely that EPS would fall by about 14% if the tax cuts were reversed, a significant headwind for US equity prices. However, in order to enact such a rollback, the Democrats would need to control both houses of Congress, and their chances of flipping the Senate remain challenging.

If we start to see an alignment of strong polling for a Democratic presidency along with control of the Senate, the downside risks to US equities would grow significantly.

Though these risks are significant and we do not think they should be ignored, they are still far ahead on the horizon. In the meantime, the environment for equities remains positive and we believe there is room for some additional upside over the next few months. There are certainly risks on our radar, such as a deterioration in trade negotiations, but they are not part of our central scenario and so we prefer to position for them via optional structures and maintain our pro-equity bias.

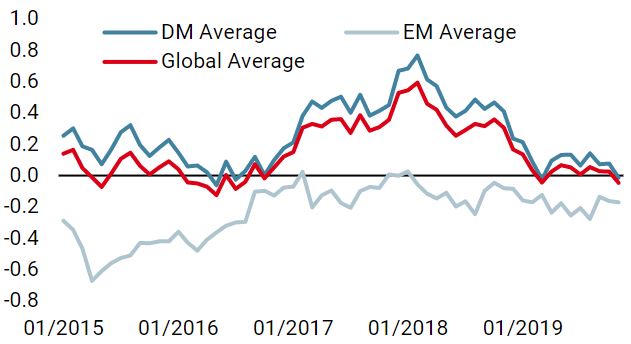

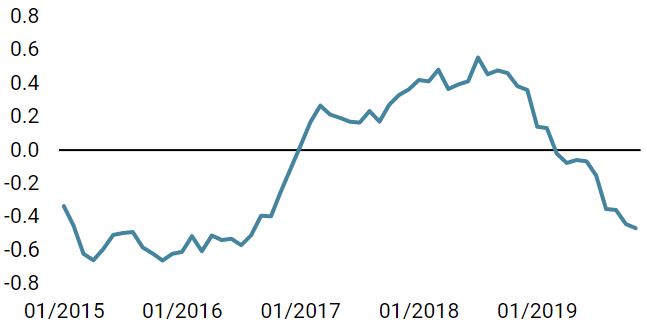

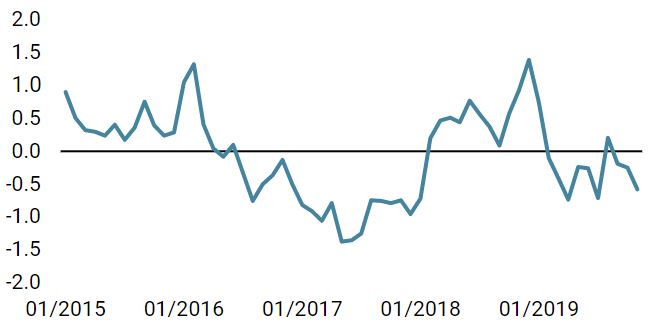

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster declined last week. However, 50% of the data is still improving and growth stabilisation remains on the cards.

- Our world Inflation Nowcaster decreased again last week and inflation risk remains low.

- Market stress remained stable last week, as the liquidity deterioration was offset by lower implied volatilities.

Sources: Unigestion. Bloomberg, as of 25 November 2019.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).