The news of a COVID-19 vaccine and a Democratic US president has reduced global uncertainty, helping on both macro and sentiment fronts. The macro situation looks solid for now even if pockets of risk remain. The vaccine situation is more likely to improve than to deteriorate, supporting sentiment, which now shows positive indications for the future of growth assets. Although valuations are increasingly a risk, we believe the combination of positive sentiment and macro pictures warrant a more positive stance on growth assets. We are beginning to see the light at the end of the tunnel.

The Light at the End of the Tunnel

What’s Next?

The macro situation is less at risk

The main reason why investors were not more bullish before this week was the fog of uncertainty clouding the outlook for 2021 and into 2022. “Will markets see through the lockdowns?” is a question often used by many market commentators, expressing the view that investors will need to look past the current temporary shock for markets to rise. Do today’s lockdowns matter more or less than what will happen in the future? Investors were in search for longer-term perspectives and this week they found them. A Democrat US President for four years and a tentative vaccine against COVID-19: these two pieces of news bring two conclusions. First, the level of uncertainty is now lower – for a year this factor has played a significant role; second, it forces investors to finally focus on the medium term more than the shorter term. After all, all lockdowns so far have been temporary and followed by a strong catch-up in consumption growth (as in the US) supported by a lot of economic stimulation. With the vaccine, lockdowns are moving from potential recession triggers (as it was the case in February-March) to potential market stress triggers: from a more fundamental element to something more technical. This difference is a net positive for our dynamic allocation.

This is all the more true as the growth situation remains solid for now: that is the key message from both our Nowcasters and Newscasters across a majority of regions. The US and Chinese Growth Nowcasters have declined recently while remaining, respectively, around the zero line (growth around potential) and above it (growth above potential). US durable goods consumption is not in a good shape (but low rates could help there) while external demand is unlikely to support the Chinese economy for now. The European lockdowns will weigh on the zone’s economies as indicated by the recent decline of our Eurozone Growth Newscaster. However, for now, the consequences of these lockdowns look much softer than those of the first. With the vaccine gaining traction, the macro situation is likely to be less and less at risk compared to before, as economic agents will increasingly see the situation as temporary, which is essential for continued improvement in consumption and investment. Consumption should benefit from the decline in savings while companies could start spending the significant cash buffer accumulated during the first half of the year. All of that is currently positive for growth assets.

Sentiment is also improving

Sentiment has been delivering interesting indications in recent days, adding marginally more positive elements to the current balance of forces driving asset returns. Two elements are worth noting in our opinion. First, the AAII retail investor survey thus far has been broadly negative in tone, conveying a lack of bullishness. With the announcement of the vaccine, the situation is clearly different and the survey has jumped to levels last seen in 2017. Flows are essential drivers of the performance of equities, and this sudden change in the survey should lead to higher retail flows to equities in the coming weeks and months.

The second essential point in our view is the fact that the beta of macro hedge fund per equity indices has already started shifting from the previously preferred Nasdaq and S&P 500 indices to European and Japanese equities. We read there an encouraging sign of a more balanced progression across equities, with a broader sector-level and geographic participation. The combination of these two elements – retail investors becoming “hotter” and smart money looking to profit from a broader exposure to equities – is an important trigger for our dynamic asset allocation, adding to our pro-growth assets stance.

Not all risks are off the table

We see incrementally more positive elements in the macro and sentiment spaces, but this does not mean that all risks are gone. The current level of pricing is an important risk for the short to medium term. Our valuation metrics show low but increasing expensiveness in growth assets, with credit more expensive than equities. It is mainly the time-series dimension that shows this expensiveness, and with the recent market progression, this metric has increased. Moreover, recent strong performance among past laggards and current PE data offer further support to this expensiveness thesis, with both US and European equities showing PE ratios close to their highest historical levels. The key difference between a conventional PE analysis and our approach to valuation from a cross asset allocation perspective is that we discount the impact of rates: lower rates make higher PE ratios structurally possible. According to our calculations, a simple increase of the whole yield curve by 1% would make our valuation indicators for equities quite negative (i.e. calling an underweight). Pricing risk is therefore significant, and even if we believe that the ECB and the Fed will try to keep rates low, a limited increase in rates would only reflect the positive macro and sentiment backdrop and could add to this valuation risk.

To conclude, our dynamic asset allocation has recently seen an increase in its exposure to growth assets as the macro and sentiment elements are outpacing the valuation risks in our view. We will continue to closely monitor our valuation indicators as that is where the main risk currently lies.

Unigestion Nowcasting

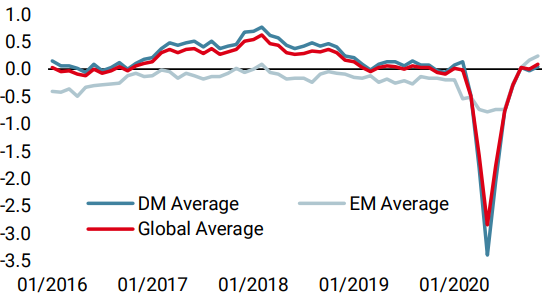

World Growth Nowcaster

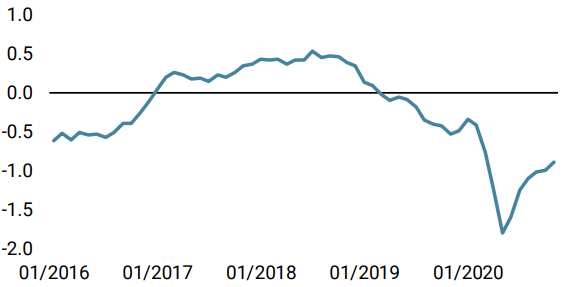

World Inflation Nowcaster

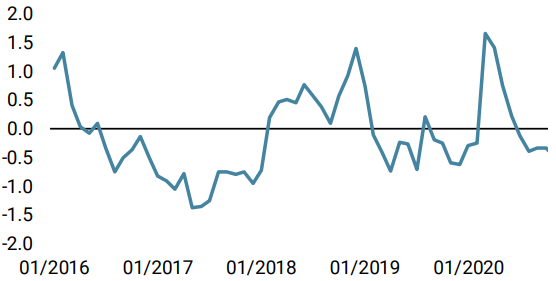

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster increased last week, strongly driven by North American data.

- Similar to the Growth Nowcaster, our World Inflation Nowcaster was also on the rise, driven by US data edging higher.

- Our Market Stress Nowcaster further decreased this week, reflecting the US election outcome and vaccine announcement.

Sources: Unigestion. Bloomberg, as of 13 November 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).