Are We Close To The Peaks?

The first few weeks of the year have been marked by major tectonic shifts in terms of central banks’ monetary policies and market action. The change from an environment of “Goldilocks” to “normalisation” has been anything but gradual, weighing heavily on market sentiment. Investors have tried to rapidly adapt to this new environment, dealing with an ever-growing number of uncertainties: inflation, geopolitical tensions between Russia and Ukraine, asset valuation, major rotations behind the surface and rapidly rising rates. Looking ahead, investors need to assess whether all these negative factors have already been discounted by markets, or if we have reached peak pessimism and calm will be restored soon.

Too High

What’s Next?

The macro environment has peaked…

From a macro perspective, we remain of the view that inflation will cool this year and tightening expectations have gone too far, too fast.

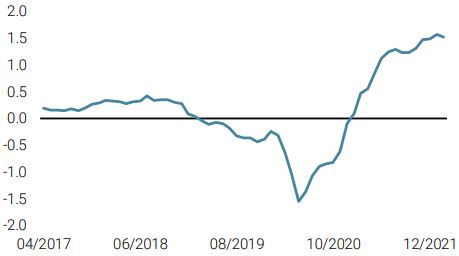

First, let’s not forget that the very high levels of inflation currently observed (and which have led to the swift U-turn from central banks) is coming from both record demand and supply-chain disruptions. The unprecedented combination of massive liquidity injections and fiscal stimulus post the Covid crisis have caused a major positive demand shock (as seen in growth numbers), while the lingering bottlenecks created by the pandemic led to rapidly increasing input prices. As these elements start to fade, actual inflation numbers will start to recede. Our US Inflation Nowcaster has steadied at elevated levels over the last six months, implying a high risk of inflation surprise (which has actually been the case). However, it has stabilised and is not increasing. At the same time, its diffusion index (measuring the percentage of increasing inflation-related data vs. decreasing) has dropped to below 50% (from an average of 70% in H2 2021), driven lower by supply costs, as show in Figure 1.

Figure 1: US Inflation Nowcaster Components – Diffusion Index:

Source: Bloomberg, Unigestion. As of 17.02.2022.

In the meantime, growth has also been slowing and is now close to its long-term potential. Not an issue per se, but it indicates that after a year of record consumption and investment, demand destruction could already be underway due to rising costs/higher prices eating away at corporate margins and consumers’ spending power.

Therefore, we remain of the view that macro normalisation is underway too, with both economic activity and inflation expected to cool off over the course of the year. That is why we also believe that investors’ current expectations of monetary policy tightening have gone too far, too fast.

…and so has hawkishness …

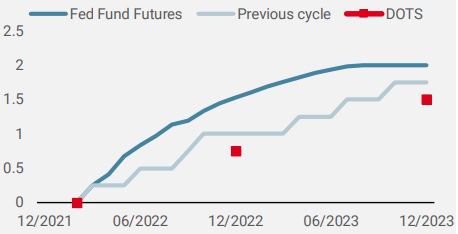

Comparing the current rate hike expectations from the Fed with the latest hiking cycle sheds light on how differently investors expect the cycle to develop. With a total of 150bps of tightening over the next twelve months currently priced in by Fed fund futures (or six 25bps hikes), expectations are: 1) much more aggressive than indicated by the dot plots (three hikes in 2022 and three hikes in 2023); and 2) for a much faster pace of increase compared to the 2016-2018 cycle when hikes occurred gradually, on a quarterly basis, as shown in Figure 2.

Figure 2: Comparison of Tightening Expectations

Source: Bloomberg, Unigestion. As of 17.02.2022.

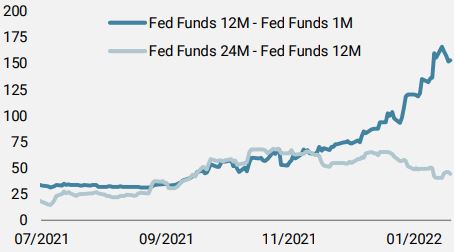

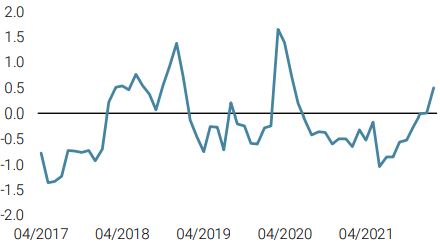

The divergence accelerated massively in January, as shown in Figure 3, buoyed by declarations by policy makers and strong CPI prints. For years, changes in forward guidance were well telegraphed between FOMC meetings to avoid communication surprises leading to major financial instability. In that respect, the next meeting (March 16) will be key in assessing the extent to which the dots and economic projections will evolve. Indeed, market participants could become more uncomfortable if real growth forecasts were to edge lower, while hikes were to adjust higher at the same time. This would increase the risk of a major monetary policy mistake and asset prices could adjust violently.

Figure 3: 12m & 24m Fed funds evolution

Source: Bloomberg, Unigestion. As of the 17.02.2022.

In spite of very hawkish rhetoric from James Bullard (St. Louis Federal Reserve President), the setting of monetary policy is a democratic process where all members of the committee have a role to play. Over the past few days, a number of other Fed members have voiced concerns that moving too fast to fight off inflation could hamper growth prospects, and that the US central bank needs to find the right balance, remain data dependent and act gradually. We therefore believe that given the current macro context and its recent dynamics, a peak in hawkishness may have been reached, at least for now.

…but sentiment has weakened

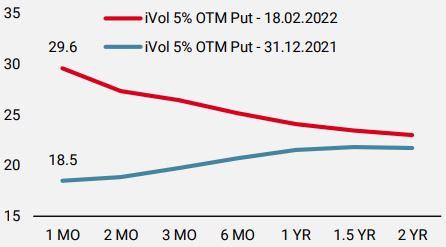

These rapid changes in monetary expectations have taken a toll on investors’ sentiment, with deleveraging occurring in most asset classes in the form of a correlation shock (when major risk premias fall in concert). Implied volatility has risen sharply as a result, investors rushing to short and medium term hedges against a protracted correction in equity markets. Volatility curves switched from their traditional contango to backwardation, indicating a very high sensitivity to short-term events, as pictured in Figure 4. Current levels of volatility imply average daily moves in excess of 1.5%, which is well above actual realised volatility, even with the recent instability in markets.

Figure 4: Implied Volatility – S&P500

Source: Bloomberg, Unigestion. As of 17.02.2022

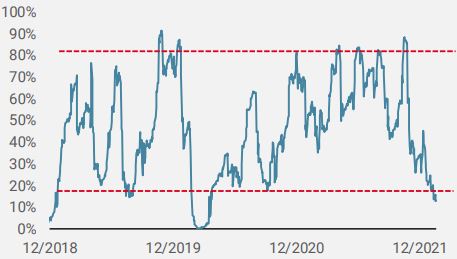

On the other hand, risk appetite has been on a downward trend since late last November, and levels are now either at or close to extreme pessimism, as shown in Figure 5. So, even if it may be too early to call a market bottom given the uncertainties surrounding macro developments, monetary policy and geopolitical matters, this is a constructive factor over the medium term.

Figure 5: Complacency indicator – S&P 500

Source: Bloomberg, Unigestion. As of 17.02.2022

Conclusion

“Goldilocks” is now gone for good, leaving in place a harsh transition to “normalisation” and investors trying to adjust their assets allocations. After years of stellar market returns, back to normal means a less rosy economic context and lower expected returns ahead. Yet, it does not mean that there will not be opportunities. As long as real growth remains positive and central banks manage to avoid a major mistake, we believe that markets have already taken significant steps in adjusting to this new backdrop. Being nimble will be key to navigate these more perturbed, less linear market dynamics.

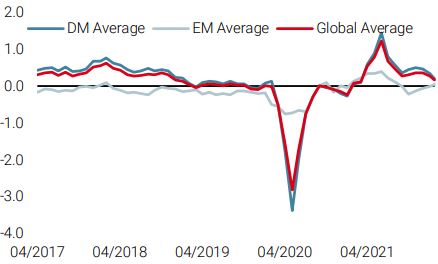

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster moved modestly lower as the US economy continues slowing and production expectations in Canada and UK housing declined as well.

- Our World Inflation Nowcaster ticked up slightly, largely due to higher inflation pressures from the US and China.

- Our Market Stress Nowcaster moved higher last week on the back of deteriorating liquidity while volatilities remained elevated and spreads wide.

Sources: Unigestion, Bloomberg, as of 21 February 2022.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).