Following the extraordinary monetary and fiscal stimulus and resulting economic boom stemming from the pandemic, inflation risk increased significantly, forcing central banks to acknowledge its non-transitory nature. Although the future course for central banks is clear, it is by no means uniform and responses differ largely across the globe. Many emerging market central banks have already tightened considerably to combat inflationary forces. Developed world central banks took their time, however, to acknowledge that inflation was here to stay and only recently started to change their tone. The timing of this shift in language and forward guidance was exacerbated by the recent appearance of the new Covid omicron variant. What can we expect from central banks going forward?

Spotlight

Central Banks

Central banks post the pandemic crisis

By definition, a central bank is responsible for overseeing the monetary system and policy of a country, regulating its money supply and maintaining price stability as well as moderating long-term interest rates. Depending on the region, some focus more on employment, others on inflation, although most now have a dual mandate, trying to find the right balance between the two.

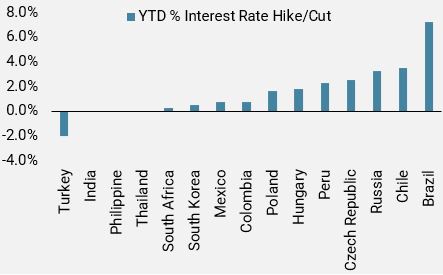

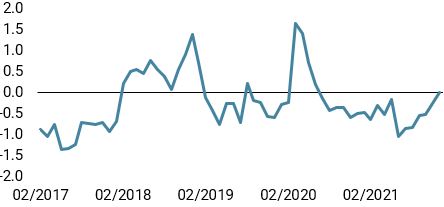

The hangover left by last year’s Covid 19 crisis resulted in different approaches by central banks and governments – some were a lot more pro-active in supporting their economies, which meant that the road to normalisation was marked by large dispersions. In emerging markets, those differences materialised at an unprecedented scale; for example, the COPOM (Brazilian Central Bank) has so far hiked rates by 725bps this year alone and continues to signal that more are on the way in an effort to aggressively combat double-digit inflation. The Reserve Bank of India (RBI), on the other hand, has so far stayed put and kept rates historically low at 4% to stimulate economic growth further, after having been particularly hard hit by the pandemic. Turkey, which has one of the highest inflation rates among emerging market countries, has taken a very different approach and decided to cut rates, a costly mistake that has seen the Turkish Lira plunge by over 50% year to date, despite numerous interventions in the foreign exchange market by its central bank. China is another clear outlier, currently easing while the rest of the world has moved towards tightening. Emerging markets have a long history of having to “manage” inflation compared to developed markets, where inflation tends to be less “sticky”. Nevertheless, emerging markets are a good case study to illustrate the large dispersion in central bank responses, which will probably continue to widen. The message is clear however, normalisation has started and accommodation is gently but surely fading across the world as illustrated in Figure 1 below.

Figure 1: Emerging Markets YTD % Interest Rate Hike / Cut

Source: Unigestion, Bloomberg as of the 15.12.2021

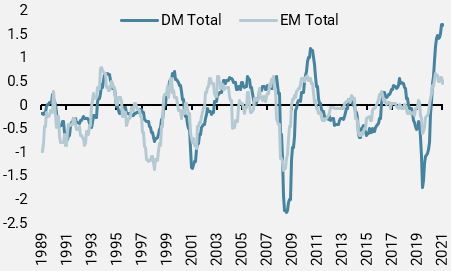

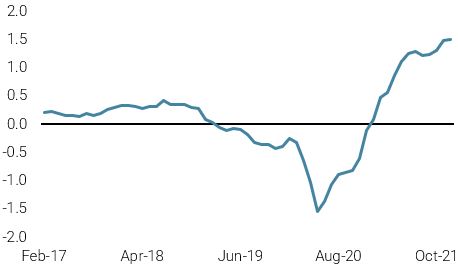

Inflation: After more than a decade of deflation / low inflation in the developed world, inflation has made an unprecedented comeback. We have been advocating since late 2020 that inflationary pressures would not be “transient”, as the post-crisis demand recovery would be met by supply and labour constraints. Our Inflation Nowcasters detected this “reflation” narrative very early for both the developed world and emerging markets, which later morphed into a full-blown “inflation” story.

Many developed world central bankers questioned this view throughout this year, until recently. The US Federal Reserve (Fed) finally made a U-turn at the end of November, with Jerome Powell saying it was probably a good time to retire the word “transient” for inflation. Bank of England (BOE) chief economist Huw Pill recently said: “…balance of risks is currently shifting towards great concerns about the inflation outlook, as the current strength of inflation looks set to prove more long-lasting than originally anticipated”. The European Central Bank (ECB) recently acknowledged that inflation in the Eurozone would stay elevated for longer than anticipated, but expects it to fall below their 2% target over the medium term. The normalisation process in the developed world has been slow so far, especially when compared to emerging markets. A few developed central banks are a step ahead however. Last September, Norway became the first country to raise interest rates, stating that it was appropriate to begin a gradual normalisation, given the improving economy. It delivered a further 25bps hike last week. New Zealand also raised rates twice by 25bps to contain inflationary pressures.

Figure 2: Developed and Emerging Inflation Nowcaster:

Source: Unigestion, Bloomberg as of the 15.12.2021

Barring any further crises / tail events, we can expect a continuation of this monetary policy normalisation into next year. That being said, we see the macroeconomic context in 2022 as challenging for a major hiking cycle to start, putting us at odds with current market pricing, notably for the Fed.

Indeed, we believe that inflation will peak next year, as saving rates have declined significantly, leaving no significant pent-up demand. At the same time, new capacity is arriving online and we expect supply issues to ease in the early part of next year. Given the large weight of food, energy and other commodities in headline inflation, we are unlikely to see the same price pressures next year, absent an extraordinary surge in these core components. One argument reinforcing our view is that many commodity markets already reflect supply outweighing demand or rising inventories via their forward curves, which are currently in backwardation. This should give central banks room to let policy shifts flow through and to assess their impacts before engaging further in aggressive tightening.

Covid uncertainty has not derailed central bank trajectory

Interestingly enough, the Fed’s latest hawkish shift comes at an unfortunate time as uncertainty rises over the appearance of yet another new Covid variant – omicron. The Fed was well behind the curve until the last December FOMC meeting last week, when it aligned itself with market pricing by tapering the pace of asset purchase to $30bn a month, which will thus conclude in March 2022. The updated dot plot shows the median rate forecast for next year at 3 hikes and about the same for 2023. The message during the press conference was clear, stronger than expected inflation and employment data reduced the need for “easy money”. We believe that the Fed rate hike pricing might be too aggressive at this stage. If history is any indication, the Fed has largely remained cautious over the last few years instead of aggressively tightening. In addition, the Fed’s terminal rate between 2% and 2.5% is among the lowest in history and thus supportive for the broader economy. Finally, the upward revisions for CPI and growth for 2022 and 2023 are limited and reflect our view that inflation should peak sooner and gradually converge towards the inflation target. According to the latest dot plot and economic forecast, real rates should stay in negative territory at the end of the tightening cycle, which could also be the first time in history.

Therefore, despite the overall hawkish headlines, we believe that the context should remain favourable for markets and macro momentum. The omicron variant could also be a dovish factor for some central banks if the situation deteriorates. Although the August 2021 delta variant turned out not to be a game changer for the economy and the markets in the end, some central banks are more sensitive to these kind of events. Recall the Reserve Bank of New Zealand (RBNZ), which decided to delay a fully priced hike due to the discovery of a few Delta variant cases. Last week however, despite omicron spreading like wildfire in the UK, the BOE finally decided to pull the trigger and delivered its first 25bps hike, adding that the new variant could raise inflationary pressures further. Despite increased short-term uncertainty, given current available information and the large proportion of vaccinated people in the developed world, we do not believe the omicron variant will derail the central banks’ normalisation paths.

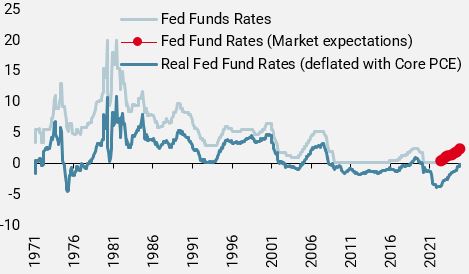

Figure 3: FED expected monetary path and current market pricing:

Source: Unigestion, Bloomberg as of the 15.12.2021

Risk to our core scenario

In 2022, monitoring real rates and yield curves will be key to assess to what extent the expected tightening by the world’s major central banks could derail the bullish trend in both earnings growth and returns for growth and real assets. A combination of faster tapering and inflation deceleration would push real rates higher and weigh on valuations for growth-oriented assets. As discussed, we expect inflation to peak next year. However, should this happen later than we anticipate, central banks could tighten more aggressively with important consequences for markets, where valuations and leverage are both high. Another risk would come from Covid, where vaccine effectiveness wanes and new and more dangerous variants force governments to resort to drastic measures such as lockdowns, disrupting the economic recovery. In such a scenario, central banks would make a U-turn from their recent hawkish stance and revert to stimulating massively to avoid deflation and cascading defaults, pushing bond yields significantly lower.

Concluding remarks

Central banks are back in the spotlight after an unprecedented period of ultra-loose monetary policy. We believe that current market pricing is high and expect fewer hikes than implied, notably by the FED, as inflation should peak. For 2022, we therefore have a preference for secular growth and quality at the expense of value. Regarding the reflation narrative and real assets, after having been exposed to inflation breakevens for several months we have taken some profits, as we consider that current pricing exhibits “perfection” in the continuation of inflation pressure. We see two main risks to our core scenario 1) a faster normalisation 2) Covid once again threatens the recovery / normalisation.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster was steady as most countries saw little change in their growth dynamics.

- Our World Inflation Nowcaster ticked up slightly due to higher inflation pressures in the US and Australia.

- Our Market Stress Nowcaster was steady as volatilities remain elevated and spreads have yet to retrace.

Sources: Unigestion, Bloomberg, as of 17 December 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).