The energy sector has been on a tear lately with supply and demand imbalances pushing certain segments of the market to record highs over a short period of time. The focus on ‘greener’ energy has left the sector largely underinvested for decades and we are now seeing the consequence: strong demand following the Covid crisis has left supply unable to cope in the short term. The resulting increase in energy prices have had a direct impact on supply-side inflation, an important component that explains why inflationary pressures have continued to push higher and not been transitory as initially expected by many central bankers. Below, we take a closer look at the drivers of the recent energy price rally to see if it is likely to be a short-term phenomenon or a long-term trend.

Energy

What Happened?

Energy: A broad-based rally driven by supply / demand imbalances

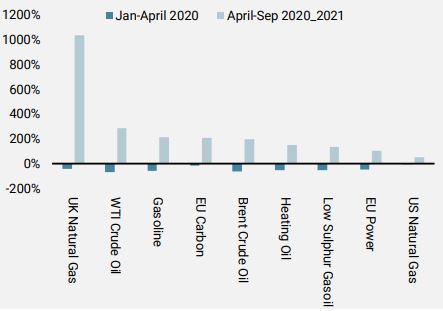

While many investors tend to focus on oil, the recent energy rally has been broader with the entire energy sector ripping higher. All sectors suffered at the peak of the Covid crisis last year but the rally that followed has dwarfed the initial pullback, taking many by surprise. This can clearly be seen in Figure 1 below, which compares the January-April 2020 correction versus the rally that followed.

Figure 1: Energy Pandemic Correction vs Subsequent Rally In %

Source: Bloomberg, Unigestion, as of 30.09.2021

Gas has attracted the most attention given the extreme price action, notably in Europe. The situation in the UK made the headlines as it went through a perfect storm of rising demand, declining stocks and a lack of external supply. The UK ranks as one of the lowest in Europe for natural gas storage capacity – less than 1% of Europe’s stored gas is held in the UK. Much of Europe therefore depends on external supply sources, notably from Russia. Sky-high energy prices are creating further price pressures by pushing some UK energy companies out of business. Since the summer, it is estimated that around ten utilities companies in the UK have been forced to close and more are expected to follow the same fate as we approach winter when peak demand typically starts. A large part of the UK’s electricity is generated by gas-fired power plants and recently, the main power cable used to import electricity from France was destroyed in a fire. The energy crisis we are currently experiencing in Europe is therefore real and will not be solved overnight, as the supply response from an underinvested sector will take time to react.

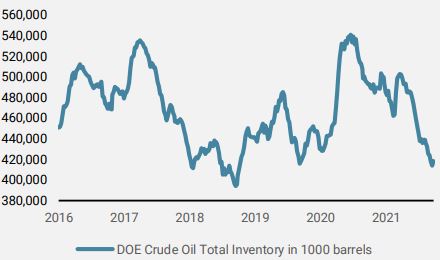

Crude oil is the energy asset class with the largest impact on the consumer and the economy, central to many industries and the world’s most important energy source. Its supply/demand balance is therefore central to the recent rally. Following the reopening of world economies post pandemic, oil demand has been strong and started to deplete inventories. This can clearly be seen in Department of Energy (DoE) total crude oil inventories, which are now back towards their 2018 lows and down 22% from their pandemic peaks.

Figure 2: DoE Total Crude Oil Inventory in 1’000 Barrels

Source: Bloomberg, Unigestion, as of 30.09.2021

The recent hurricane Ida also paralysed the Gulf of Mexico and its oil production, further adding to the bullish rhetoric for oil and gas. Just under 1.5 million barrels of oil and 1.7 billion cubic feet of natural gas come out of the Gulf every day. Although production has restarted, some oil companies have already announced that some of their platforms will not be operational until next year due to the damaged incurred.

It is no secret that oil is also a favoured trade by hedge fund / macro players to hedge inflation risk. With inflationary surprise risk still in very high territory according to our in-house proprietary indicators, where all components of the indicator continue to persist at historically high levels despite the disappearance of base effects, one can expect inflation hedge demand to remain firm. Prolonged supply disruptions combined with multiple media reports of an “energy crisis” should keep sentiment positive towards the asset class. The positioning of other sentiment components is also far from extreme or stretched levels, leaving scope for more buying from the speculative community going forward.

OPEC: The elephant in the room?

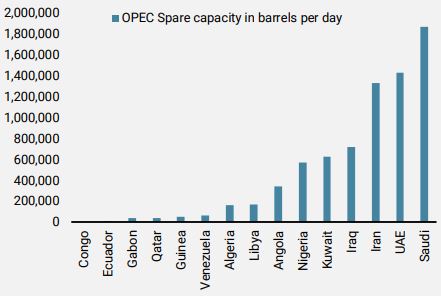

OPEC has chosen to adopt a strategy to gradually increase oil output as it expects demand to remain firm in the coming years. Indeed, looking at Figure 3 below we can see that OPEC does have spare capacity and therefore the means to increase production significantly in theory. Without taking into account Iran, for obvious reasons, OPEC spare capacity currently sits at around 6+ million barrels per day. It is worth noting that just under 50% of that spare capacity comes from Saudi Arabia and the United Arab Emirates.

Figure 3: OPEC Estimated Spare Capacity Broken Down Per Member

Source: Bloomberg, Unigestion, as of 30.09.2021

Several OPEC members such as Nigeria and Angola have struggled in recent months to increase output, again the result of a decade of underinvestment or maintenance that has constrained their ability to increase supply. The potential increase in supply from spare capacity therefore rests primarily on the two largest producers, Saudi Arabia and the UAE. However, it would be counterproductive for them to increase production materially or pre-emptively at this stage despite recent pressure from the US administration, which is currently in communication with OPEC and looking for solutions to address the sharp price increase issue.

What is likely to be the result from this Energy crisis?

Interestingly enough, one of the main reasons why we are in this situation today is the lack of investment over the last decade due to the push towards a “green” revolution. Sadly, the current power crisis is pushing many countries to return to one of the most polluting methods of energy production: coal burning. The subsequent increase in coal burning and energy consumption has pushed the price of carbon to record highs. As an example, China coal consumption has hit record levels this year as the country tries to deal with the energy consumption boom. This increase in carbon emissions has benefited carbon offsets / allowances, explaining the sharp rally in European carbon futures to record highs last week.

We can expect a supply reaction down the road as current prices make it profitable to start new projects, but this will take time. For instance, the number of US oil rigs has increased significantly from pandemic lows and currently stands at around 420, up from 172 in summer 2020. Given the latest price action, numbers should continue to rise to reach their pre-pandemic levels of just under 700. Expected oil-well start-ups confirm such estimations.

We also suspect that governments will be keen to make sure we do not end up in a similar situation in the future by pre-emptively increasing storage capacity, or so-called strategic reserves. This should effectively keep demand healthy as many of these reserves have been slowly but surely depleting. In the US, DoE petroleum reserves are now back to 2003 levels, down from peaks reached in 2011.

Watch out for the winter

The weather element is an important factor for energy markets. Winter can bring large price spikes and a very cold winter often results in soaring demand for heating purposes. Winter seasonals are typically reflected in the forward curve of certain energy markets such as natural gas, where winter months trade at a premium. A colder than average winter could prove catastrophic for the already tightly supplied energy markets. Some governments in Europe have already started to implement measures to help cope with the surging costs on households resulting from the spike in prices. France for example is giving out “energy cheques” to the lowest income households. Spain has adopted emergency measures to cap energy prices and profits. This will likely be a key topic at the EU Summit at the end of October.

Concluding remarks

Commodity markets, and particularly energy markets, play an important part in the inflation narrative. We continue to believe in a high inflation surprise risk, which should continue to support energy prices. The tight supply / demand balance should remain in play as long as the macroeconomic recovery continues to unfold. A decade of underinvestment resulting from the shift towards greener alternative sources of energy will not be reversed rapidly. Although we can expect more supply down the road, the reality is that it will take time. We have recently witnessed a slowdown in macro momentum but the overall growth picture remains above potential and thus supports our call for an overweight in real assets. Another supportive element is the valuation argument; indeed, the oil market currently remains backwardated, which means long positions result in a positive roll yield. The weather element will also be an important component over the next few months, when peak demand usually occurs.

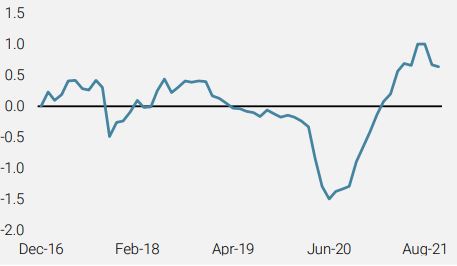

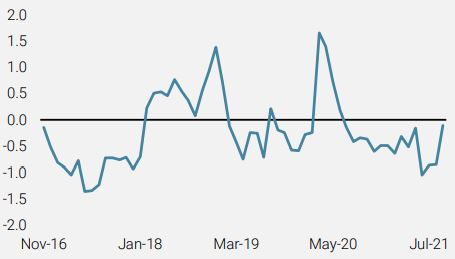

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster moved further down, primarily driven by Europe and Japan

- Our World Inflation Nowcaster was steady with varying changes across countries offsetting.

- Our Market Stress Nowcaster rose further over the week as volatility rose and spreads widened.

Sources: Unigestion, Bloomberg, as of 01 October 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).