Interest rates have been edging downwards for a couple days now, begging the question: is this the end of the “reflation/inflation” trend? We understand that current inflation figures fall below the expectations of most market observers but we think that the signs point to a solid inflation surprise in the coming months. Some markets remain unconvinced but, for now, we retain “inflation surprise” as our core scenario. The positive performance coming from the fixed income world is temporary and more red numbers are yet to come. Here is why.

Deborah Conway

What’s Next?

Reflation is finding its way to markets

For the past four months, the inflation theme has underpinned the lion’s share of our publications, our portfolios and the performance of financial markets. Our “inflation” basket, which tracks the pricing of this risk using a cross-section of market returns, has so far sent a very clear signal. Its Sharpe ratio since the beginning of the year has put this basket at the top of the ranking of the four macro regime baskets we monitor. It has generated a Sharpe ratio of 3.22, above the very strong “growth” basket, whose Sharpe ratio in 2021 is “only” 2.59. At the opposite extreme, the Sharpe ratios of the “recession” and “market stress” baskets are respectively -3.67 and -2.90. From this analysis, there is little doubt that inflation risk pricing has appeared across markets, causing Q1 to be one of the worst quarters for fixed income securities (-2.51% for global governments bonds). This means that, to a certain extent, expectations have increased around the inflation topic. What does the data tell us?

The first signs of reflation

While the pricing of this risk has kept portfolio managers and financial market observers busy, inflation has yet to be fully reflected in published data – although it is still showing an uptrend. In the US, the consumer price index for Q1 rose by 2.6% year-on-year, slightly surprising economists to the upside (the consensus was for 2.5%). In Germany, the same figure is already at 2%. The index in France went from a 0% change in September to 1.4% in March. This is not just a European or American development: in Norway, inflation is at 3.1%; in Asia, Chinese inflation went from -0.5% in November to 0.4% in March, while Korean inflation went from 0.1% in October to 1.5%. While high inflation is not here yet, all global consumer price indices have started to recover towards their long-term levels. More interestingly, an analysis of the components of these indices clearly shows the different elements that explain this recovery in inflation. In the US in particular, a significant number of inflation components are in positive territory: real estate, food and medical costs have maintained a positive growth rate. Transportation and commodities sectors have begun to recover and should benefit from strong base effects. While the transportation sub-component continues to show negative year-on-year growth, its recovery is extremely rapid: year-on-year growth has dropped from -9% to -2% in just a few months, and should turn positive by June at the latest. A similar trend can be observed in Europe. The components currently recovering in European consumer price indices are remarkably consistent with those observed in the US.

The great consistency

A trend seems to have begun, and this trend should continue in the quarter ahead. Several elements seem to point in this direction. First, producer price indices began to rise sharply in March, reaching 4.2% in the US and 4.4% in China. On average, the year-on-year changes in these price indices stood at 3.8% in March, compared with -3% in May. In addition to this strong increase in input prices, wages are showing signs of strength. In the UK, unit labour costs rose by a remarkable 7.2% from Q4 2019 to Q4 2020. The Atlanta Fed Wage Growth Tracker shows a 3.4% increase in wages in February, while the employment cost index in Q4 showed a solid 2.5% increase. Finally, in Germany, wage growth rose from -4.5% in Q2 to almost 0% in Q4. Interestingly, the Fed’s inflation nowcaster for the year ahead shows a very rapid increase: since the beginning of the year it has moved from 1.2% in January to 3.3% today. This does not take into account the fiscal stimulus that has yet to be fully unleashed on the economy and remains stored largely as savings (the US households’ saving rate remains at 13.6% as of February). Finally, our own nowcasters and newscasters are delivering the same message: inflation surprise has rarely been so high as today, with our indicators reaching levels in the top 10% of values. Finally, 70% of the data aggregated by our World Growth Nowcaster is improving. High and rising: for us, this is the very definition of an inflation shock.

Forecasts behind the curve

In spite of these observations, inflation forecasts are still lagging. First, economists’ forecasts are increasing for 2021 and 2022 but are still quite slow to react to the data that is currently being gathered. In December, economists were expecting 2% inflation this year, but have revised that number to 2.5%. Their 2022 forecasts have barely evolved, remaining at 2.1%: inflation is not considered sustainable. Based on an historical regression over the 1990-2020 period, the increase in producer price indices alone is enough to see core inflation in the US reach 2.5% in July 2022 due to lead-lag relationships. What about financial markets’ perception of the inflation risk? The government bond market is probably the most at odds with our expectations, with nominal rates losing the ground it had previously gained. The inflation market is showing more reactivity: the two-year inflation breakeven has now reached 2.71%. Ten-year inflation breakevens remain capped at 2.30% for now, and the five-year/five-year forward inflation breakeven has breached the 2% line but is struggling to go higher. Finally, it is interesting to note that the Conference Board consumer confidence inflation forecast for the next 12 months shows significantly higher readings at 6.7%!

Keep your inflation hedges

Our assessment lies somewhere in-between. Inflation should reach the 3% mark and then exceed it: the demand shock still lies ahead of us, not behind us. Crossing the 3% mark historically leads to very different performance patterns across equity factors – supporting value and costing momentum – and is usually negative for bonds and positive for commodities and commodity-related currencies. This therefore remains our position for the moment. The level of rates seems capped for now but we remain convinced that the materialisation of inflation risk in inflation figures that should happen over Q2 will act as a wakeup call for markets.

Unigestion Nowcasting

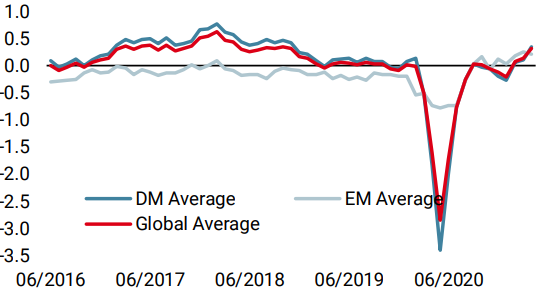

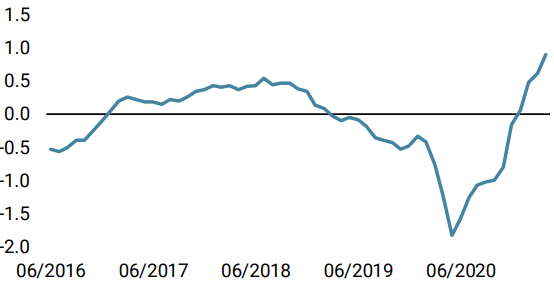

World Growth Nowcaster

World Inflation Nowcaster

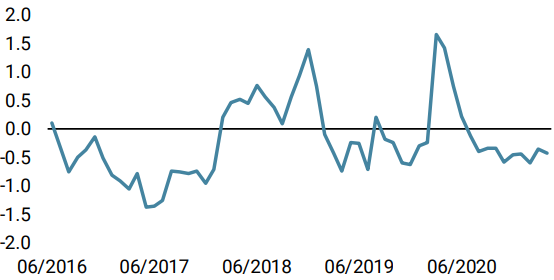

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster increased again significantly on strong US data releases for March and April. Recession risk is therefore solidly anchored at the “very low” level.

- Our World Inflation Nowcaster increased again, this time quite broadly across developed economies. Inflation surprises are likely.

- Our Market Stress Nowcaster remained stable over the past week, with most of its components doing the same.

Sources: Unigestion. Bloomberg, as of 16 April 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).