Co-creation: taking our relationship with investors to the next level

At Unigestion, we don’t believe innovation is just about launching lots of new products. Against a hugely challenging backdrop for investors, innovation must serve a purpose: in our eyes, it’s all about co-creating with our clients the investment solutions that meet their needs. In this paper, we explain the importance of co-creation and provide some examples of how we have been able to help our clients through this partnership approach.

Written by Fiona Frick, Chief Executive Officer

BACKGROUND: A CHALLENGING TIME FOR INVESTORS

Institutional investors find themselves in an extremely challenging environment, for the following reasons:

- Bond returns have slumped, and equity returns are weakening. In this high-equity-volatility/low-yield environment, investors are facing significant challenges in terms of how to achieve adequate returns with traditional asset classes.

- Bonds used to act as the safety valve in a multi-asset portfolio, but with bond yields having plummeted, they cannot fall much further, limiting the protection they can provide when stocks fall.

- Asset class correlations have increased. It is perhaps unsurprising that many asset classes are moving in tandem as they are being carried along by the same tide of central bank liquidity.

- Negative market events are becoming more frequent. This is a consequence of reduced market liquidity, fewer market makers and the more widespread use of automated trading.

In short, what worked in the past is unlikely to work in the future. As a result, asset allocation models need to be overhauled, in our view.

THE CHANGING FACE OF ASSET ALLOCATION THEORY

In the old days, things seemed much simpler. In the 1950s, Modern Portfolio Theory and the Capital Asset Pricing Model (CAPM) suggested that a simple 60% equity/40% bond portfolio (the “tangency portfolio”) would produce the best risk-adjusted performance. It was supposed to deliver a return of around 10% per year with similar volatility. And this is what it did, more or less, between 1950 and 2009.

In the 1990s there was a wave of new research: Fama & French updated CAPM theory, while Haugen & Baker highlighted the benefits of low-volatility investing. The result of this research was that asset classes became segmented into sub-asset classes, such as value, small-cap and low-volatility in equities, and government and investment-grade & high-yield credit in bonds.

…what worked in the past is unlikely to work in the future. As a result, asset allocation models need to be overhauled, in our view.

In 2000, David Swensen, the CIO of Yale Endowment, highlighted the benefits of diversification and allocating to less-liquid assets. The performance of this approach during the tech bubble increased the uptake of his model, which was seen as the origin of institutional investors’ alternative bucket.

And in the past few years another wave of innovation has occurred, fuelled by the 2007–08 crisis. Even though most institutions had diversified their portfolio holdings across equities, bonds and alternatives before the crisis, they had underestimated the level of equity risk their portfolios were exposed to. This meant that diversification didn’t work. The boundary between traditional and alternative assets has blurred as the same risk factors affect equities, hedge funds and private equity.

As a result, the concept of diversification has drastically changed. As our understanding of the different systematic factors that affect returns has improved, diversification has moved away from investing in different asset classes to investing in the different risk factors that drive those asset classes. The main idea is to aggregate risks to understand correlations and diversify not only by asset class, but also by risk exposures.

It seems that each time there is a crisis, asset allocation theory changes. Will this new investment theory prove more powerful than the old? Time will tell. At least it is grounded in the solid principles of risk management.

WE’RE HERE TO HELP

What does all this mean for our relationship with our clients? It means that we as an asset manager need to work harder to achieve the returns you need. It also means we need to work closely alongside each other so that together we can meet your goals.

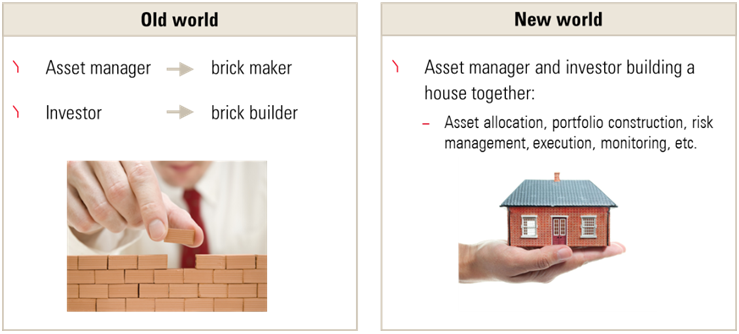

This is very different to how it used to be. In the old days, investors hired an asset manager to run a segment or a sub-asset class within their portfolio. Investors generally determined their asset allocation themselves, sometimes with the help of a consultant.

It’s a bit like building a home. In the past, we made the bricks, while the client put those bricks together to build the house.

Unigestion is embracing the opportunity to better understand your needs, constraints and challenges and brainstorm with you on the investment solutions you require. This is what we call co-creation.

But in the new world, with segmentation around risk factors, risk management has taken centre stage. This puts greater responsibility on asset managers as risk management is part of our day-to-day job. Unigestion is embracing the opportunity to better understand your needs, constraints and challenges and brainstorm with you on the investment solutions you require. This is what we call co-creation.

Let’s look at some examples of how we’ve co-created solutions with our clients and topics that we’re currently working on.

CASE STUDY: RISK ANALYSIS FOR A CHARITABLE FOUNDATION

A foundation that supports a range of cultural and scientific projects came to us as it needed accurate look-through risk analysis of its entire portfolio so that it could understand its sensitivity to a range of different economic scenarios. It also wanted advice on how to restructure its portfolio if necessary.

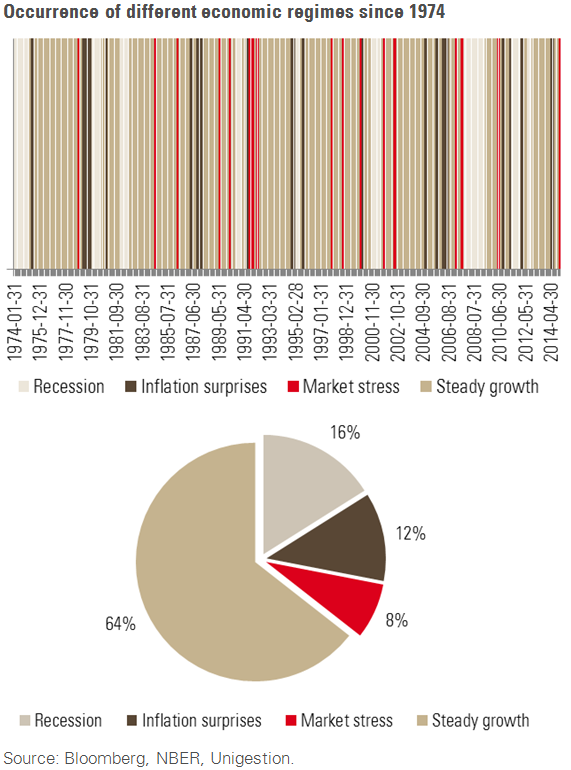

As our investment approach is based on the principle that different economic regimes influence asset class returns, we used some of the methods we have developed in the management of our multi-asset portfolios to analyse the sensitivity of the foundation’s portfolio to different backdrops. As the first step of our approach, we defined four regimes:

- steady growth: a regular increase in the production of goods and services in a mild inflation environment

- inflation surprises: unexpected increases in the price of goods and services

- recessions: sustained, significant drops in output

- market stress: unrelated to the macro phenomena above, markets can behave irrationally and go through periods of stress.

In the graphic below we show the incidence of different regimes since 1974 and, in the pie chart, the proportion of time spent in these regimes.

…our investment approach is based on the principle that different economic regimes influence asset class returns…

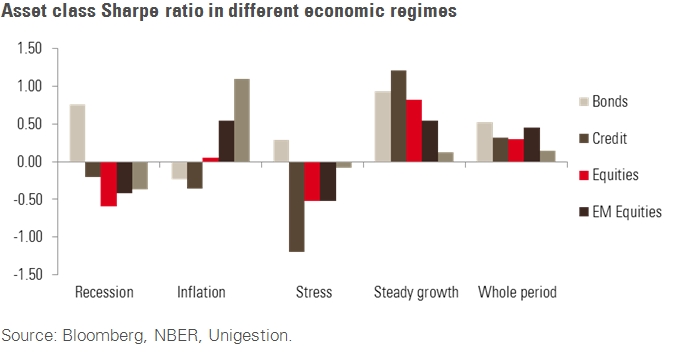

The second step was to map asset class returns to these different regimes. We found that over the long run, the Sharpe ratios of different asset classes were similar to each other, but they differed over the medium term depending on the prevailing economic regime.

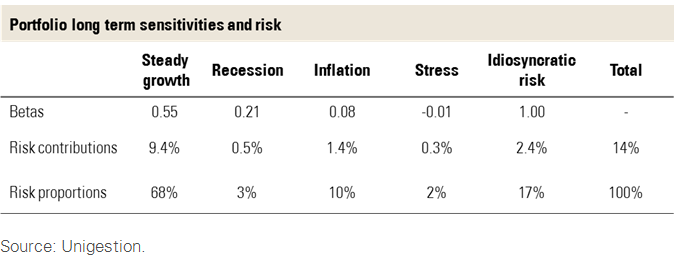

The third step was to analyse the sensitivity of the foundation’s asset allocation to the various macroeconomic regimes.

From there, we discussed with the board if they felt their portfolio was aligned with their top-down view of the economy and the possible adjustments they could make.

Mapping their asset allocation to market regimes enables our clients to see if their portfolios are positioned in line with their expectations. Unigestion is able to provide this kind of analysis to any interested investor.

RPMI RAILPEN

RPMI Railpen (Railpen) manages the assets of the Railways Pension Scheme (RPS) in the UK on behalf of its parent company, the Railways Pensions Trustee Company Limited. Railpen Investments, its investment arm, is an investment manager with assets under management of around £21 billion. The RPS has over 350,000 beneficiaries. In addition, RPMI looks after all the administration and trustees services for a number of third-party clients.

Initially, Railpen had been looking at the underlying drivers of risk and return of various asset classes, and how much they were paying to get exposure to these factors through actively managed strategies. As a result of this review, they decided to restructure their growth fund and move their equity allocations to alternative risk premia. They also decided to bring more management responsibility in-house to reduce their number of external providers, preferring to collaborate more closely with a small number of them for strategic thinking.

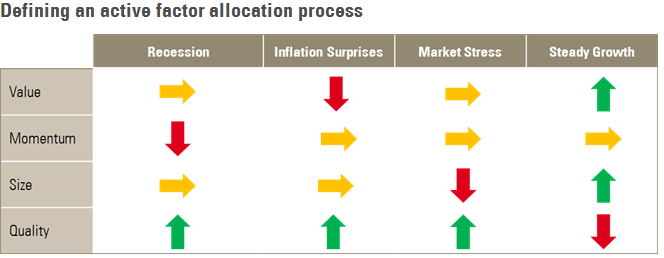

As a result, Unigestion and Railpen have collaborated closely over the past year to devise strategies based on the principle that, individually, factors outperform the index but with variable risk and that Unigestion’s unique approach to active risk management can make these factors more robust. We based this on our 18 years of experience in managing equities according to our 360° risk-management approach and our proprietary macro-risk-based allocation process. We also proposed using enhanced definitions of each factor, allocating to higher-quality value stocks, less-volatile momentum stocks, more diversified quality stocks and more stable small-cap stocks than generic factor portfolios.

Together, we developed a new approach to factor investing consisting of three parts:

- Accurately defining equity risk factors that are proven to add value over the long term and that also make economic sense. We defined four factors: value, momentum, size and quality.

- Constructing a risk-managed portfolio for each of these factors, as each involves considerable “fat tail” risk. We adopted the methodology we have been using for close to 20 years in running our defensive equity portfolios. This gives much more robust results than an equally weighted portfolio as it significantly reduces fat tails.

- Actively allocating across these risk factors, as they are cyclical, and through the different market regimes we referred to above.

The portfolio construction and allocation between these factors is actively determined based on Unigestion’s top-down macro and stock-level risk assessments.

Based on our analysis, we have launched two strategies on their behalf: a long-only factor fund combining four factors, and a long-short, market-neutral factor fund.

Having worked in partnership with Railpen over the past five years, we have a close understanding of this client’s investment needs, and Railpen in turn trusts our investment approach. From here, we expect considerable long-term co-operation between Railpen and Unigestion, particularly in terms of sharing our knowledge and research.

RETHINKING HEDGE FUNDS

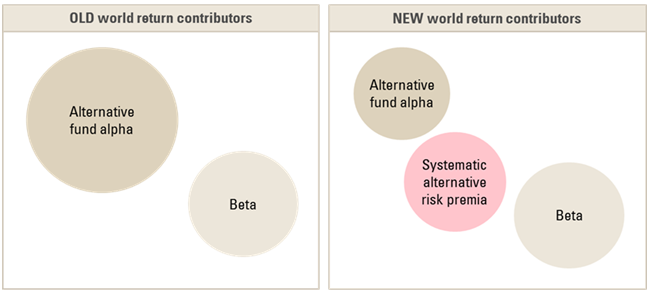

Some of our clients have been dissatisfied with the performance of their hedge fund allocations in recent years. They allocated to hedge funds for their diversification benefits and performance potential, but have been disappointed with hedge funds’ net performance – especially relative to the fees that they charge.

As a result of work that we have carried out on factor-based performance, we have developed a deep understanding of the drivers of hedge fund manager performance. We have found that what might have been considered as alpha in the past can in fact be, to some extent, just a result of exposure to an alternative risk premium.

Previously, alpha was viewed as generating returns that were not related to the market index. Now, it is better seen as return that cannot be explained by some systematic risk factor, so we analysed which hedge fund managers have delivered real alpha that could not be replicated by an alternative systematic factor. The result has been that a number of our clients have replaced some of their hedge fund managers with systematic direct exposure to alternatives, which we can manage on their behalf.

We believe that alternative risk premia are set to play an increasingly important role in investors’ portfolios, especially at a time when traditional risk premium yields are low and volatility may be rising. They can be replicated through liquid, rules-based portfolio-management techniques, making them an attractive option. Examples of alternative risk premia include trend-following, and carry on FX, credit, bonds and volatility. Our understanding of alternative strategies and ability to allocate to specific risk premia mean we are ideally placed to exploit newly identified drivers of returns on behalf of our clients.

CO-CREATION: A NEW ASSET MANAGEMENT MODEL

We believe the days of the old asset management model in which institutional investors choose their allocation and managers just run the assets are numbered. In our view, asset managers need to provide a more all-encompassing service, innovating solutions specifically designed to meet the needs of their individual clients.

This is exactly how we see our job at Unigestion. Managing part of our investors’ portfolios is a big responsibility in itself, but we believe our role goes far beyond that. We see ourselves as the trusted investment partner of our clients, helping them find innovative ways to meet their goals in this challenging environment.

In practice, this means three things:

- sharing knowledge and our research agenda and brainstorming together to overcome our investors’ challenges

- providing analytical support, acting as the outsourced research department of our investors and sharing our modelling tools with them

- designing solutions that meet clients’ exact needs.

Many companies talk about innovation, but innovation is only useful if the end result truly meets the needs of clients. In our eyes, innovation is all about co-creation, working together to create a useful end solution. It is about working “with” our investors rather than “for” them. It is only by working together that innovation can truly help meet clients’ needs.

Important Information

This document is addressed to professional investors, as described in the MiFID directive and has therefore not been adapted to retail clients.

It is a promotional statement of our investment philosophy and services. It constitutes neither investment advice nor an offer or solicitation to subscribe in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Data and graphical information herein are for information only. No separate verification has been made as to the accuracy or completeness of these data which may have been derived from third party sources, such as fund managers, administrators, custodians and other third party sources. As a result, no representation or warranty, express or implied, is or will be made by Unigestion as regards the information contained herein and no responsibility or liability is or will be accepted.

All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information.

Past performance is not a guide to future performance. You should remember that the value of investments and the income from them may fall as well as rise and are not guaranteed. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.