Thus far, 2020 has been a year of superlatives. Macroeconomic fundamentals, policy action and financial markets have all exhibited exceptional behaviours, for better or for worse. Growth has been recovering fast from an unprecedented shock but market trajectories have been uneven, conveying different messages depending on which asset class investors look at. Growth-related assets, equities in particular, indicate a V-shaped recovery, but what about fixed income assets? Does a closer look into government bonds, credit and inflation-related assets reveal the same picture, and if not, why?

Follow the Money

Bonds have always been the macro asset in essence. Growth and inflation expectations are the alpha and omega of the asset class and should remain the key underlying price drivers. The past decade has seen the ever-growing influence of central banks’ unconventional monetary actions and with it disruptions in the expected behaviour of rates (both nominal and real), and more recently in credit spreads given their inclusion in various asset purchases programmes. Rather than reacting to economic fluctuations, central bank actions have now become the strongest driver of economic activity, hence the biggest hand in the fixed income space. 2020 is no exception. A large repricing of the growth and inflation premium triggered a selloff in nominal yields and a widening in credit spreads of multiple standard deviations over a very short period. The average carry on 10-year bonds of major developed countries is 59bps lower today than it was at the end of 2019 (66bps vs. 125bps as of 31.12.19). More importantly, yield curves have shifted in parallel, instead of flattening (with the deterioration in macro anticipations) then steepening (with rate cuts affecting the short end of curves and improving macro expectations lifting the long ends). This is unusual, and indicates two things: This is the reason why yield curves did not bear-steep in the recovery, as they would usually do, and why we remain of the view that yields on sovereign bonds will remain capped for a prolonged period. The balance of powers has clearly shifted in favour of monetary strength and unconventional quantitative programmes. This holds true in the credit space as well: under the influence of combined monetary and fiscal stimulus, designed to backstop what could have been one of the worst default waves on record, credit spreads have recovered swiftly. Current levels on high yield indices would usually indicate above-potential growth levels than the current macroeconomic backdrop and future uncertainties would suggest. Another mismatch in valuation triggered by policymaking. So far, the only asset class displaying a greater sensitivity to economic expectations has been inflation-linked securities. Breakevens took a plunge during the Covid-19 crisis, with 10-year yields dropping 120bps in the US and 80bps in Europe, 90% of which has already been recouped on the back of V-shaped future growth prospects. The simple answer is any meaningful increase – or discontinuation – of support programmes, which makes listening to central banks and governments of paramount importance. For several years, we have been turning FOMC speaker declarations into a quantitative signal, offering a high level of point-in-time correlation with the evolution of interest rates. Upstream, leading information that will influence central bank decision-making are twofold, and can be scrutinised sequentially: sentiment and data on the Covid-19 virus evolution and its impact on the real economy. Indeed, the divergence between what policymakers say and how markets behave has been growing, specifically in growth-related assets: central bank rhetoric continues to emphasise strongly prolonged downside risks yet market sentiment has surged dramatically. Bond investors have been pragmatic instead of being rational: they have front-run asset classes impacted by liquidity injections and we believe this is here to stay. Flows and positioning into supported segments of the universe have been stellar. Speculative positioning is now at multi-year highs in both credit and treasury futures and the average exposure to duration of macro managers remains well above long-term averages. Flows into the largest credit ETFs pushed total assets 85% higher than at the end of 2019 (excluding market effects) in US credit, and 27% in Europe. These divergences from fundamentals have also created side effects in other assets and we believe the impact of these dislocations will last as long as policymakers have the upper hand – i.e., for a long time. Talking about fundamentals and valuations, we estimate the theoretical fair value of US 10-year rates to be around 1.8%, which is 120bps higher than its current yield. As a result, real rates have now plunged deep into negative territories, currently in the region of -1% when discounting expected inflation from nominal rates. Controlled yield curves and money erosion from these negative real rates have therefore been one the main factors behind the recent rush into precious metals – as explained in last week’s edition of Macro Views – and the underperformance of financial stocks. Consequently, the balance of risks in the fixed income universe have shifted to a less favourable stance, even though we do not expect any meaningful upswing in nominal rates or credit spreads on the back of the aforementioned elements. Our preference is still for growth-related assets alongside convex defensive strategies to help absorb unexpected surges in risk aversion.What’s Next?

Macro factors vs. policy action

What will drive fixed income markets in the short run?

Consequences for dynamic asset allocation

Unigestion Nowcasting

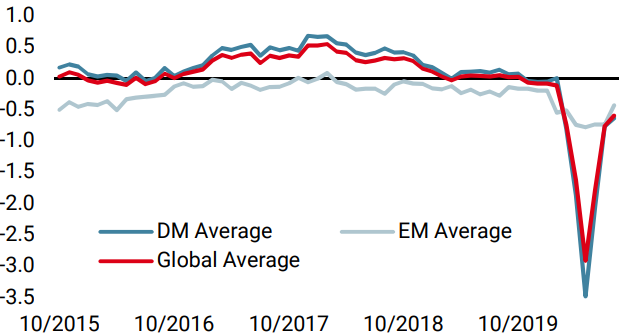

World Growth Nowcaster

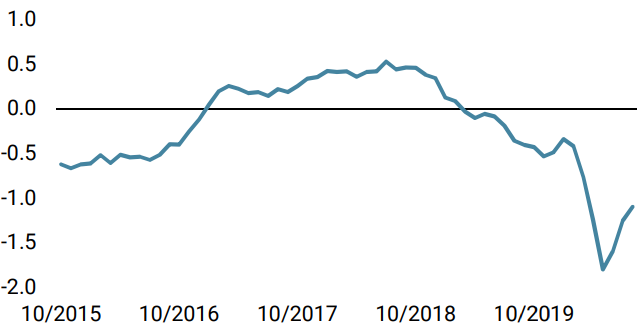

World Inflation Nowcaster

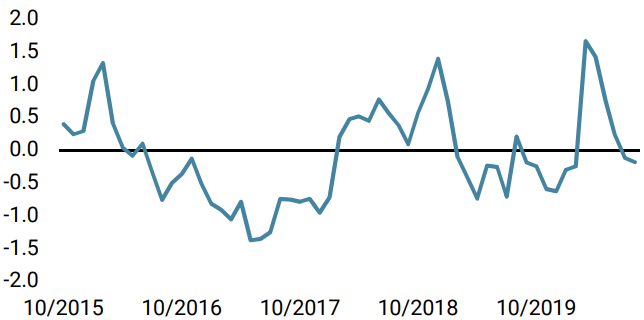

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster stopped progressing last week as US data flow stabilised.

- Our world Inflation Nowcaster increased last week, as inflation pressures increased in the US and the Eurozone.

- Our Market Stress Nowcaster increased marginally as liquidity metrics moved sideways.

Sources: Unigestion. Bloomberg, as of 17 August 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).