Are you really invested in small and mid-market companies?

- We think investors do not have sufficient exposure to the small and mid-market, especially given there is no strict definition of small and mid-market across the private equity landscape.

- By investing in small and mid-market funds, we believe that investors will benefit from: exposure to a large, attractive segment of the economy, greater portfolio diversification and potential outperformance versus large and mega funds.

- In order to effectively navigate the small and mid-market and identify the best opportunities, it requires boots on the ground, local knowledge, in-depth experience and dedicated resources.

Private equity investors are underweight to the small and mid-market in private equity, both knowingly and unknowingly. Knowingly, since they find small and mid-market funds difficult to access. Unknowingly, because their definition of small and mid-market is simply too broad. Indeed, without a clear, strict definition among industry participants, investors may believe they have exposure to small and mid-market companies through investments in funds, which, more often than not, are simply large-cap funds in disguise.

We believe it is important for investors to gain exposure to what we consider the ‘true’ small and mid-market in private equity. So, what is considered the small and mid-market? What benefits does this segment offer? Importantly, how can investors build an intelligent exposure to small and mid-market companies?

What are the characteristics of the small and mid-market?

When we talk about investing in small and mid-market funds within private equity, we essentially speak about gaining meaningful exposure to small and medium-sized enterprises (SMEs).

SMEs make significant and diverse contributions to the global economy. They are varied by nature and tend to be fast growing, ranging from producers of domestic services to global suppliers of digital products, high-quality artisanal goods or sophisticated instruments. In a majority of countries, SMEs tend to account for a significant proportion of total employment. For example, among countries of the Organisation for Economic Co-operation and Development (OECD), companies with less than 250 employees account for about 70% of private sector jobs on average and contribute between 50%-60% to gross domestic product (GDP).

In our view, small firms are also the driving force behind radical innovations that are important for economic growth, since they exploit opportunities neglected by larger, established companies. In certain emerging or high growth industries, such as the environmental sustainability and fintech sectors, SMEs are both critical and leading

market participants.

On the other hand, we believe small companies have some disadvantages compared to larger firms. For example, larger companies can better exploit global opportunities due to their size, which allow them to build a broader customer base and/or source materials

more cheaply.

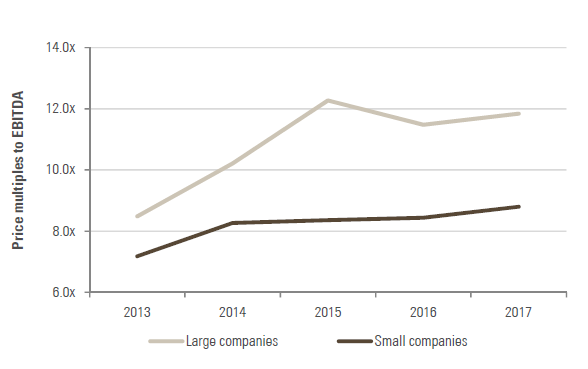

However, therein lies the opportunity for active investors. By their very nature, large companies typically have little room for improvement and tend to exhibit growth more closely correlated to GDP growth. Public and private valuations of large companies tend to be higher, driven by the attraction of investors to stable and predictable dividend streams. Meanwhile, investors in small companies tend to benefit from lower valuations, higher potential for efficiency improvements and more exposure to sectors with little correlation to GDP growth, which together have the potential to drive attractive, long-term returns (see Figure 1).

Figure 1: Average price multiples to EBITDA

Note: Small companies are defined as having enterprise values below EUR 500 million; large companies are defined as having enterprise values above EUR 500 million.

Is there a clear definition of what constitutes ‘small and mid-market’ across the private equity landscape?

In public equity investing, the definition of what constitutes small-, mid- and large-cap companies is exclusively based on market capitalisation.

For private equity investors, on the other hand, there are two recognised ways of defining the small and mid-market segment.

There is no consistent definition of what constitutes ‘small-cap’ across managers.

- Some prefer to define this segment according to the size of a company in a similar way to public equity investing. For example, the European Private Equity and Venture Capital Association (EVCA) defines private equity backed companies with enterprise values of under EUR 25 million as small and under EUR 500 million as mid-market.

- Others prefer to define the small and mid-market segment by using fund size as a proxy for company size. This is principally because there is much more data publicly available at the fund level than at the company level. Therefore, it is relatively easy to compile market statistics to show fund level performance against different fund criteria, such as fund size, geography and strategy. Thomson Reuters, Pitchbook, Preqin and Cambridge Associates all provide private equity performance data at the fund level, categorised by fund size.

Most private equity investors use fund size as a measure to define the small and mid-market; however, there are no consistent fund size definitions applied. For example, some investors within private equity are known to define a small and mid-market fund size as any fund below USD/EUR 2 billion in size. The problem, we believe, with such a broad definition is that, in Europe this would put a local EUR 100 million fund doing niche EUR 30 million enterprise value deals in the same category as a pan-European EUR 1.5 billion fund doing competitive EUR 750 million enterprise value deals. In our view, companies with enterprise values over EUR 500 million start to lose the attractive characteristics and benefits of SMEs.

At Unigestion, we make use of both the above definitions to clearly indicate what constitutes small and mid-market when we invest in SMEs directly and in small and mid-market funds:

- For our investment programmes that directly invest in SMEs, we define such companies as those with an enterprise value of below USD/EUR 500 million.

- For our investment programmes in small and mid-market funds, we adhere to strict size ranges. For our global small and mid-market primary investment programme, we target private equity funds below EUR 750 million in Europe and below USD 1.5 billion in North America.

By using such clearly delineated size ranges, we believe our investors will gain exposure to true SMEs.

What are the benefits of gaining exposure to SMEs?

We believe investing in SMEs through small and mid-market funds, i.e., those funds we define as below EUR 750 million in Europe and below USD 1.5 billion in North America, provides three key benefits for investors:

Among other things, our research findings demonstrate that a diversified portfolio of small and mid-market funds outperformed a portfolio of large funds through various market cycles over the past 20 years.

Exposure to a large, attractive segment of the economy

As we already mentioned, SMEs are the single biggest contributor to GDP in the OECD. Furthermore, we believe investors are able to benefit from low valuations, efficiency improvements and exposure to sectors with little correlation to GDP growth.

Diversification

The key factors that create investment value in SMEs turn out to be quite different to those that create value in large companies. As a result, changes in the macroeconomic environment tend to affect the performance of small and large funds in different ways.

For example, a large company has the ability to raise higher levels of debt than a smaller company does. In periods of high GDP growth, such a company will likely enjoy strong revenue and EBITDA growth. Since the enterprise value of the company will increase according with its EBITDA, the effect of debt means that its equity value will rise at a much higher rate. However, this also means that it could be more vulnerable in recessionary periods with such large amounts of debt on its balance sheet.

Meanwhile, private equity managers typically have more opportunities to improve operationally smaller companies through, for example, the implementation of better information technology systems or investment in manufacturing facilities. In addition, SMEs are more likely to be single country-focused, be more specialised and offer a limited range of products and services. Therefore, under the right ownership, SMEs are able to expand through globalisation, product innovation and the professionalisation of their sales and marketing activities. As a result, we would expect to see a greater proportion of the returns being driven through revenue growth and EBITDA margin improvement in SMEs than in larger companies.

Proven outperformance

There have been numerous studies, which demonstrate that small and mid-market funds tend to outperform large and mega-market funds in the long term. Studies by the British Private Equity and Venture Capital Association (BVCA), the European Private Equity and Venture Capital Association (EVCA) and BNY Mellon provide evidence of historical outperformance of small buyout funds on an internal rate of return (IRR) and multiple basis.

At Unigestion, we have undertaken research in collaboration with Professor Oliver Gottschalg, an associate professor at HEC Business School Paris, to investigate the performance of small and mid-market funds versus large funds (see our Perspectives October 2017, ”Size matters – small is beautiful 2.0”). Among other things, our research findings demonstrate that a diversified portfolio of small and mid-market funds outperformed a portfolio of large funds through various market cycles over the past 20 years.

As an illustration to the above, Ambienta, a private equity manager, acquired Oskar Nolte, a German market leader in solvent-free wood coating systems, for EUR 67 million from its founder in April 2015. Under Ambienta’s guidance, the company hired a new leadership team, expanded into new countries beyond Germany and opened new production and R&D facilities. As a result, revenue grew by over 40%, while the EBITDA margin almost doubled. In April 2018, Ambienta sold the company to Peter Möhrle, a German industrial conglomerate, generating a 3x multiple on its original investment. This is a clear example of i) the high growth potential of a niche market, ii) the multiple ways that private equity managers are able to improve SMEs and iii) the ultimate outperformance potential of investments in SMEs.

So, how should an investor allocate across the different market-size segments?

Out of the total capital raised for buyouts globally, only around 30% is earmarked for the small and mid-market, which we define (as explained above) as funds below EUR 750 million in Europe and below USD/EUR 1.5 billion in North America. If an investor were to invest only 30% in the small and mid-market, we believe they would not have sufficient exposure to this segment.

In our view, a sufficiently diversified global small and mid-market portfolio ought to include at least 30 funds, covering at least three successive vintages.

Taking into account the small and mid-market’s diversification benefits and its potential for overall outperformance versus the large and mega market, we believe that investors should allocate 50%–55% to this segment and 45%–50% to large and mega buyout investments (see Figure 2).

Figure 2: Recommended portfolio allocation

How can investors build an intelligent exposure to the small and mid-market segment?

Globally, there are over 5,000 small and mid-market managers, compared to about 500 large and mega-market managers. In our view, a sufficiently diversified global small and mid-market portfolio ought to include at least 30 funds, covering at least three successive vintages.

In order to deliver the best returns while minimising downside risk, we believe an investment programme should contain the following elements:

In order to effectively navigate the small and mid-market and identify the best opportunities, we believe it requires boots on the ground, local knowledge, indepth experience and dedicated resources.

- Access to top performers. Many of the top-established small and mid-market managers are closed to new investors. In order to obtain access to them, it requires many years to build up the relationships with these managers by, for example, backing them when they were less well known. In addition, investing in emerging managers who are capable of becoming top performers requires a detailed due diligence process in order to develop a high conviction.

- Local knowledge and resources to cultivate relationships. Most small and mid-market managers are single country-based, which allows them to benefit from local relationships for sourcing and managing portfolio companies. Each country or region has its own idiosyncrasies when it comes to regulations, labour laws and company culture. We believe it requires investors having not only the necessary resources, but also the local knowledge to source and cultivate manager relationships in each market.

- Informed views on macroeconomic trends, sectors and private equity markets. The benefit of a global investment programme is that investors are able to exploit the most attractive trends, sectors and investment strategies from each region. Within each country or region, this requires detailed knowledge on the macroeconomic outlook, the attractiveness of each sector and the maturity of the private equity market. With this knowledge, we believe one can select the investment managers or opportunities that best play these investment ‘sweet spots’.

- Disciplined investment and monitoring process. Each investment opportunity must be subject to the utmost scrutiny to determine whether attractive returns are likely to be achieved, while minimising the downside risk. This requires an in-depth due diligence process and active monitoring post the initial investment.

In the final analysis, we think the true small and mid-market offers investors a vast universe of untapped investment opportunities. However, in order to effectively navigate this space and identify the best opportunities, it requires boots on the ground, local knowledge, in-depth experience and dedicated resources. This will not only result in exposure to the most attractive SMEs, but we believe it will also potentially lead to outperformance versus large and mega private equity funds in the long term and provide important diversification benefits for investors’ portfolios.

Important Information

The information and data presented in this page may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this page present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this page contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion.

Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.