Key Points

- Investment slowdown continues while exits rebound

- Fundraising remains strong, though highly concentrated among a few mega funds

- We continue to harness the latest advances in AI to complement our investment process and strengthen our conviction on investment decisions

Overview

We are half way through another year – a good time to take a look back and reflect on the most recent market activity to see what broad trends we can detect for the year to date. Overall, while investment activity remained subdued in Q2, we saw an encouraging increase in exits. To some, this gives the impression that things are beginning to settle down and that the worst might be behind us. However, it is still too early to tell if this was a one-off phenomenon or rather a sign of better times ahead. Nonetheless, it was welcome news to many cash-strapped investors. Despite continued macro uncertainty surrounding interest rates, inflation, and forward-looking growth prospects, there are some encouraging signs that current monetary policy is starting to have the desired effect, easing pressure on the central banks and boosting consumer sentiment. Taken together, there are many reasons to be optimistic for H2.

Investment Slowdown Continues

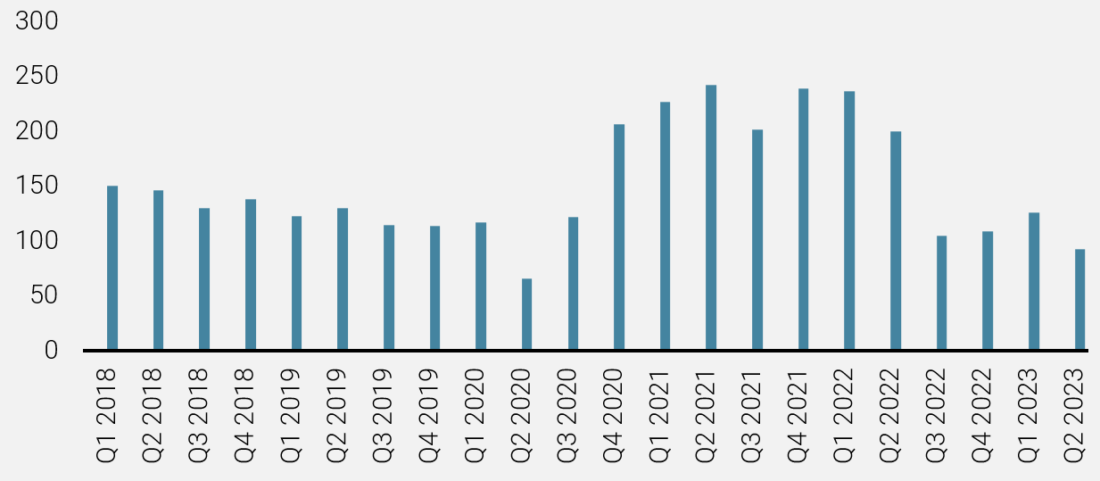

The slowdown in investment activity that started in Q3 2022 seems to be more than just a blip and has continued into Q2 this year, with an aggregate value of private equity deals closed of USD 92bn in the quarter and USD 218bn for H1, representing a 50% reduction over the levels seen in H1 2022 . On the positive side, quarterly investment activity seems to have stabilised, albeit at a lower level of around USD 100bn. And while this looks low compared to the previous 24 months, it is roughly in line with the longer-term average. The combination of interest rate hikes, geopolitical uncertainties, and the continued challenging fundraising environment, have likely made GPs more cautious than ever when deciding where to commit their valuable capital. The slowdown in H1 can be seen across all regions with the US down 67%, Europe down 47%, and Asia holding up the best with a reduction of new investments by only 27%.

Figure 1: Global PE Investment Activity 2018–Q2 2023 Aggregate Deal Value (USD BN)

Source: Preqin, July 2023

Numbers may be down, but we see no shortage of interesting opportunities. We closed several new investments in Q2, one example being a direct lead acquisition of “TecVia” from Springer Nature in Germany on behalf of our direct investment programme. TecVia is a leading provider of digital driving education with a 64% market share in Germany, 53% in France, and 35% in Spain. Going forward, we see significant potential to grow the company organically in its core markets, especially in the area of driving simulators. In addition to organic growth ambitions, we see further potential in selective M&A opportunities. TecVia is a great example of the type of deal we like, combining a strong market position, high barriers to entry, stable and resilient revenues, and attractive growth opportunities.

Exits Rebound

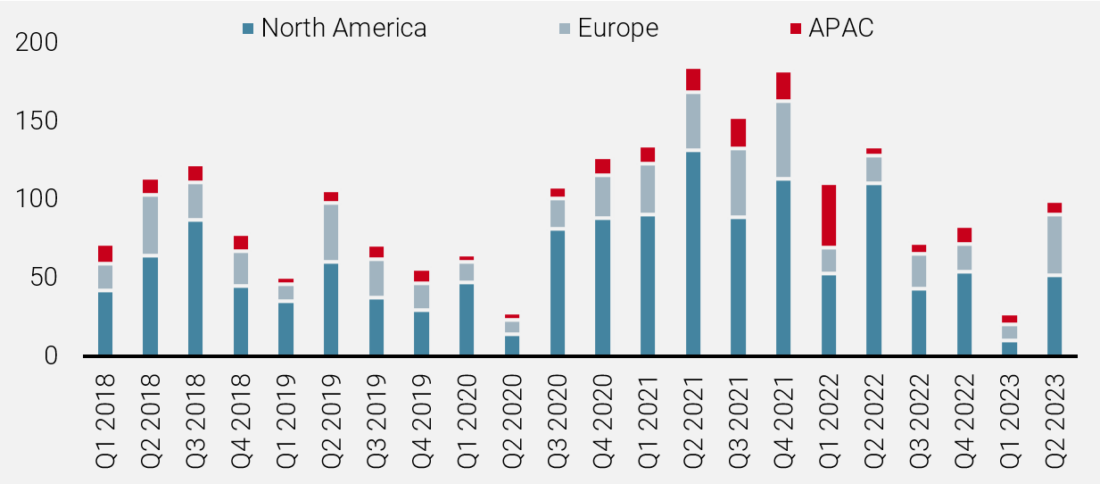

When looking at exits the story is a bit different. While Q1 showed a worrying slump for the start of the year, Q2 has seen an impressive rebound in exits, reaching an aggregate value of USD 99bn[1]. This is in line with what we saw on a quarterly basis in 2022, but still leaves H1 below the level of prior years given the weak activity in Q1. Regionally the US and Asia saw equal drops in exits in H1 (measured by aggregate deal value) of about 65% each, while Europe has bucked the trend thanks to an exceptionally strong Q2 and is now 45% ahead compared to H1 2022. One reason for the increase in exits may be the growing pressure from LPs on GPs to generate liquidity, helping them get their allocations back within range, but also allowing them to allocate new capital in a market environment brimming with attractive options.

Figure 2: Global PE Exit Activity – Aggregate Deal Value (USD bn)

Source: Preqin, July 2023

At Unigestion we had one of our best exit years ever in 2022 and continue to see high quality companies being sold at attractive prices, often at valuations significantly above the latest reported valuation. One recent example is the exit of Wasco, a Dutch HVAC wholesaler in the portfolio of GEM IV, a Benelux-focused fund managed by Gilde Equity Management. The company was acquired in 2019 as an undermanaged subsidiary of a US company. The GP invested heavily in capacity expansion and efficiency improvements, as well as repositioning the company from a “dirty gas” to a “clean, renewable energy” company. It was recently announced that Wasco has been sold to a French strategic player, generating an exceptional return for Unigestion managed vehicles.

Looking at the exit data a bit more carefully, there are two clear observations. Firstly, IPOs as an exit route have become scarce. After a huge drop last year from a peak in 2021, this year is set to come in even lower. On the one hand IPOs have always been highly correlated to the strength of equity markets, so a slowdown is not completely surprising. On the other hand we see companies choosing to stay private for longer. For GPs in the mid-market who tend to focus more on trade sales and secondary buyouts as preferred exit routes, the picture looks decidedly more positive, but is clearly something to monitor. And secondly, there has been a slight uptick in bankruptcies/write-offs compared to last year, which could be an early sign of trouble if the trend were to continue or even increase[2].

Fundraising Strong, or so it seems

Despite a lot of talk about how tough the fundraising market is, the facts initially seem to say otherwise. Aggregate capital raised in H1 amounts to EUR 188bn – 25% higher than for H1 2022 – putting us on track for a potentially record-setting year. Dig a little deeper though, and the story is more mixed. Of the EUR 98bn raised in Q2, 72% was from just five funds. Indeed, the largest fund in Q2, CVC Capital Partners IX, raised a whopping EUR 26bn, making it the largest private equity fund ever raised. In reality, many smaller and lesser-known funds are indeed struggling with fundraising as capital constraints continue to put a dampener on new commitments[3].

But it is not all gloom and doom. Strong GPs with robust strategies are still moving forward with fundraising and the lucky few LPs with capital to commit have an impressive group of funds to select from. We made several new commitments in Q2, including one to BlackFin IV, a leading pan-European manager focused on buyout investments in mid-market companies operating in the financial services industry across continental Europe. The typical businesses it targets will be commission driven (service) and asset light. Unigestion has backed the successful trajectory of BlackFin across Funds I-III and co-invested alongside the manager in numerous deals. Another example is our commitment to Next Capital V, an Australian-based firm targeting lower mid-market businesses in Australia and New Zealand. Though sector agnostic, it tends to invest in sectors such as healthcare, infrastructure and government services, logistics, and financial services. We have built a strong relationship with Next Capital backing the manager since Fund III, as well as completing two co-investments with it.

Dry Powder Steady

The rough equilibrium between investments, exits and fundraising means that dry powder in the market has remained relatively stable, though the overall trend continues to inch upwards. Today there is some EUR 3.8bn in dry powder available versus EUR 3.6bn at the end of 2022 . The biggest increase is in the venture capital space, followed by funds of funds. Given the difficulty in fundraising for these strategies at the moment, GPs are likely to be more discerning than ever when selecting their next deals and holding on to capital longer than usual.

The Explosion of AI

Since the public launch of ChatGPT in late 2022, it has been nearly impossible to ignore the topic of artificial intelligence (AI) – for good or bad – as it continues to dominate the global media. Private equity may not seem to be the most obvious sector when it comes to concrete applications, but should investors reconsider? What if AI could be used as a tool to boost fund manager selection success? Historically, investors have relied on their own experience and, to a certain degree, on their gut feeling to tackle the challenge of fund manager selection within private equity. At Unigestion, we believe this traditional approach can be enhanced with artificial intelligence-based techniques, resulting in superior returns. This belief is based on the potential for such techniques to remove human biases and AI’s ability to provide better understanding of the complex relationships between the factors influencing investment returns.

Combining NLP and ML to Predict the Probability of Investment Success

In 2019, we pioneered the use of machine learning (ML) algorithms to predict the performance of private equity funds ex-ante using quantitative features related to investment strategy, market conditions, and the performance track record of private equity funds[4].

Continuing with this line of research, we have partnered with the University of Oxford, SKEMA Business School, and the Technical University of Munich to broaden the previous work by examining the efficacy of combining ML algorithms and natural language processing (NLP) techniques to predict the performance of private equity funds[5]. The combination of these techniques has proved successful in predicting future stock price movements in public markets. However, in the context of privately-held illiquid investment vehicles such as private equity funds, its application had been uncertain due to a number of factors specific to the private equity landscape where standardised data is both limited as well as private.

The main disclosure document used by private equity fund managers to market their fund offering is the Private Placement Memorandum (PPM). Combining NLP techniques and ML algorithms to extract reliable signals from the investment memoranda of private equity funds helps us evaluate their investment attractiveness without human biases and with a better understanding of the complex relationships between factors influencing investment returns. For example, in our own research we find that „operational (and) financial“, „network relationship“ and „relationship (with the) management team“ among other combinations of words, are positively associated with fund success. On the other hand, „investment criteria“ and „company management“ are negatively correlated with fund success. The beauty of ML lies in its ability to make sense of complex, non-linear relationships among various features and identify patterns humans cannot observe. In a back test, funds selected by the algorithm as having the highest probability of success at the outset of an investment yielded a TVPI 13% higher than the average TVPI of the funds that achieved median performance. Adding this tool to the private equity toolbox has the potential to add true alpha.

The above results outline the potential benefits of using NLP-based methods in combination with ML algorithms in investment decision-making. While this study only relies on textual data to predict fund performance, we believe the combination of textual data with other numerical inputs can lead to better predictive capability and, consequently, better returns. We are still far from replacing human analysts, but these new tools should allow investment teams to better understand the attractiveness of investment opportunities and make more informed investment decisions.

The Private Equity Investment Team,

Unigestion

Unigestion Private Equity Activity

Here are the highlights of some of the investments and exits that we completed in Q2. Reference to specific securities should not be considered a recommendation to buy or sell.

|

In April, we made a primary fund commitment to Next Capital V. Next Capital is an established Sydney-based private equity firm that targets lower mid-market buyout businesses in Australia and New Zealand with enterprise value between AUD 50m to AUD 250m. Next Capital is sector agnostic but is leaning towards several service-led sectors such as healthcare, infrastructure and government services, logistics and financial services. Next Capital’s team has been active in the Australia private equity industry since the early nineties under Macquarie Bank’s umbrella at MDI; they have experience investing through multiple business cycles and have delivered strong returns and proven DPI to LPs. The Fund recently closed its first investment: Country Care, an Australia healthcare products distributor (independently and through national group of resellers), at an entry valuation of 6.9x EV/EBITDA multiple. |

| Also in April, we made a primary commitment to BlackFin IV. BlackFin is a Pan-European manager with several offices across Europe and is advised by a team of 25 investment professionals. The team is highly experienced with a strong network amongst banks and insurance companies in Europe to source off-market transactions. Their focus is on buyout investments in mid-cap companies operating in financial services across continental Europe, mainly France, Benelux and DACH. The targeted business models will be commission (service) driven and asset-light. | |

| Again in April, we made a primary fund commitment to Achieve EdTech Buyout Fund. Achieve EdTech specializes in control buyouts of growth stage companies in software or tech-enabled services companies in the US that facilitate learning. Achieve EdTech is led by a strong team of three who dedicated their careers to innovation in the education space and refined their investment thesis since rebranding the firm from University Ventures to Achieve Partners. Their strategy uniquely invests in the “capital gap” between early-stage and scaled edtech businesses, focusing on target companies that are not a fit for venture capital but have not yet reached scale for traditional buyout funds. Achieve has already closed two deals (one in which we co-invested), giving early visibility in the fund. | |

| In May, Gilde announced an important exit in their GEM IV fund, their largest to date. Wasco is a heating, ventilation, air-conditioning and cooling (HVAC) wholesaler. After initially investing in 2019, they sold to Rexel, a French listed wholesaler, for 9.2x EBITDA. At the time, Wasco did not have a renewable energy focus. It was an undermanaged subsidiary of US-listed Ferguson, serving the Dutch gas heating market but with limited differentiation versus competitors. Together with CEO Herold van den Belt, son of Wasco’s founder, they set out to transform Wasco into the leading HVAC wholesaler, ready for the upcoming Dutch energy transition, by repositioning it from a “dirty gas company” to a “clean renewable energy” company. | |

|

Also in May, we closed a new primary fund commitment in HV Fund IX Venture. HV Capital was founded in 2000 as part of the Holtzbrink Publishing Group and became fully independent venture firm in 2010. Across their eight funds they manage EUR 1.1bn, they have invested in >220 companies, and they realised 127 exits with a consistent multiple of >3x. While they are sector agnostic, they continuously monitor the DACH start-up landscape for attractive sectors and have strong relationship to successful entrepreneurs and angel investors. |

|

In June, we made a primary fund commitment to Riverside Value Fund I (RVF I). The Riverside Company is an investment firm with over 30 years of investment experience across multiple regions and strategies. RVF I identifies and acquires underperforming North American lower middle-market businesses with strong underlying fundamentals that are facing operational inefficiencies or financial challenges. RVF has industry specialization in the following sectors: Business Services, Consumer Brands, Education and Training, Franchising, Healthcare, Software and IT Services, and Specialty Manufacturing and Distribution. Furthermore, target companies typically have USD 60 to 300m of revenue, valuations covered by tangible assets, a conservative use of leverage, and a strong focus on capital preservation. RVF I currently has three platform investments. |

|

Also in June, we successfully completed the direct lead acquisition of Project Lenkrad (TecVia). Project Lenkrad is a carve-out of Springer Nature’s business for mobility education and training solutions. We will acquire 100% of the company and thereafter establish the newly formed TecVia Group. It will be the leading pan-European provider of content and software solutions for driver’s license training and the education and training of commercial drivers with more than 20,000 customers. Going forward, we see significant potential to grow the company organically in its core markets Germany, France, Spain, Switzerland and Austria especially in the area of driving simulators. In addition to the organic growth ambitions, we see further potential in selectively reviewed M&A opportunities. |

|

Again in June, we closed a co-investment in REF Cleanroom, a deal lead by Riverside. With the acquisition of the platform company Dastex and simultaneously closing the first add-on in Sweden, Vita Verita, Riverside is laying the groundwork to build the leading pan-European cleanroom product supplier and value-add distributor. The owner-led company built a leadership position in Germany having longstanding relationships with a large customer base and providing highly mission critical products with the reputation as premium partner to the pharma, healthcare and tech industries. The market is highly fragmented resulting in a great opportunity to acquire additional companies with local dominance to accelerate geographical expansion and take advantage of cost and commercial synergies. |

[1]Source: Preqin, July 2023

[2]ibid

[3]Source: Preqin, July 2023

[4]See the Unigestion Perspectives paper “A Quantitative Approach to Private Equity Fund Selection”

[5]Source: Preqin, July 2023

Important information

INFORMATION ONLY FOR YOU

This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

RELIANCE ON UNIGESTION

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time. Such information is intended to provide you with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf of one or more Unigestion entities will be involved in managing any specific client account on behalf of another Unigestion entity.

NOT A RECOMMENDATION OR OFFER

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Reference to specific securities should not be construed as a recommendation to buy or sell such securities and is included for illustration purposes only.

RISKS

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Unigestion maintains the right to delete or modify information without prior notice. The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, and may experience substantial & sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

PAST PERFORMANCE

Past performance is not a reliable indicator of future results, the value of investments, can fall as well as rise, and there is no guarantee that your initial investment will be returned.

If performance is shown gross of management fees, you should be aware that the inclusion of fees, costs and charges will reduce investment returns.

Returns may increase or decrease as a result of currency fluctuations.

NO INDEPENDENT VERIFICATION OR REPRESENTATION

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

TARGET RETURNS, FORECASTS, PROJECTIONS

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events and are subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. You are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Target returns and/or forecasts are based on Unigestion’s analytics including upside, base and downside scenarios and might include, but are not limited to, criteria and assumptions such as macro environment, enterprise value, turnover, EBITDA, debt, financial multiples and cash flows. Targeted returns and/or forecasts are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

If target returns, forecasts or projections are shown gross of management fees, the inclusion of fees, costs and charges will reduce such numbers.

USE OF INDICES

Information about any indices shown herein is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison. You cannot invest directly in an index and the indices represented do not take into account trading commissions and/or other brokerage or custodial costs. The volatility of the indices may be materially different from that of the strategy. In addition, the strategy’s holdings may differ substantially from the securities that comprise the indices shown.

HYPOTHETICAL, BACKTESTED OR SIMULATED PERFORMANCE

Hypothetical, backtested or simulated performance is not an indicator of future actual results and has many inherent limitations. The results reflect performance of a strategy not currently offered to any investor and do not represent returns that any investor actually attained. One of the limitations of hypothetical performance results is that they are generally prepared with the benefit of hindsight.

Hypothetical performance may use, among other factors, historical financials (turnover, EBITDA, debit, financial multiples), historical valuations, macro variables and fund manager variables. Hypothetical results are calculated by the retroactive application of a model constructed on the basis of historical data and based on assumptions integral to the model which may or may not be testable and are subject to losses. Changes in these assumptions may have a material impact on the hypothetical (backtested/simulated) returns presented. Certain assumptions have been made for modeling purposes and are unlikely to be realized. No representations and warranties are made as to the reasonableness of the assumptions.

This information is provided for illustrative purposes only. Specifically, hypothetical (backtested/simulated) results do not reflect actual trading or the effect of material economic and market factors on the decision-making process. Hypothetical trading does not involve financial risk, and no hypothetical trading record can completely account for the impact of financial risk in actual trading. For example, the ability to withstand losses or to adhere to a particular trading program in spite of trading losses are material points which can also adversely affect actual trading results. Since trades have not actually been executed, results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity, and may not reflect the impact that certain economic or market factors may have had on the decision-making process. Further, backtesting allows the security selection methodology to be adjusted until past returns are maximized.

If hypothetical, backtested or simulated performance is shown gross of management fees, the inclusion of fees, costs and charges will reduce such numbers.

ASSESSMENTS

Unigestion may, based on its internal analysis, make assessments of a company’s future potential as a market leader or other success. There is no guarantee that this will be realised.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority („FCA“). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” („AMF“).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission („OSC“). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority („FINMA“).

Document issued July 2023.