- Global private equity investment grew overall in Q1 2022, driven by North America and APAC, but showed a decline in Europe.

- Despite geopolitical concerns, rising inflation and turbulent stock markets, our portfolio has shown particular resilience and we continue to see a high level of dealflow through our global network of investment partners.

- In Q1 2022, we committed EUR 175.7m to investments, including EUR 44.3m invested in 3 secondary transactions and EUR 39.7m invested in 3 direct investments.

Overview

After a hectic 2021 in the private equity market, we were expecting 2022 to be a calmer affair. Indeed, following a record year of investments, private equity investors would have been forgiven for some respite at the beginning of 2022. As it turne d out, Q1 was busy for some, quieter for others. Overall investment activity continued to increase vs the same quarter in 2021, although this was driven by North America and Asia Pacific. Likely driven by the Russian invasion of Ukraine, investment activity in Europe was lower in Q1 vs one year ago. The story was similarly mixed for exit activity with North America showing a small increase while Europe was significantly down. Meanwhile, despite the headlines of large cap buyout funds targeting larger than ever funds this year, fundraising saw its quietest quarter since the onset of the Covid pandemic. Is this a sign that investors are beginning to show caution?

North America Carries on Regardless

The global aggregate value of private equity deals closed during Q1 was EUR 295bn, 14% up on the same quarter last year1. While activity in North America (+27%) and APAC (+33%) showed particular strength, Europe (-16%) slowed down, likely driven by geopolitical events.

Since the beginning of the pandemic, investment activity in mid-market companies (defined as deals with an enterprise value of less than EUR 500m) has been much more robust compared to large deals. However, in the last three quarters, spurred on by pent up demand, large deals have shown the most activity. The aggregate value of large deals in Q1 grew by 36% while small deal activity was down by 4%. However, this increase came principally from North America and Asia Pacific, where large deal activity was up 67% and 104% respectively, compared to only a 4% increase in Europe.

Meanwhile, despite healthy exit activity in North America in Q1 (+11%), the global aggregate value of exits was EUR 155bn, a decrease of 15% on the same quarter last year. This decline was driven by APAC (-30%) and, most notably, Europe (-46%).

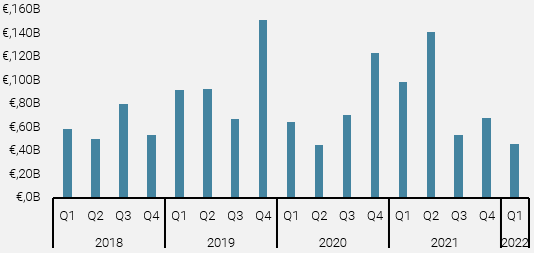

Potentially indicating that investors are holding back, fundraising was materially down this quarter. In Q1 only USD 46bn was raised globally for buyout funds, less than half of the amount raised in the corresponding quarter of 2021 and the weakest first quarter since 20152. Given the high amount that was invested in 2021 and the consequent reduction in dry powder, it was largely expected that many managers would be replenishing their coffers this year. However, it is too early in the year to draw conclusions. There are reported to be at least 15 buyout firms each aiming to raise USD 15bn or more in 2022.

Figure 1: Fundraising

Source: Preqin, April 2022.

Despite the differences in private equity activity across regions, we continue to apply our investment themes in a regional context in order to source the best opportunities globally for our investors. Our investment themes lead us to areas of high growth, irrespective of the macro environment.

Our investment themes lead us to areas of high growth, irrespective of the macro environment

In January, we invested in Ectivate Education, a Singapore-based education platform made up of two core companies: I Can Read, a premier regional English language provider focused on young children, and Indigo, a leading tuition provider that specializes in English for secondary to high school students. The plan is to continue to consolidate the fragmented but resilient tutoring market in Singapore. This company plays our Future of Work investment theme and has a measurable positive contribution to SDG 4 – Quality Education.

In February, we invested in Tandem, a fast growing digital bank in the UK that provides lending products with an emphasis on the green economy. Our investment, alongside Pollen Street Capital, will help fund the acquisition of Oplo, a social purpose non-bank lending business, in order to create a sizable UK purpose-led bank. Tandem plays our Personal/Financial Wellbeing investment theme.

Meanwhile, in the US on the secondaries side, we closed a single asset restructuring of Micronics, a leader in the filtration market. The company’s products are used for wet and dry industrial filtration needs where the demand is driven by environmental regulatory compliance and technological change and innovation. Our investment is being used to acquire NFM, a competitor in the filtration market, to create a market leading platform. Notably, including the synergies from the merger, the valuation of the transaction is an attractive 5.4x EBITDA. This was an off-market transaction which we sourced through one of our existing GP relationships.

In March, we committed to the first fund of bd-capital Partners, a UK-based specialist investor in the healthcare, services and consumer sectors. The firm is led by a well-seasoned team who were formally part of the Consumer European team at Advent International. This fits our typical emerging manager investment profile: (i) we have good visibility on the first few investments, with three already having closed, (ii) we have guaranteed co-investment rights, and (iii) we have been able to come in on preferred economic terms.

Overall, despite geopolitical concerns, rising inflation and turbulent stock markets, we continue to see a high level of dealflow through our global network of investment partners. This allows us to keep our bar extremely high and only invest in the most robust, attractively valued opportunities which are playing our investment themes and thus promising compelling growth.

Normalisation – Delayed or Derailed?

Our core scenario for 2022 called for normalization: economic growth cooling towards potential levels that, combined with easing supply constraints, would allow inflation to cool as well. While the former macro trend has been affirmed, the latter has been, at best, deferred or, at worst, derailed.

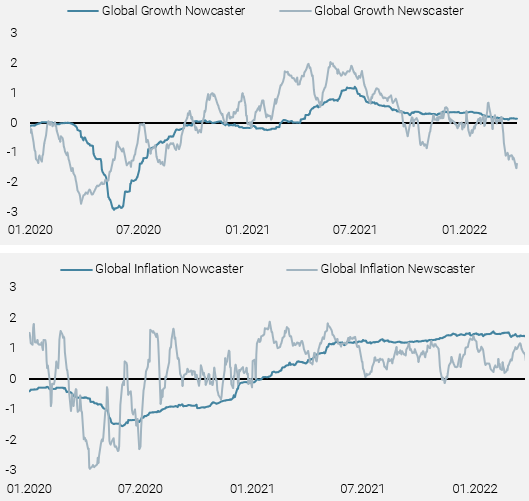

Figure 2 shows the evolution of our systematic indicators tracking global growth and inflation conditions in real-time, our Nowcasters (which assess traditional macro data) and Newscasters (which assess alternative news data on macro conditions). Growth conditions have normalized significantly, with the Global Growth Newscaster suggesting an elevated risk of recession, primarily due to reporting on the economic impact of the Russian invasion of Ukraine and tightening monetary policy.

On the other hand, both our Global Inflation Nowcaster and Newscaster point to the stability of a high inflation regime. Importantly, diffusion indices for the Nowcasters have been hovering around 50% or below since the start of the year, which suggests that these indicators will likely fall in the months ahead. However, the combination of the Russia/Ukraine conflict and additional Covid lockdowns in China have increasingly disrupted supply chains and sent various commodity prices higher, further supporting the level of our inflation indicators.

The combination of the Russia/Ukraine conflict and additional Covid lockdowns in China have disrupted supply chains and sent various commodity prices higher, fuelling inflation.

Figure 2: Growth and Inflation Indicators

Source: Bloomberg, RavenPack, Unigestion. Data as at 1 April 2022.

After an eventful start to the year, the second quarter should provide investors with greater insight into the sustainability of the current inflationary environment and the consequent reaction of monetary policy. The key question will be to what extent central banks can raise real rates to tame inflation without triggering a recession, or whether an inflationary mind-set takes hold and drives wages and inflation expectations higher, thereby keeping real yields depressed. Markets are expecting central banks like the Fed to be successful in avoiding a “hard landing”, which is a difficult task at any time, never mind during a major geopolitical crisis.

The key question will be to what extent central banks can raise real rates to tame inflation without triggering a recession.

With regard to the Fed itself, markets have priced in over nine hikes in the next twelve months and an additional hike in 2023. If the Fed meets these expectations, and recent statements indeed point to such an aggressive tightening path, they should be successful in raising real rates and fighting off inflation. However, the risk of tipping the economy into recession is substantial in such a scenario, especially in light of the significant economic slowdown already taking place.

Portfolio Stability in a Crisis

When the war broke out in Ukraine in late February, we immediately undertook an analysis of our entire portfolio to verify that we had no existing companies, either through direct investments or fund managers, with headquarters or significant operations in Russia, Ukraine or Belarus. Since our investment remit does not cover these regions, we were able to quickly confirm that we indeed did not have any direct exposure.

The next part of our analysis went deeper into the operations of our portfolio companies to understand the second order effects. For this, we analyzed over 1,200 portfolio companies, both in our direct portfolios and the portfolios of our fund managers, representing more than 75% of the aggregate NAV of our portfolios. For each company, we determined if it had: (i) any customer or supplier exposure to this region, (ii) any local operations in the region, and (iii) any material exposure to energy prices.

The results showed us that no company in our portfolio has more than 30% of its revenues or cost base exposed to the region. Meanwhile, only 13 companies out of 1,200 had between 10% and 30% of their revenues and/or cost base exposed. In these cases, the companies have quickly remedied the situation.

For example, FORM.com, a US application software company for the retail sector, had 20% of its programmers based in Ukraine prior to the conflict. Following the onset of the war, the company made sure that these programmers and their families were safely moved to neighbouring Poland. As a result, the company’s operations have not been effected.

In a second example, Deeper, a Lithuanian company offering smart sonar devices for anglers, had been selling approximately 11% of its products by value to Russian-based consumers. Following the onset of the war, the company was able to immediately halt its sales into Russia and instead increase its effort towards other high growth markets. While this temporarily dented their revenues, the growth in other markets has been able to fill in the hole.

We continue to monitor the ongoing second and higher order effects of the conflict on our portfolios, and will report to our investors as we get further relevant information.

Opportunities in Climate Impact Investing

With environmental concerns increasingly top of mind, consumer behaviour across the world is changing. Individuals embrace more sustainable living, seeking products and services that align with their personal values to do no harm to the environment. In a large-scale survey conducted by the UN Development Programme in 2021, two-thirds of the 1.2 million respondents considered climate change as an emergency and called for decision makers in the public and private sector to step up and take action.

Over the next few years, as governments, companies and consumers become fully focused on the reduction of carbon emissions, the amount of investment required to get our economies onto the path of carbon net-zero by 2050 are huge, measured not in just billions, but in trillions.

It is clear that investors who want exposure to impact investments would like to benefit from these trends. However, most investors ask two critical questions. Firstly, can I achieve impact and attractive returns at the same time? Secondly, how can I track whether real impact is being delivered?

Many investors want to achieve impact and returns, but it is not always easy to track whether real impact is being delivered.

Impact and Returns

We believe that several climate impact sectors will significantly benefit from this tailwind, leading to exciting investment opportunities. From Energy Transition and Green Mobility through to Green Construction and Decarbonization of Heavy Industry, to name just a few, the expected growth is huge. For example, an estimated USD 3.4tn needs to be invested into renewable energy in order for it to reach its targeted 55% share of the energy supply by 20303. In Europe, given the current reliance on Russian fossil fuels, the push towards renewables will only be exacerbated.

It will be nimble private, climate-focused businesses which will benefit from these tailwinds and play a leading role in the push for net-zero. For example, the electric vehicle industry is expected to grow by 36% per year until 2030, which will require USD 3tn of investment annually4. Innovative companies which provide technology, services or infrastructure for electric vehicles will clearly benefit from this growth.

At Unigestion, in the last 12 years, we have invested in multiple companies benefiting from the climate tailwind and achieved attractive returns. In Energy Transition, we invested in a Japanese solar provider, achieving a 2.9x return for our investors. In Green Construction, we invested in a business which contributes to significant energy savings through lighting fixtures, achieving an 8.0x return. Finally, in Green Mobility, we invested in a software business which reduces emissions related to logistics, achieving a 3.0x return.

Quantified Impact

The introduction of SFDR (Sustainable Financial Disclosure Regulations) in March 2021 was a big step towards the standardization of ESG integration, measurement and reporting for all EU-based financial firms (as well as international firms marketing to European investors). In addition, the Science-Based Targets initiative (SBTi) released the first guidance for private equity firms at COP 26 in November 2021. Science-based targets (SBTs) provide companies with a clearly-defined path to reduce emissions in line with the Paris Agreement goals such that carbon net-zero is achieved by 2050.

Using SBTs, companies can measure their greenhouse gas (GHG) emission intensity (calculated as annual GHG emissions in tonnes of CO2 divided by revenues in EUR m) against sector or tailor-made benchmarks. The critical point for impact managers who build portfolios of environmentally sustainable investments (as defined by SFDR Article 9) is that the GHG emission measure must include scopes 1, 2 and 3. This means that, as well as the direct emissions of a company, the relevant emissions of the suppliers and users of the company’s products/services will be included.

Consequently, using this and other related measures, managers of an Article 9 fund are able to demonstrate real impact across the portfolio, both on an absolute (entry vs. exit) and relative (vs. for example SBTs) basis.

With these clear tailwinds and transparent, objective ways to measure impact, investors can achieve the holy grail of impact investing – strong returns with quantified impact. At Unigestion, our recently launched Climate Impact programme fully captures this attractive investment opportunity, with clear impact measures and benefits from our 12 years of impact investing experience. We are excited to be at the forefront of the journey towards a low carbon economy.

Unigestion Private Equity Activity

In the first quarter of 2022, the Unigestion private equity team committed EUR 175.7m to investments, including EUR 44.3m invested in 3 secondary transactions and EUR 39.7m invested in 3 direct investments. Here are the highlights of some of the investments and exits that we completed in Q1:

In January, our latest direct programme closed an investment in Blauwtrust Groep (www.blauwtrustgroep.com) alongside Blackfin Capital Partners. Blauwtrust Groep is based in the Netherlands and active across the mortgage value chain. Founded in 1985, the company has progressively expanded its service offering to include mortgage distribution, servicing and origination. It employs 750 FTEs and, in 2021, generated around EUR 125m in revenue and EUR 38m in EBITDA. The Dutch mortgage market is one of the largest in Europe (on a relative basis) and one where traditional banks have been unable to cover the entire market. The housing shortage has driven an increase in house prices (+8% per annum between 2016 and 2020) and this trend is expected to continue in the coming years. The continued disintermediation of the value chain by ‘alternative’ parties along every step is providing a significant tailwind for the company’s future growth.

In January, our latest direct programme closed an investment in Blauwtrust Groep (www.blauwtrustgroep.com) alongside Blackfin Capital Partners. Blauwtrust Groep is based in the Netherlands and active across the mortgage value chain. Founded in 1985, the company has progressively expanded its service offering to include mortgage distribution, servicing and origination. It employs 750 FTEs and, in 2021, generated around EUR 125m in revenue and EUR 38m in EBITDA. The Dutch mortgage market is one of the largest in Europe (on a relative basis) and one where traditional banks have been unable to cover the entire market. The housing shortage has driven an increase in house prices (+8% per annum between 2016 and 2020) and this trend is expected to continue in the coming years. The continued disintermediation of the value chain by ‘alternative’ parties along every step is providing a significant tailwind for the company’s future growth.

In the same month, Unigestion closed an investment in Yaneng Biosciences (www.yanengbio.com) with CBC Group, a leading healthcare-focused buyout/growth firm in China. Yaneng Biosciences is a leading molecular diagnostics company engaged in the R&D, manufacturing and sales of HPV tests for cervical cancer screening, thalassemia genetic tests and other diagnostics-related products and services. The company is China’s market leader in HPV and thalassemia testing and, in 2020, generated USD 88m in net revenues and USD 38m in EBITDA. Growing at 20%+ CAGR, molecular diagnostics is the fastest growing segment in China’s in-vitro diagnostics (“IVD”) industry, while HPV testing for cervical cancer, thalassemia genetic testing and hereditary deafness testing are the largest categories in the women and children’s health market. HPV testing is still underpenetrated in China which provides potential upside to the company’s growth, driven by increasing adoption.

In the same month, Unigestion closed an investment in Yaneng Biosciences (www.yanengbio.com) with CBC Group, a leading healthcare-focused buyout/growth firm in China. Yaneng Biosciences is a leading molecular diagnostics company engaged in the R&D, manufacturing and sales of HPV tests for cervical cancer screening, thalassemia genetic tests and other diagnostics-related products and services. The company is China’s market leader in HPV and thalassemia testing and, in 2020, generated USD 88m in net revenues and USD 38m in EBITDA. Growing at 20%+ CAGR, molecular diagnostics is the fastest growing segment in China’s in-vitro diagnostics (“IVD”) industry, while HPV testing for cervical cancer, thalassemia genetic testing and hereditary deafness testing are the largest categories in the women and children’s health market. HPV testing is still underpenetrated in China which provides potential upside to the company’s growth, driven by increasing adoption.

In February, we invested in Quadriga VI. Quadriga Capital, based in Frankfurt, has 25 years of investment experience in the DACH region, making it one of the pioneers in private equity investments in medium-sized companies in Germany, Austria and Switzerland. Quadriga focuses on three sectors: healthcare, technology-based services and so-called „smart“ industries. The team has investment specialists with in-depth industry knowledge and networks in these sectors and their sub-sectors. In addition, Quadriga has an extensive network of operational consultants and industry experts to help optimize the sourcing and value creation processes of target companies. Since 1995, it has invested an aggregate amount of EUR 1.6 billion in 43 platform and 108 bolt-on acquisitions.

In February, we invested in Quadriga VI. Quadriga Capital, based in Frankfurt, has 25 years of investment experience in the DACH region, making it one of the pioneers in private equity investments in medium-sized companies in Germany, Austria and Switzerland. Quadriga focuses on three sectors: healthcare, technology-based services and so-called „smart“ industries. The team has investment specialists with in-depth industry knowledge and networks in these sectors and their sub-sectors. In addition, Quadriga has an extensive network of operational consultants and industry experts to help optimize the sourcing and value creation processes of target companies. Since 1995, it has invested an aggregate amount of EUR 1.6 billion in 43 platform and 108 bolt-on acquisitions.

In the same month, we also closed an investment in GBA Group (www.gba-group.com), a specialist in bioanalytical laboratory services („TIC“ – Testing, Inspection and Certification). The company, which is headquartered in Hamburg and employs over 1,300 people, is active in Germany, Austria, Belgium and Poland. Through strong buy and build activity, it has continued to expand its geographic footprint. The company provides testing services in the most attractive and resilient TIC areas: the food and beverage industry (2021 revenue share of 36%), the pharmaceutical industry (31%), and environmental analysis (33%). High growth and an expansive acquisition strategy have enabled GBA Group to establish a leading position in these subsectors. Having made 16 acquisitions in Germany and other European countries since 2014, the company plans to continue this strong growth under our ownership.

In the same month, we also closed an investment in GBA Group (www.gba-group.com), a specialist in bioanalytical laboratory services („TIC“ – Testing, Inspection and Certification). The company, which is headquartered in Hamburg and employs over 1,300 people, is active in Germany, Austria, Belgium and Poland. Through strong buy and build activity, it has continued to expand its geographic footprint. The company provides testing services in the most attractive and resilient TIC areas: the food and beverage industry (2021 revenue share of 36%), the pharmaceutical industry (31%), and environmental analysis (33%). High growth and an expansive acquisition strategy have enabled GBA Group to establish a leading position in these subsectors. Having made 16 acquisitions in Germany and other European countries since 2014, the company plans to continue this strong growth under our ownership.

Also in February, Resource Partners II, a Polish fund in our primary programme and a mandate account, exited Maced (www.maced.pl), generating gross proceeds of EUR 7.0m. Maced has two production plants (Polanów and Gardno) and is the biggest manufacturer of dog treats in Poland and one of the biggest in Europe. Initially, most of its products were exported to Western European countries. Today, the company serves the largest retailers and distributors in the EU, as well as the majority of pet shops in Poland. The transaction resulted in a gross TVPI of 2.8x and 78% gross IRR.

Also in February, Resource Partners II, a Polish fund in our primary programme and a mandate account, exited Maced (www.maced.pl), generating gross proceeds of EUR 7.0m. Maced has two production plants (Polanów and Gardno) and is the biggest manufacturer of dog treats in Poland and one of the biggest in Europe. Initially, most of its products were exported to Western European countries. Today, the company serves the largest retailers and distributors in the EU, as well as the majority of pet shops in Poland. The transaction resulted in a gross TVPI of 2.8x and 78% gross IRR.

In February, our latest secondary programme closed an investment in a single asset continuation vehicle for US Fertility (www.usfertility.com), sponsored by Amulet Capital Partners. US Fertility is the largest network of fertility clinics in the country, offering a full suite of services including traditional fertility treatments, IVF, genetic testing and egg freezing. The US fertility market remains highly fragmented with the five largest players capturing less than 20% of market share. US Fertility benefits from attractive macro trends, a differentiated physician partnership model, and an accretive pipeline of M&A and ancillary product growth.

In February, our latest secondary programme closed an investment in a single asset continuation vehicle for US Fertility (www.usfertility.com), sponsored by Amulet Capital Partners. US Fertility is the largest network of fertility clinics in the country, offering a full suite of services including traditional fertility treatments, IVF, genetic testing and egg freezing. The US fertility market remains highly fragmented with the five largest players capturing less than 20% of market share. US Fertility benefits from attractive macro trends, a differentiated physician partnership model, and an accretive pipeline of M&A and ancillary product growth.

In March, Next Capital signed an agreement to sell NZ Bus (www.nzbus.co.nz), New Zealand’s largest urban public transport business and operator of metropolitan bus services. Unigestion invested alongside Next Capital in NZ Bus in August 2019. We were attracted by the favourable industry fundamentals (urbanization, population growth and support for public transport) and the company’s well-invested asset base and strategic portfolio of depots. But above all, we backed the impressive leadership team and Next Capital’s experience in the bus sector – NZ Bus is Next Capital’s third bus deal – to deliver on an ambitious operational improvement plan which has included the electrification of a large portion of the fleet. As a result, EBITDA grew from NZD 18m at the time of acquisition to NZD 55m on exit. The transaction is expected to result in a gross TVPI of 4.2x and 65% gross IRR.

In March, Next Capital signed an agreement to sell NZ Bus (www.nzbus.co.nz), New Zealand’s largest urban public transport business and operator of metropolitan bus services. Unigestion invested alongside Next Capital in NZ Bus in August 2019. We were attracted by the favourable industry fundamentals (urbanization, population growth and support for public transport) and the company’s well-invested asset base and strategic portfolio of depots. But above all, we backed the impressive leadership team and Next Capital’s experience in the bus sector – NZ Bus is Next Capital’s third bus deal – to deliver on an ambitious operational improvement plan which has included the electrification of a large portion of the fleet. As a result, EBITDA grew from NZD 18m at the time of acquisition to NZD 55m on exit. The transaction is expected to result in a gross TVPI of 4.2x and 65% gross IRR.

1Pitchbook, April 2022

2Preqin, April 2022.

3Frost & Sullivan Report Growth Opportunities from Decarbonization in the Global Power Market.

4IEA Sustainable Development Scenario.

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

To the extent that this report contains statements about the future, such statements are forward looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modelling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Additional Information for U.S. Investors

For US investors, Unigestion is relying on SEC Rule 15a-6 under the Securities Exchange Act of 1934 regarding exemptions from broker-dealer registration for foreign broker dealers. Foreside Global Services, LLC is acting as the chaperoning broker dealer for Unigestion for the purposes of soliciting and effecting transactions with or for U.S. institutional investors or major U.S. institutional investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss. The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

This material is approved and disseminated by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority („FCA“) and registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients. This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority („FCA“). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the United States by Unigestion (UK) Ltd., which is registered as an investment adviser with the United States Securities and Exchange Commission (“SEC”). All inquiries from investors present in the United States should be directed to clients@unigestion.com at Unigestion (UK) Ltd. This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” („AMF“).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission („OSC“). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority („FINMA“).

Document issued May 2022.