SHOULD WE WORRY ABOUT BONDS CARRY WHEN THE FED CUTS RATES?

- Bonds carry has been one of the best-performing alternative risk premia strategies in recent years.

- While the strategy has historically performed well when the Fed has cut rates, the current situation is unusual as bonds carry in the US is much lower than in other G8 countries.

- Nonetheless, the strategy’s allocation, by design, will continue to adapt to changes in implied carry and we expect further robust returns in the future.

Overview

In light of rising trade war risks and a marked slowdown in the global economy that has pushed inflation risks lower, major central banks have shifted recently from “normalisation mode” to “easing financial conditions” in order to avoid recession. As a result, global bond yields have declined significantly. In this new market environment, what can we expect from a bonds carry strategy, which aims to deliver positive returns in various economic regimes by being long sovereign bonds that offer high carry and short those offering low carry?

Bonds Carry: One of the Best-Performing ARP in the Recent Past

Alternative risk premia (ARP) solutions aim to deliver high risk-adjusted returns with a low correlation to traditional assets such as equities, sovereign bonds and commodities. To achieve that objective, we have identified a spectrum of individual ARP which make economic sense for why they should reward the investor, have been historically proven to produce positive long-term returns, and are liquid and easy to implement. In that framework, our investment universe consists of three types of ARP: Equity Factors, Macro Directional strategies, and Alternative Income/Carry strategies.

The bonds carry strategy we illustrate in this paper takes long positions in bonds with above-median carry and short ones in those with below-median carry in a duration-neutral manner. It aims to capture the carry premium within the G8 universe (excluding Japan and Italy). While the strategy is constructed to be duration neutral, it can still be exposed to shifting

and/or diverging expectations on central bank monetary policies.

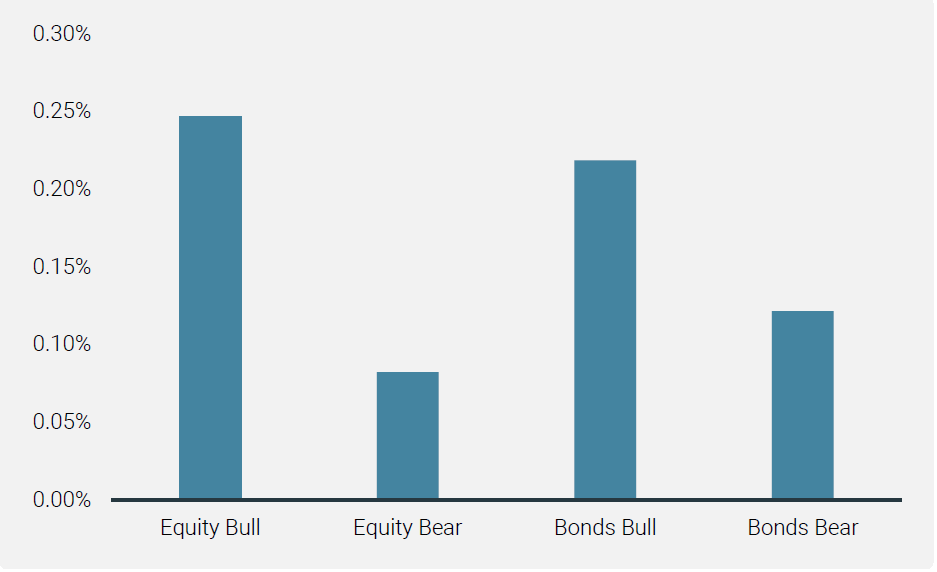

Since the launch of our ARP strategies, first within our flagship multi asset fund, then as a standalone fund, bonds carry has delivered impressive absolute returns across all market environments – equity bull, equity bear, bonds bull and bonds bear markets (Chart 1).

Chart 1: Bonds Carry in Different Market Conditions (Average Weekly Bonds Carry Performance)

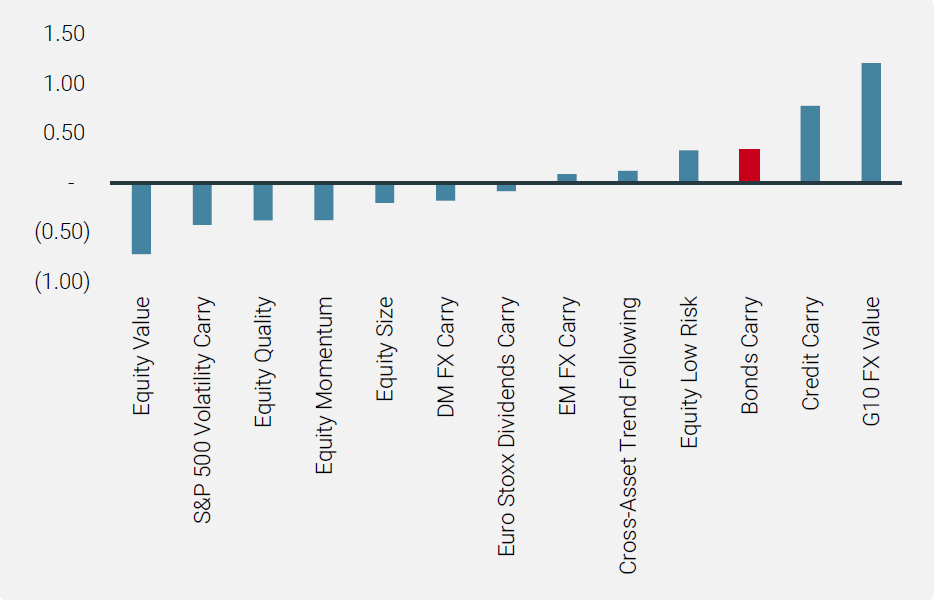

Bonds carry has also been one of the best performers across individual ARP on a risk-adjusted basis (Chart 2).

Chart 2: Risk-Adjusted Returns of Individual ARP Since Strategy Launch

Bonds Carry: The Slope Matters, Not Just the Bond Yield

Carry, the return earned should prices not change, is defined following Koijen et al (2016). For bonds, carry consists of two effects: (i) the bond’s yield spread relative to the risk-free rate plus (ii) the “roll-down”, which captures price changes as the bond rolls down the yield curve. It is important to note that the carry of a bond is not simply determined by the level of its yield, but also by its “roll-down”.

To illustrate the effect of a “roll-down”, consider a normal upward-sloping yield curve. As a five-year bond becomes a four-year bond after one year, the decrease in yield will naturally lead to a gain in the bond’s price, assuming that the level and shape of the yield curve remains unchanged. For a normal upward-sloping yield curve, the steeper the yield curve, the higher the “roll-down”.

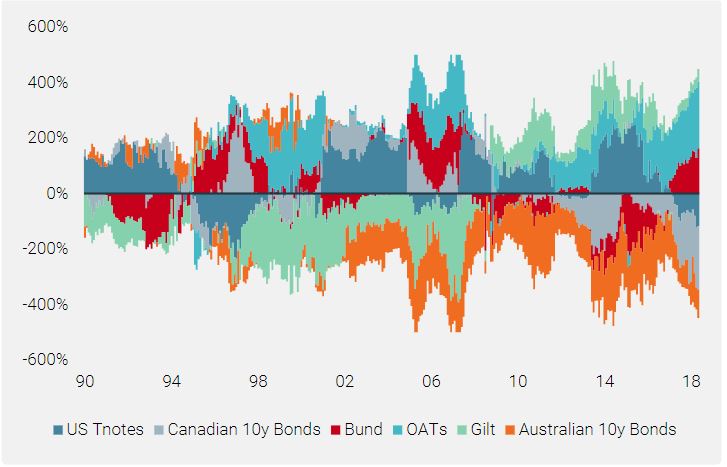

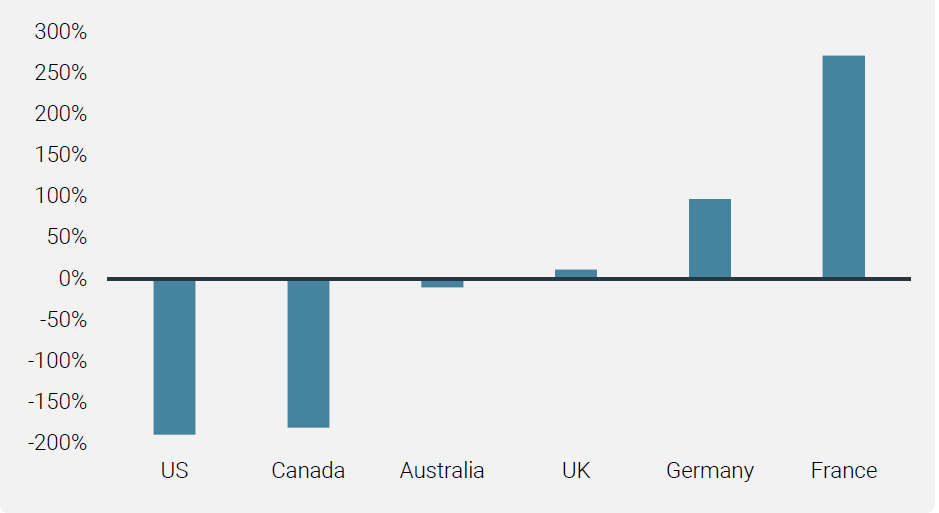

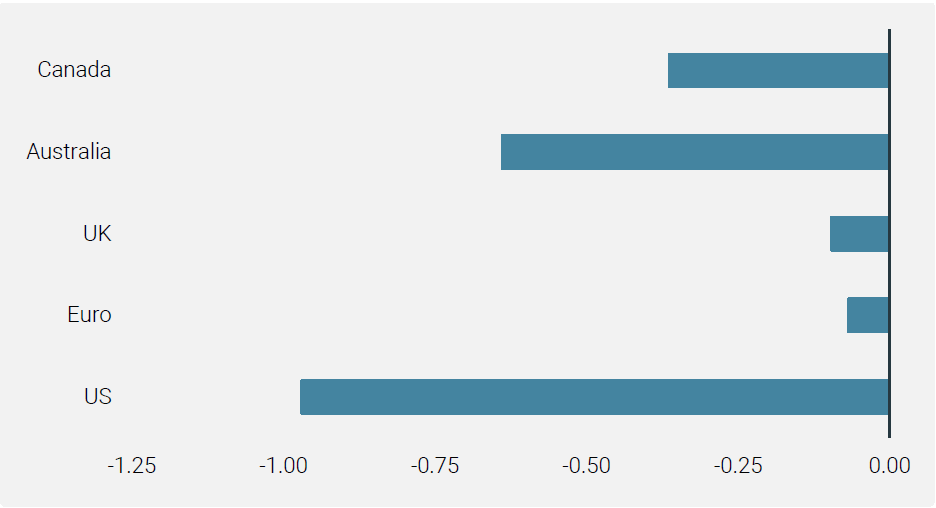

Historically, from 1990, this strategy was long US bonds due to a steeper US curve on average (Chart 3). However, as the US curve has flattened due to the Fed’s normalisation since 2015, despite European bonds offering negative or very low yields, the strategy has been long European bonds and short North American bonds since 2017. Currently, given the flat curves in the US, Canada and Australia, the positioning continues to be long European bonds and short North American and Australian bonds (Chart 4).

The carry of a bond is not simply determined by the level of its yield, but also by its “roll-down”

Chart 3: Historical Bonds Carry Strategy Capital Allocation

Chart 4: Bonds Carry Strategy Capital Allocation as at 25.06.2019 (for a Strategy with a 10% Volatility Target)

As markets expect monetary easing across most main developed markets in the coming years, and more so in the US than anywhere else (Chart 5), is this positioning at risk?

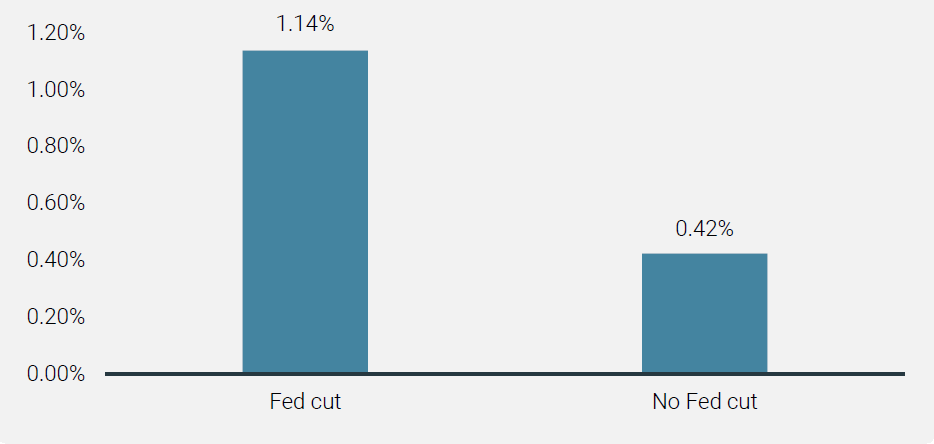

During the months where the Fed cut rates, bonds carry delivered positive and higher returns on average than periods without rate cuts.

Chart 5: Monetary Policy Market Expectations (12-month Expected Changes in Central Bank Rates, in Basis Points)

Historically, Fed Cuts Have Been Favorable for Bonds Carry

Since 1990, there have been five Fed easing cycles (1990/1992, 1995/1996, 1998, 2001/2003 and 2007/2008). As shown in Chart 6, during the months where the Fed cut rates, bonds carry delivered positive and higher returns on average than periods without rate cuts, and the spread in absolute performance is large. Furthermore, the proportion of positive monthly returns during periods of rate cuts is also higher (71%) than that during periods with no cuts (61%).

Chart 6: Average Monthly Performance of Bonds Carry Since 1990 by Fed Monetary Action

At first glance, based on its historical return behaviour, one may draw the conclusion that we need not be overly concerned about the future returns of the strategy.

Does It Work Even If Recession Is Not on the Horizon?

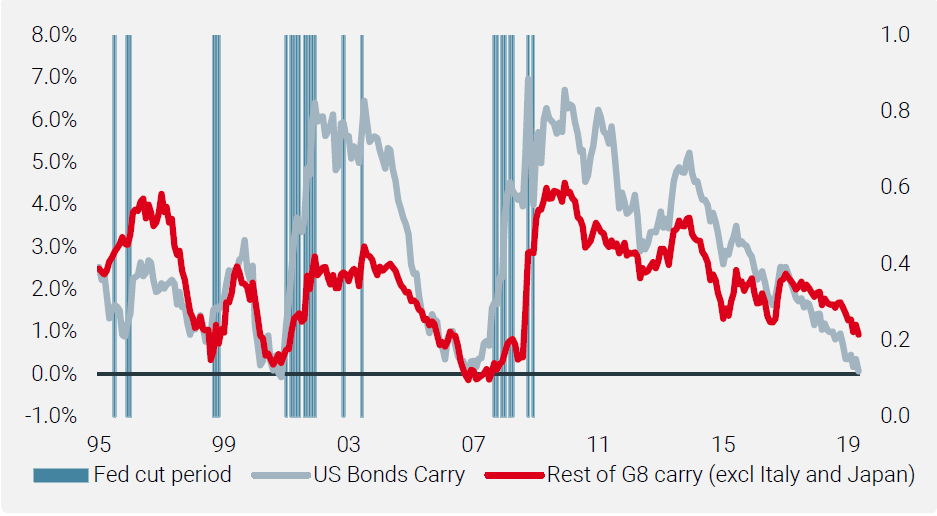

However, the current situation is unusual. The Fed has been more aggressive in its normalisation than other central banks. As a result, the yield curve in the US is flatter than in most other countries. This is illustrated in Chart 7, which compares the carry provided by the US versus the rest of G8 bonds (excluding Italy and Japan, as they are not in the strategy’s investment universe). Chart 7 shows that the current US bonds carry is much lower than the rest of the G8 countries, which is rare historically. In the past, there was only one occurrence similar to the current situation during periods of Fed cuts, particularly when recession risk is not high: 1995/1996. As a result, it was also the only historical Fed cut period where the strategy was also short US bonds (and short Canadian bonds for the first half of that period), as is the strategy’s position today (Chart 8).

The current US bonds carry is much lower than the rest of the G8 countries, which is rare historically

Chart 7: US Bonds Carry vs the Rest of G8 Bonds Carry

Chart 8: Average Historical Allocation of the Strategy During Periods where the Fed Cut Rates

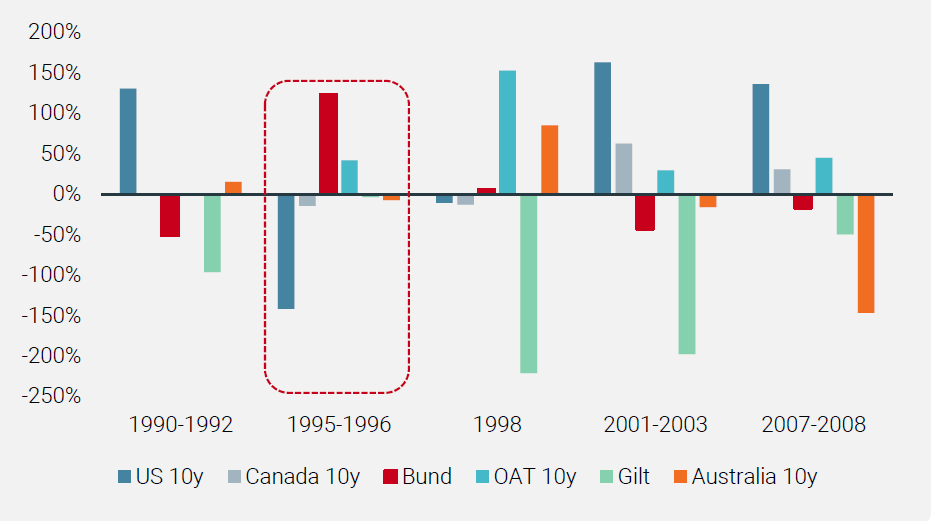

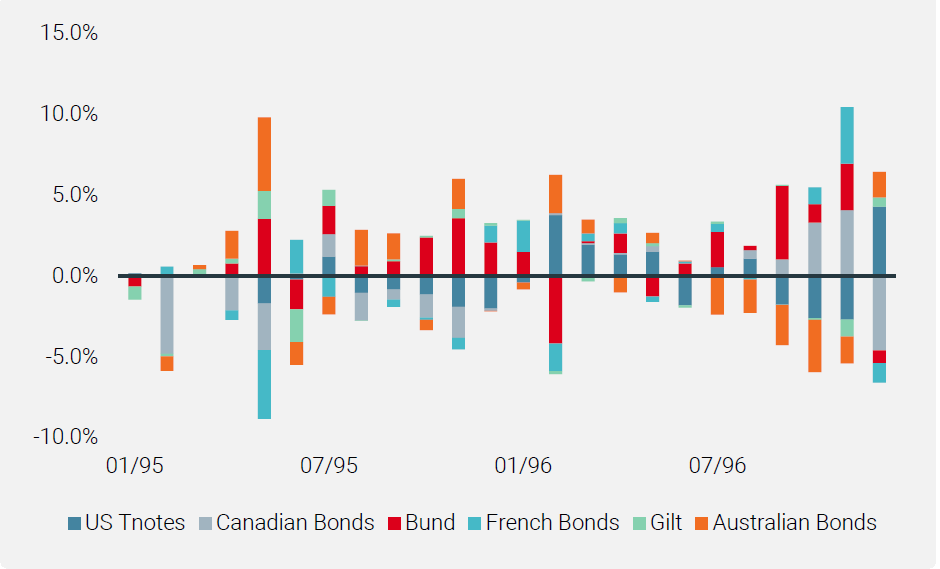

How did the strategy perform during this period, which was similar to today? During the first six months of 1995, ahead of Fed rate cuts, the strategy lost money (-8.5%), as it did in April and May of 2019. As shown in Chart 9, which presents performance contributions over the 1995/1996 period, the short position in US bonds was costly.

Chart 9: Performance Contributions During 1995/1996

However, the bulk of the negative contribution came from the short exposure to Canadian bonds, as the Bank of Canada had been aggressively easing during this period. Nevertheless, thanks to global easing from most of the G8 central banks, most sovereign curves steepened in 1995 and 1996, pushing the carry of the bond strategy much higher. In addition to the positive impact of yield changes, this increase in implied carry helped the strategy to recover sharply in the second half of 1995 (+5.2%) and in 1996 (+14.6%). Where short positions hurt performance as their respective central banks undertook substantial rate cuts, this was mostly offset by long positions posting large positive contributions.

Finally, it is worth highlighting that the strategy’s allocations change with each sovereign bond’s carry, which in turn is determined by the slopes of their respective yield curves. As an illustration, following significant monetary easing in Canada, the Canadian curve had steepened, increasing Canadian bonds’ carry. As a result, the strategy shifted from a short to a long position in Canadian bonds, which contributed positively to the performance in 1996, as shown in Chart 9.

This Time It’s Different?

We believe that history could repeat itself, protecting the strategy against a deep and prolonged drawdown arising from its large short position in US bonds. However, there is one important difference to note. Contrary to the current situation, US rates were lower than most other G8 countries back in 1995. Before the June 1995 Fed cut, US Fed fund rates were at 6% vs 6.6% for the UK, 8% for Canada, and 7.5% for Australia. Only German rates were lower at 4.85%, and even then, this is still much more elevated than G8 rates today. This means that every G8 central bank had room to carry out monetary easing, which led the strategy to benefit from an increase in implied carry (through the steepening of the curve), while losses from rate cuts on the short positions were largely offset by gains on the long positions. Today, the situation is very different as most non-US short-term rates are still low, even negative in some cases. As a result, the potential cushion delivered by curve steepening through global monetary easing and the gains on the long positions through yield cuts could be more limited this time. However, by design, the strategy’s allocation will adapt to the changes in implied carry, as it has done in the past. We believe that this should lead the strategy to continue to provide the robust returns it has done over recent decades.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Backtested or simulated performance: Backtested or simulated performance is not an indicator of future actual results. The results reflect performance of a strategy not currently offered to any investor and do not represent returns that any investor actually attained. Backtested results are calculated by the retroactive application of a model constructed on the basis of historical data and based on assumptions integral to the model which may or may not be testable and are subject to losses.

Changes in these assumptions may have a material impact on the backtested returns presented. Certain assumptions have been made for modeling purposes and are unlikely to be realized. No representations and warranties are made as to the reasonableness of the assumptions. This information is provided for illustrative purposes only. Backtested performance is developed with the benefit of hindsight and has inherent limitations. Specifically, backtested results do not reflect actual trading or the effect of material economic and market factors on the decision-making process. Since trades have not actually been executed, results may have under-or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity, and may not reflect the impact that certain economic or market factors may have had on the decision-making process. Further, backtesting allows the security selection methodology to be adjusted until past returns are maximized. Actual performance may differ significantly from backtested performance.

Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA). It is also registered with the Securities and Exchange Commission (SEC). Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion Asset Management (France) S.A. is authorised and regulated by the French Autorité des Marchés Financiers (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is regulated in Canada by the securities regulatory authorities in Ontario, Quebec, Alberta, Manitoba, Saskatchewan, Nova Scotia, New Brunswick and British Columbia. Its principal regulator is the Ontario Securities Commission. Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore.

Document issued July 2019.

Lesen Sie mehr

Lesen Sie mehr