MiViews Q4 2019: Einigen Wir Uns Darauf, Uneins Zu Sein

- Das makroökonomische Umfeld ist nicht so schlecht, wie viele denken. Wir erwarten keine globale Rezession in den nächsten sechs Monaten und stimmen daher nicht mit den Rezessionssignalen der invertierten Zinskurven überein.

- Dank der schwachen Inflation werden die Notenbanken zunehmend auf der Seite der Anleger agieren. Wir sehen dies als positiv für Carry-bezogene Anlagen.

- Unseres Erachtens ist die Stimmung allzu pessimistisch. Die Anleger sind unter investiert und übermäßig abgesichert. Sollte sich die Makro-Situation verbessern, besteht das Risiko einer schnellen Trendwende, da Anleihen derzeit sehr teuer sind.

Überblick

Wir allokieren Risiken dynamisch, indem wir die drei Schlüsselfaktoren überwachen, die mittelfristig die Anlageerträge beeinflussen: 1) makroökonomische Faktoren (Konjunktur und Inflation), 2) Marktstimmung und 3) Bewertung. In jüngster Zeit spiegelten die Märkte die Sorgen auf der Makroseite wider: Viele Zinskurven sind flach oder invertiert, ein traditionelles Zeichen dafür, dass eine Rezession bevorsteht. Unsere Makroindikatoren widersprechen dieser Einschätzung und zeigen, dass die Welt entsprechend ihres Potenzials wächst. Die Inflation ist unserer Meinung nach das größte Problem bei der Anpassung der Portfolios an das aktuelle Umfeld. Es gibt keinen Inflationsdruck, was viele Zentralbanken verwirrt. Wir erwarten, dass sie noch einige Zeit unterstützend wirken, was wiederum die Attraktivität von Credits und Aktien erhöhen dürfte. Die Marktstimmung zeigt deutliche Anzeichen von Pessimismus, sowohl bei der Allokation als auch bei der Nachfrage nach Hedging-Instrumenten. Schließlich sehen wir bei Anleihen größere Bewertungsrisiken als bei Aktien oder Credits. Kurz gesagt, stimmen wir dem breiten Marktpessimismus nicht zu und erwarten für das kommende Quartal einen Stimmungsumschwung.

Globales Rezessionsrisiko Begrenzt, Inflation Gering

Anleger sind angesichts verschiedener Indikatoren, die insgesamt immer mehr auf eine weitere konjunkturelle Verlangsamung hinweisen, über die Makrolage besorgt. Vor 12 Monaten, als die Wachstumsbedingungen stark waren, hätte eine Verlangsamung nur zu einem begrenzten Anstieg des Rezessionsrisikos geführt. Heute ist die Situation hingegen ganz anders, da sich das Konjunkturumfeld eindeutig verschlechtert hat.

Im gesamten Spektrum der Makrodaten treten besorgniserregende Signale auf, wobei die meisten von der industriellen Seite der Wirtschaft kommen:

- So fiel der ISM-Index für das verarbeitende Gewerbe in den USA von seinem Hoch von 60,8 im August 2018 auf 47,8 im September 2019. Eine ähnliche Verschlechterung trat 2015-2016 ein, obwohl eine Rezession nicht folgte. Der Auftragseingang, die zukunftsweisendste Komponente dieser Einkaufsmanager-Umfrage, erreichte kürzlich die Tiefststände von 2015 und zeigte ein besonders düsteres Bild.

- Die US-Kapazitätsauslastung erreichte im Oktober 2018 ihren Höhepunkt, ist seither aber fast kontinuierlich gesunken, was die Fed als weiteres Anzeichen für eine sich verschlechternde Makrolage in den USA sicherlich zur Kenntnis genommen hat.

- In Deutschland setzt die IFO-Umfrage, ein Frühindikator der deutschen Konjunktur, die deutsche Wirtschaft bereits in eine Rezession, wobei der Rückgang des BIP im zweiten Quartal anhalten dürfte.

- Die Umfrage der Europäischen Kommission kommt zu einem ähnlichen Ergebnis für Finnland, das neben Belgien und Schweden ebenfalls in eine Rezession geraten dürfte. Die gleiche Umfrage stuft auch das Vereinigte Königreich in eine schwierige Situation ein.

- Ähnliche Anzeichen gibt es auch in den Schwellenländern. Das Wachstum der chinesischen Stromerzeugung liegt in der Nähe des Niveaus von 2015. Das BIP Südafrikas ist in drei der letzten sechs Quartale negativ, mit einem starken Rückgang von -3,2% im ersten Quartal. Der Welthandelsindex CPB ging in einem Jahr um 3 % zurück. Schließlich erwarten Analysten in diesem Jahr einen Rückgang der Gewinne in den Schwellenländern.

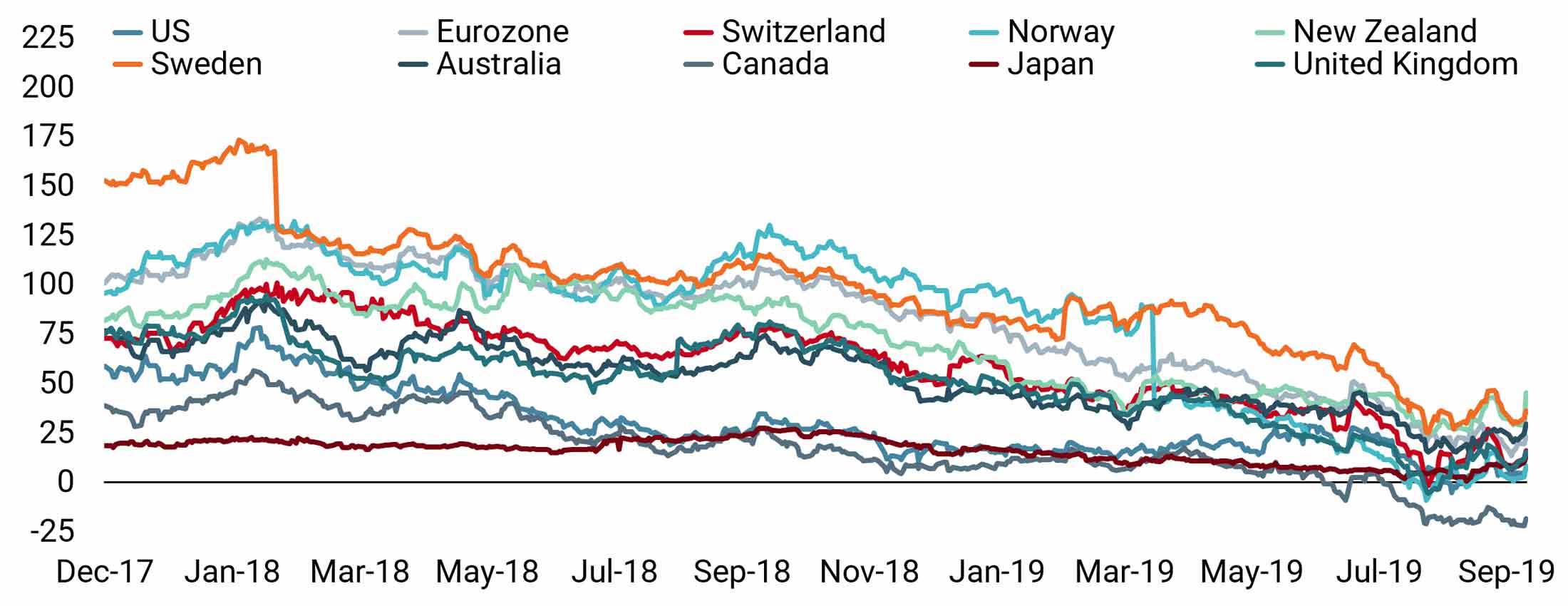

Vor diesem Hintergrund erwarten Investoren in den kommenden Monaten eine Rezession, die durch die aktuelle Form der Zinskurven der Staatsanleihen deutlich wird. In vielen Industrieländern sind die Zinskurven inzwischen flach bis invertiert. Abbildung 1 verdeutlicht diesen Umstand: Die Zinssätze der meisten G10-Staatsanleihen nähern sich dem Niveau der japanischen Kurve an, das schon lange andauert. Die aus der US-Zinskurve abgeleitete Rezessionswahrscheinlichkeit der New York Fed liegt derzeit bei 37%, gegenüber 31% im August. Dies ist beträchtlich, und das Risiko steigt.

Abbildung 1: Zinskurvenneigungen (10 Jahre minus 2 Jahre) in den G10-Ländern

Es scheint kein Entrinnen zu geben. Die Anzeichen sind klar und eine Weltrezession steht vor der Tür. Ist dies aber wirklich der Fall?

Betrachtet man ein breiteres Spektrum an Daten, kommen wir zu einem ganz anderen Schluss. Unsere selbst entwickelten Wachstums-Nowcaster sind Konjunkturindikatoren, die täglich das Rezessionsrisiko verfolgen. Diese Indikatoren decken ein breites Spektrum wirtschaftlicher Aspekte ab, darunter Konsum, Investitionen, Produktionserwartungen, Wohnungsbau und Außenhandel für 90% des weltweiten BIP. Ziel ist die Nutzung dessen, was wir über Rezessionen am besten wissen: Sie beeinflussen ein breites Spektrum wirtschaftlicher Dimensionen innerhalb und über eine große Anzahl von Volkswirtschaften hinweg. Diese werden seit Ende des Zweiten Weltkriegs erfasst, und unsere Indikatoren wurden entsprechend konzipiert, um genau diese Erkenntnis zu nutzen.

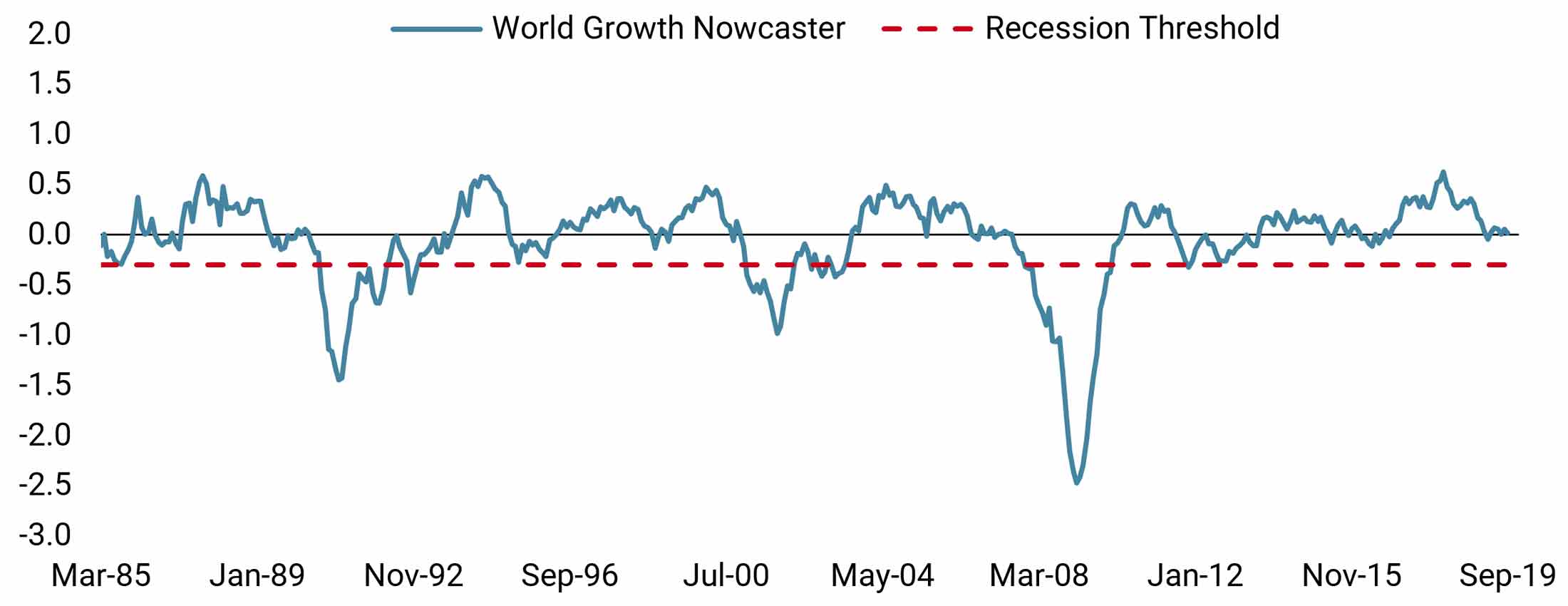

Was sagen uns die Nowcasters? Wie bereits in einem früheren Beitrag1 beschrieben und in Abbildung 2 deutlich dargestellt, bewegt sich unser World Growth Nowcaster derzeit um die Nulllinie. Dies deutet darauf hin, dass die Weltwirtschaft derzeit ihrem Potenzial entsprechend, d. h. ihrer natürlichen Wachstumsrate, von – laut IWF – rund 3,5 % wächst.

Abbildung 2: Weltwachstums Nowcaster gegenüber der Rezessionsschwelle

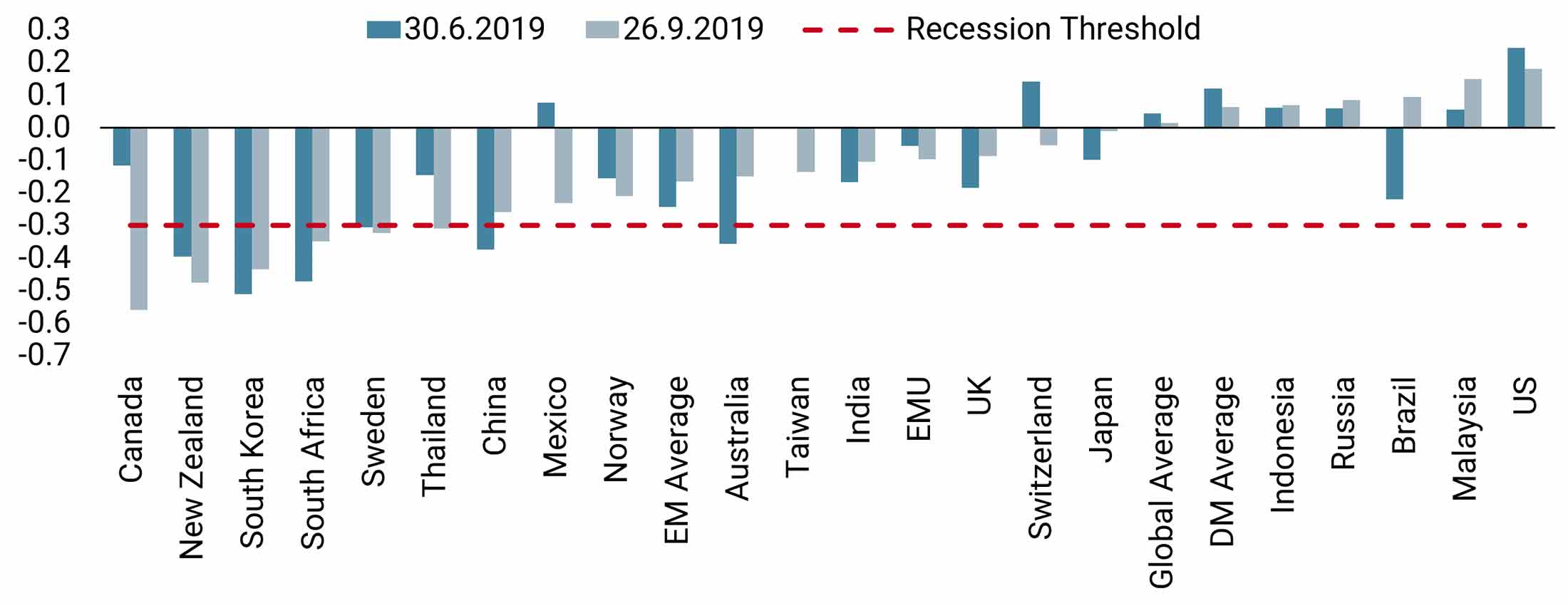

Wir können aus Abbildung 2 schließen, dass die Welt noch weit von der Rezessionsschwelle entfernt ist, was vor allem auf die starke US-Wirtschaft zurückzuführen ist. Im zweiten Quartal lag das BIP der Vereinigten Staaten mit 2% leicht über seinem potenziellen Wachstum. Das Problem ist jedoch, dass viele Länder schlechter abschneiden als die USA. Abbildung 3 zeigt, dass die Wirtschaftsbedingungen derzeit uneinheitlich sind. Die schwächsten Länder sind laut unseren regionalen Wachstums-Nowcasters Kanada, Neuseeland, Südkorea, Südafrika, Schweden und Thailand. In den anderen Volkswirtschaften scheint die Situation akzeptabel zu sein, da die jeweiligen regionalen Wachstums-Nowcaster-Niveaus bei etwa Null liegen. Darüber hinaus sind im Vergleich zum vergangenen Quartal einige Anzeichen einer Verbesserung der makroökonomischen Rahmenbedingungen erkennbar. In den Schwellenländern hat sich die Situation in Indien, Indonesien, Brasilien und Russland leicht verbessert.

Abbildung 3: Regionale Wachstums-Nowcaster

Wir sehen derzeit drei Gründe für eine konjunkturelle Verbesserung:

- Die Welthandelsindizes sind seit Beginn des Handelskrieges stark gefallen, aber viele haben sich inzwischen stabilisiert, wenn nicht sogar erholt. So stieg beispielsweise der Baltic Dry Index zuletzt um 200%, ein positives Zeichen für langsam wachsende Schwellenländer, deren Wachstumsaussichten davon abhängen.

- Der größte Teil der Verschlechterung, die wir bei unseren Indikatoren beobachten, betrifft die Umfragen zu den Produktionserwartungen, die eine starke Anfälligkeit für die Handelskriegsrhetorik zeigen. Sollte sich diese Situation verbessern, würden sich die Daten aus vielen dieser Umfragen wieder verstärken.

- Drittens scheint sich sowohl die EZB als auch die People’s Bank of China (PBoC) des zunehmenden Risikos einer Abschwächung bewusst zu sein. So hat die EZB unlängst einen neuen QE-Plan aufgelegt, die PBoC hat ihren Mindestreservesatz gesenkt, während die Regierung Chinas weiterhin Konjunkturanreize durchführt. Beide Wirtschaftsräume dürften sich im Schlussquartal 2019 einer gewissen Unterstützung erfreuen.

Niedrige Inflation heißt anhaltende geldpolitische Unterstützung

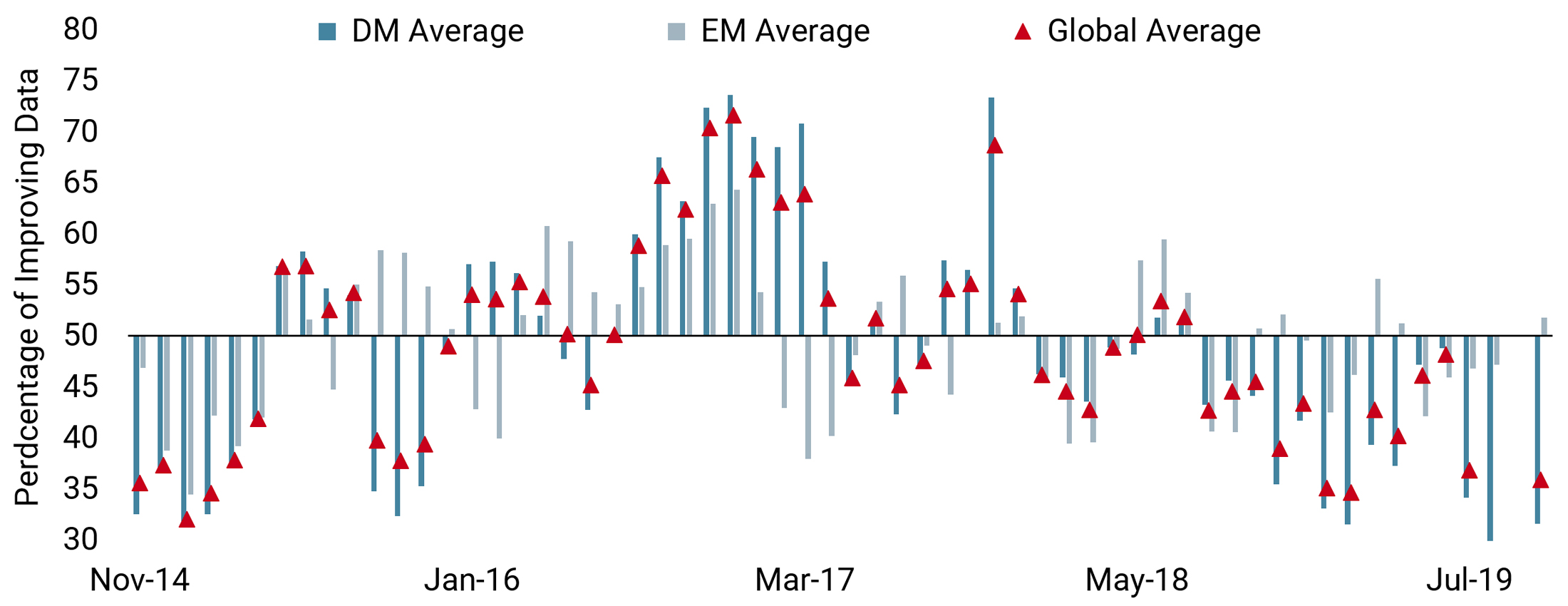

Die Inflationssituation spielt eine wesentliche Rolle in unserer aktuellen Makroeinschätzung. Wie von der EZB und unlängst von der Fed dargelegt, enttäuschten die letzten Inflationsdaten, und seit November 2018 sind die Inflationsprognosen kontinuierlich gesunken. In den USA wurden die Inflationsprognosen für 2020 von 2,3% auf 2% revidiert (Quelle: Bloomberg), während sie in der Eurozone von 1,7 % auf 1,3 % sanken. Unsere Inflations Nowcaster, die das Risiko einer Inflationsüberraschung bewerten, zeigen einen ähnlichen Trend, da sie seit dem Sommer 2018 kontinuierlich zurückgegangen sind. In jüngster Zeit hat sich dieser Trend beschleunigt, wie in Abbildung 4 dargestellt. Der Zusammenbruch unseres Indikators ist in der oberen Grafik eindeutig zu erkennen. Wenn dieser Indikator negativ ist, prognostiziert er die Gefahr einer Abwärtsüberraschung der Inflation. Die untere Grafik zeigt ein sogar noch beunruhigenderes Bild der Inflationsaussichten. Der Diffusionsindex (der Prozentsatz der sich verbesserten Daten in unserer Inflations Nowcaster) hat in letzter Zeit ein sehr niedriges Niveau erreicht. Etwa 30% aller Inflationsdaten verbessern sich, so dass 70% davon sich verschlechtern. Weltweit weisen alle Inflationsquellen nahezu in die gleiche Richtung, insbesondere in den USA. Unseres Erachtens ist dies ein Kernelement der aktuellen Makrolage: Die Inflation tritt nirgendwo auf, wodurch die Zentralbanken voraussichtlich expansiv bleiben und den Finanzmärkten willkommene Unterstützung bieten werden.

Abbildung 4: Inflations Nowcaster (links) und Diffusionsindex (rechts)

Fazit unseres Makroausblicks: Wir sehen ein geringeres Rezessionsrisiko als der Markt. Die Maßnahmen der Zentralbank sollten für die Anleger weiterhin positiv sein, da die Inflation weiterhin schwach ist. Dies sollte zu einer expansiven Geldpolitik führen, die wachstumsorientierte Vermögenswerte unterstützt.

Anleger Sind Überaus Vorsichtig

Das zweite Element unseres Ausblicks ist die Marktstimmung. Angesichts der bereits erwähnten stützenden Makro-Situation könnte man erwarten, dass sich die Marktteilnehmer positionieren, um von der Fortführung dieses anhaltenden Wachstumszyklus zu profitieren. Unsere verschiedenen Indikatoren zeigen jedoch, dass die Anleger defensiv positioniert sind.

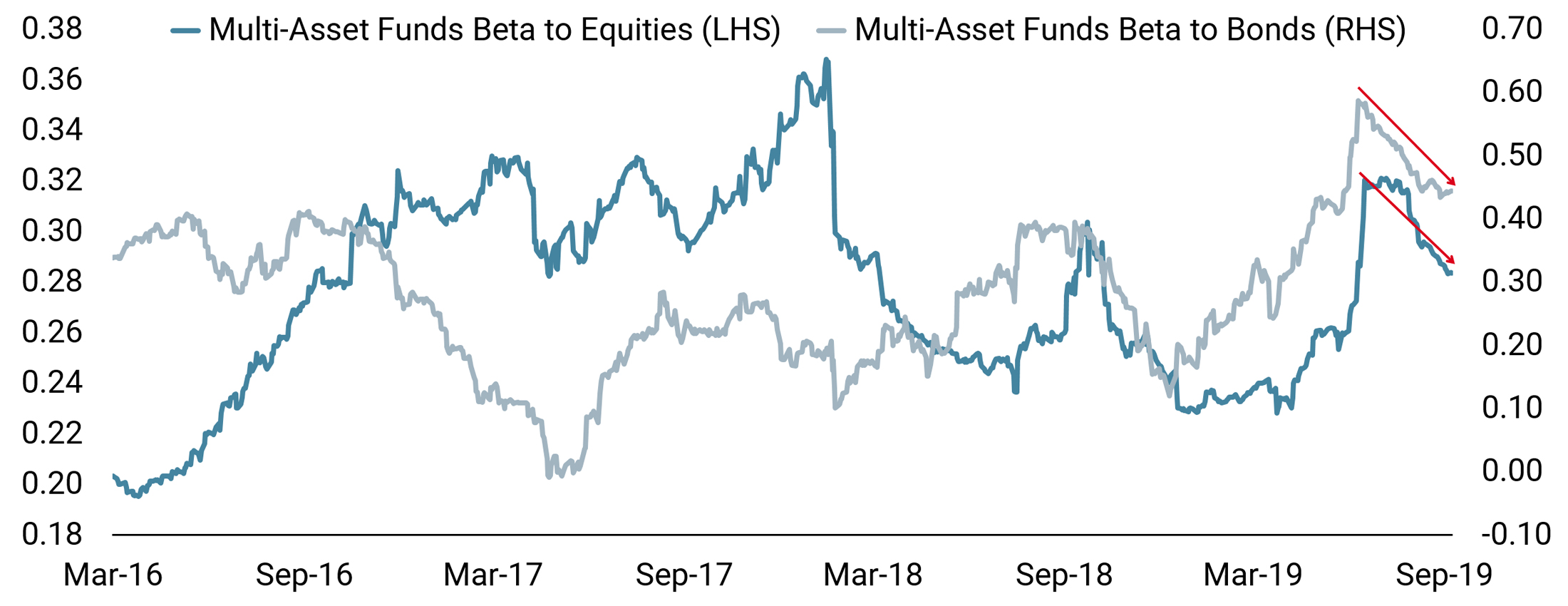

Das erkennen wir an zwei wesentlichen Elementen. Erstens, wenn man sich das historische Beta einer repräsentativen Gruppe von Multi-Asset-Fonds zu Anleihen und Aktien ansieht, erscheint ein klarer Trend. Seit Juni 2019 haben diese Fonds ihre Exposure in beiden Anlageklassen deutlich verringert. Die Situation ist ähnlich, wenn man das Beta der verschiedenen Hedge-Fonds-Strategien betrachtet, von Global Macro bis Long Short Aktien. Bedeutet dies angesichts der Entwicklung der Weltmärkte von Januar bis Juni, dass viele Anleger Gewinne mitgenommen haben? Von Dezember 2018 bis Juni 2019 erzielte ein ausgewogenes Multi-Asset-Portfolio eine Rendite von 10% USD bei einer annualisierten Volatilität von 5% – eine klare historische Anomalie. Berücksichtigt man jedoch die negative Entwicklung der Märkte Ende 2018, so ergibt sich eine andere Schlussfolgerung. Seit August 2018 liegen Aktien bei fast 0%, während Anleihen 7% erzielten, was der langfristigen Sharpe-Ratio in USD von traditionellen Anlagen von nahezu 0,5 entspricht. Unseres Erachtens stellt die rollierende Zwölf-Monats-Performance an den Märkten keine Anomalie dar.

Abbildung 5: Multi Asset Fund Beta zu Aktien und Anleihen

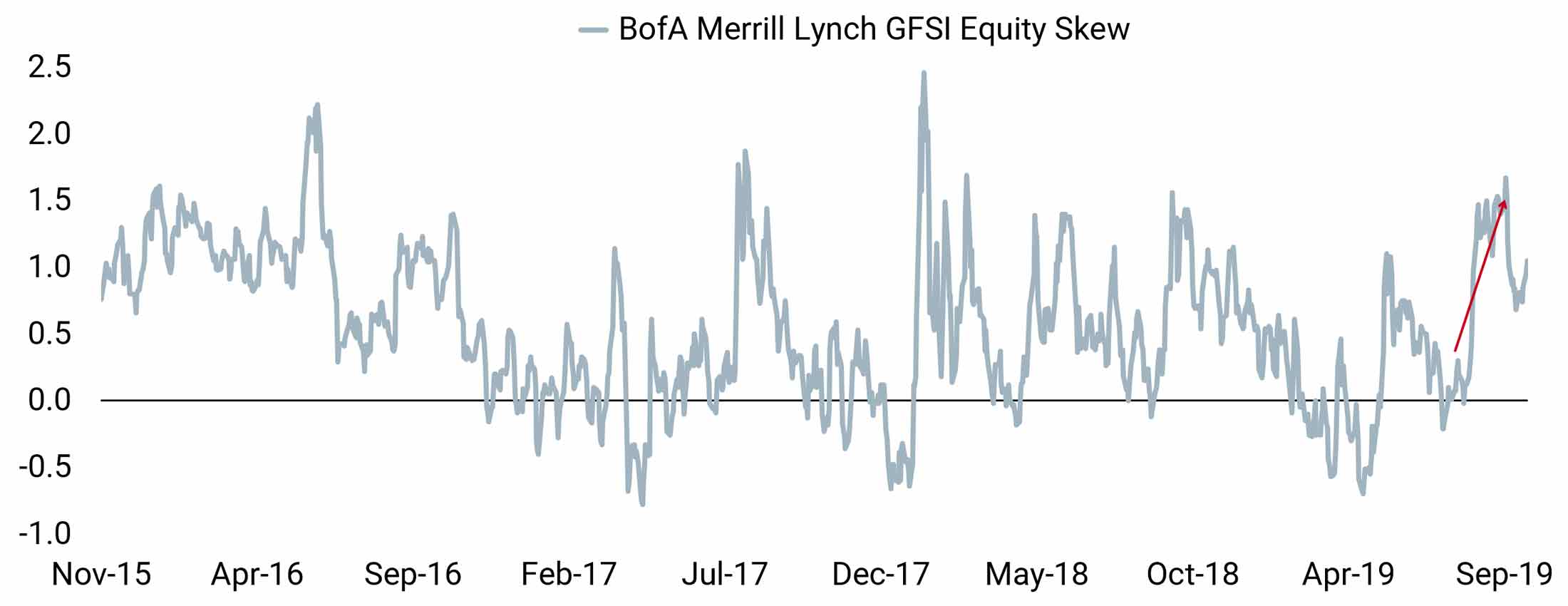

Hedging-Kosten gegen einen Marktrückgang sind ein guter Indikator dafür, wie vorsichtig Investoren heute positioniert sind. Abbildung 6 zeigt Veränderungen der Schiefe der Aktien- und Devisenmärkten – ein Maß für die Nachfrage nach Hedges gegen Marktrückgängen gegenüber Marktanstiegen. Die Nachfrage nach Absicherungen gegen Abwärtsrisiken ist deutlich gestiegen, während Multi-Asset-Fonds ihre Engagements reduziert haben (siehe Abbildung 5). Die Anleger haben daher das Hedging in jüngster Zeit erheblich erhöht, ein deutliches Zeichen für Pessimismus. Im Zusammenhang zu diesen höheren Hedging-Kosten gegen Abwärtsrisiken glauben wir, dass der Devisenmarkt einige interessante Alternativen zum Schutz vor einem globalen Abschwung der Wachstumswerte bieten kann2.

Abbildung 6: Schiefe des Marktes für Aktienoptionen

Investoren haben zuletzt Gewinne mitgenommen, aber auch ein hohes Maß an Downside-Hedging zeigt einen Pessimismus, den wir vorerst nicht teilen. Wir sehen diesen Pessimismus als Anlass für einen möglichen aufwärts Squeeze und glauben, dass die Märkte im Laufe des nächsten Quartals ihre Einschätzung der Makro-Situation neu bewerten werden.

Bewertungen Sind Hoch, Aber Uneinheitlich

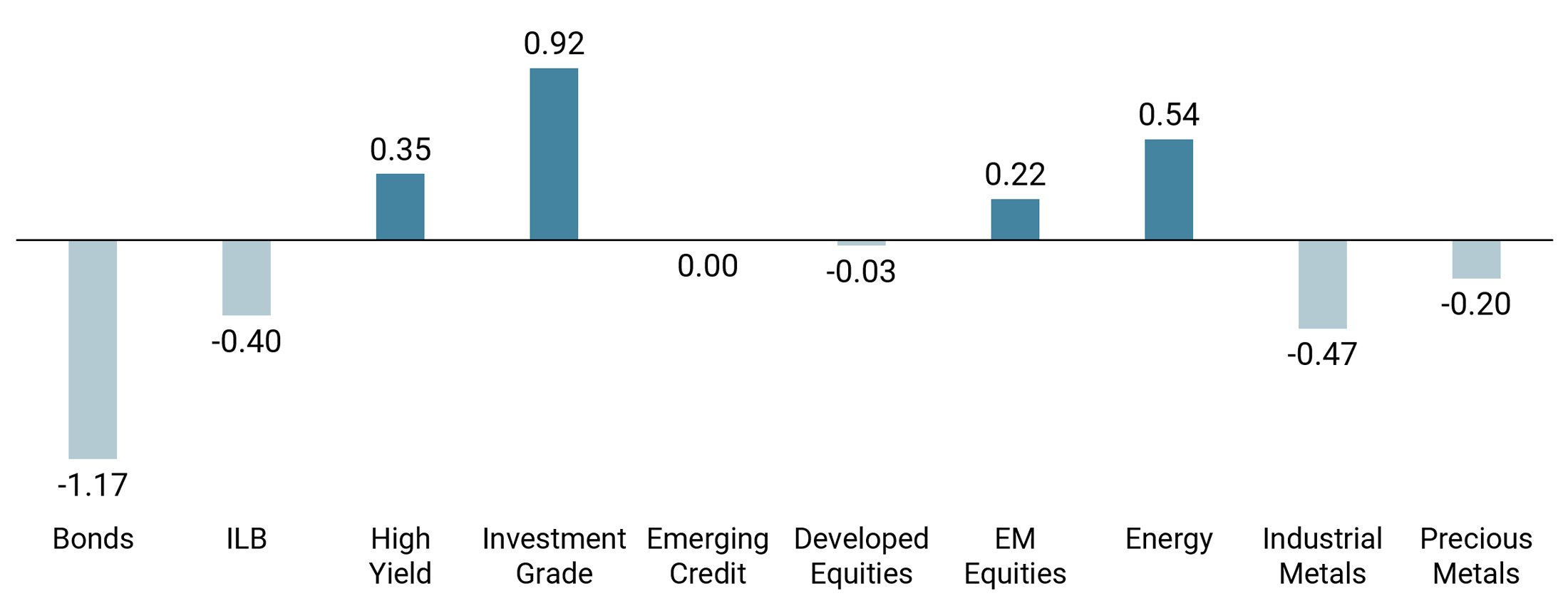

Schließlich denken wir, dass die Bewertungen der Märkte etwas Interessantes aussagen. Abbildung 7 zeigt unsere Bewertungen auf Basis des Carry jeder Anlageklasse und zeigt, dass Vorsicht geboten ist. Zunächst einmal sind Hedging-Assets teuer. Anleihen sind derzeit am teuersten, weitaus mehr als Inflationslinker, Industrie- oder Edelmetalle. Aus dieser Sicht sind die Anleger schlecht auf eine Bewertungserholung vorbereitet, die zu einer deutlichen Verbilligung der Anleihen führen würde. Dagegen sehen viele wachstumsorientierte Risikoprämien wie Credit, Schwellenländeraktien und Energie billig aus. Innerhalb einer Bewertungsbandbreite von -2 (sehr teuer) bis +2 (sehr günstig) erreicht Energie derzeit +0,54 und Investment-Grade +0,92, obgleich sie in diesem Jahr bisher hohe Renditen erzielte.

Wir erwarten auch, dass das vierte Quartal angesichts der Bewertungsunterschiede zu einer stärkeren Differenzierung innerhalb der geografischen Aktienindizes führen wird. Betrachtet man eine Vielzahl von Bewertungskennzahlen in Perzentilen, darunter EV/Umsatz, KBV oder Verhältnis von Kurs zu freiem Cashflow, so ergeben sich deutliche Unterschiede. Der einzige Index, der nach allen Kriterien teuer ist, ist der S&P 500, während der TOPIX der einzige Index ist, der nach allen Maßen günstig ist. Zwischen den beiden Indizes liegt ein breites Spektrum an Teuerungswerten: Europäische Aktien sind nicht gerade billig, während Schwellenländer bei weitem nicht teuer sind. Sollte sich das Makro-Umfeld verbessern, dürften die Nachzügler von 2019 wohl von einem stärkeren Anlegerinteresse profitieren. In der Vergangenheit, als die Schwellenländer das aktuelle Bewertungsniveau erreichten, waren die daraus resultierenden 1- bis 6-Monats-Renditen mit etwa 1% pro Monat positiv. Ähnlich ist es beim MSCI World Index: Auf dem aktuellen Bewertungsniveau (und trotz dominanter US-Repräsentanz) zeigt die Geschichte, dass er im kommenden Quartal (im Durchschnitt) rund 3% Rendite erzielen könnte. Wir gehen davon aus, dass die globalen Aktien im vierten Quartal eine positive Performance erzielen werden, die das Ungleichgewicht zwischen den USA und anderen Aktienindizes verringert.

Abbildung 7: Unigestion Cross-Asset-Bewertungs-Scoring

Hinweis: Ein positives (negatives) Scoring bedeutet, dass die Anlage billig (teuer) ist. Die Bewertungen werden mit dem Carry der einzelnen Anlagen gegenüber anderen Anlagen und ihrer eigenen Historie ermittelt.

Unsere Analyse Stimmt Den Märkten Nicht Zu

Unser dynamischer Allokationsansatz offenbart ein Zusammenkommen verschiedener Elemente. Das globale Wachstum bleibt akzeptabel und weit entfernt vom Rezessionsniveau. Zugleich spricht die schwache Inflation weiterhin für eine beträchtliche Unterstützung der Zentralbanken. Die Stimmung ist aus unserer Sicht daher übermäßig negativ und birgt das Risiko einer schnellen Schwankung der Märkte, wie etwa in der ersten Septemberhälfte. Schließlich sind wir der Meinung, dass die Märkte die aktuellen Bewertungsrisiken nicht genügend erkennen. Anleihen und andere Hedge-Assets sind teuer, während bestimmte Growth Assets weiterhin fair bewertet sind.

Unsere Allokation für das vierte Quartal spiegelt daher eine positivere Sichtweise wider als bei den meisten anderen: Wir stimmen dem derzeit herrschenden Pessimismus nicht zu und sind in Growth Assets übergewichtet. Wir halten diese Positionierung seit Anfang September und sehen derzeit keinen Grund, sie vorerst zu ändern. Wir erwarten auch, dass die Unterstützung der Zentralbanken positiv für Carry-bezogene Anlagen und Strategien sein wird.

Wir sind uns jedoch der Risiken bewusst, wie z. B. einer weiteren Verschlechterung des Handelskrieges, eines unerwartet schlechten Ausgangs in der Brexit-Situation oder einer wesentlichen Verschlechterung des Makro-Newsflows. Wir suchen daher weiterhin nach Hedging-Möglichkeiten, insbesondere im Devisenmarkt, und nutzen verschiedene FX-Crosses und Strategien, um die Kosten, die durch die Schiefe an den Aktienoptionsmärkten entstehen, auszugleichen.

1 Siehe „Verwirrende Rezessionsdaten“, September 2019.

2 Siehe „FX Risk Premia: a Cost-efficient and Liquid Way to Hedge Equity Risk“, September 2019.

Wichtige informationen

Dieses Material wird Ihnen vertraulich zur Verfügung gestellt und darf weder ganz noch teilweise verteilt, veröffentlicht, vervielfältigt oder gegenüber Dritten offengelegt werden.

Die in diesem Material präsentierten Informationen und Daten können sich auf generelle Marktaktivitäten oder Branchentrends beziehen, sie sind jedoch nicht als Grundlage für Prognose-, Analyse- oder Anlageberatungszwecke vorgesehen. Diese Informationen und Daten sind keine Finanzwerbung und stellen kein Angebot, keine Aufforderung und keine Empfehlung irgendeiner Art für Anlagen in den Strategien oder in den betreffenden Anlageinstrumenten dar. Einige der hierin beschriebenen oder erwähnten Anlagestrategien können als Anlagen mit hohem Risiko und als nicht schnell zu realisierende Anlagen angesehen werden, die zu erheblichen und plötzlichen Verlusten führen können, einschließlich eines vollständigen Verlusts der Anlage.

Unabhängig von dem Datum, an dem Sie möglicherweise auf diese Informationen zugreifen, stellen die in diesem Material zum Ausdruck gebrachten Anlageüberzeugungen, Wirtschafts- und Marktansichten oder Analysen die Einschätzung von Unigestion zum Publikationsdatum dar. Für die Richtigkeit dieser zum Ausdruck gebrachten Überzeugungen und Ansichten gibt es keine Garantie, und diese stellen keine vollständige Beschreibung der betreffenden Wertpapiere, Märkte und Entwicklungen dar. Alle hier zur Verfügung gestellten Angaben können ohne Vorankündigung geändert werden. Sofern vorliegendes Dokument Aussagen über die Zukunft enthält, handelt es sich um zukunftsgerichtete Informationen, die mehreren Risiken und Unwägbarkeiten unterliegen, einschließlich der Auswirkungen von Konkurrenzprodukten, Marktakzeptanz- und sonstiger Risiken, wobei diese Aufzählung keinen Anspruch auf Vollständigkeit erhebt.

Die Daten und grafischen Informationen in diesem Dokument dienen ausschließlich Hinweiszwecken und stammen unter Umständen aus externen Quellen. Obwohl wir die von öffentlichen Quellen und Drittquellen bezogenen Informationen für zuverlässig halten, haben wir diese nicht unabhängig verifiziert und können deren Richtigkeit oder Vollständigkeit daher nicht gewährleisten. Folglich werden keine Zusicherungen oder Garantien, weder ausdrücklich noch implizit, von Unigestion in dieser Hinsicht gemacht oder gemacht werden und es wird keine Verantwortung oder Haftung übernommen. Sofern keine anderslautenden Angaben gemacht werden, stammen die Daten und Informationen von Unigestion. Die Ergebnisse aus der Vergangenheit sind kein Anhaltspunkt für zukünftige Ergebnisse. Alle Anlagen sind mit Risiken verbunden, einschließlich des Risikos eines Gesamtverlusts für den Anleger.

Unigestion SA ist durch die Eidgenössische Finanzmarktaufsicht (FINMA) zugelassen und wird von dieser reguliert. Unigestion (UK) Ltd. wurde von der britischen Financial Conduct Authority (FCA) zugelassen, wird von dieser reguliert und ist bei der Securities and Exchange Commission (SEC) eingetragen. Unigestion Asset Management (France) S.A. ist durch die französische Autorité des Marchés Financiers (AMF) zugelassen und wird von dieser reguliert. Unigestion Asset Management (Canada) Inc. mit Niederlassungen in Toronto und Montreal ist als Portfoliomanager und/oder befreiter Händler („exempt market dealer“) in neun Provinzen Kanadas und außerdem als Investmentfondsmanager in Ontario und Quebec zugelassen. Die Hauptaufsichtsbehörde ist die Ontario Securities Commission (OSC). Unigestion Asia Pte Limited ist durch die Monetary Authority of Singapore (MAS) zugelassen und wird von dieser reguliert. Unigestion Asset Management (Copenhagen) wird gemeinsam von der Autorité des Marchés Financiers (AMF) und der Danish Financial Supervisory Authority (DFSA) reguliert. Unigestion Asset Management (Düsseldorf) SA wird gemeinsam von der Autorité des Marchés Financiers (AMF) und der Bundesanstalt für Finanzdienstleistungsaufsicht (BAFIN) reguliert.

Veröffentlichungsdatum dieses Dokuments ist der Oktober 2019.